.png)

.webp)

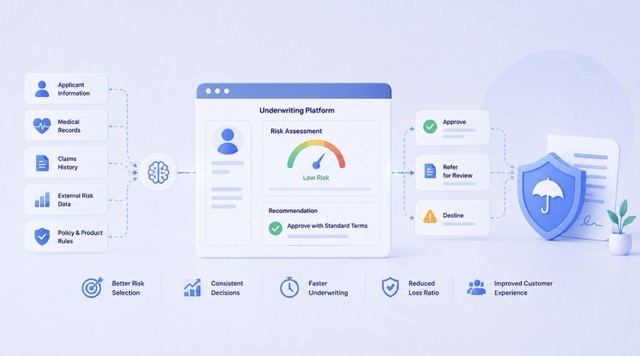

An underwriting software is a specialized tool used by insurance companies and financial institutions to assess risks associated with providing insurance coverage or loans. It automates the underwriting process, which involves evaluating an applicant's eligibility, determining premiums or interest rates, and deciding whether to approve or deny the application.

Underwriting software is essential for insurance companies and financial institutions, providing efficient risk assessment, accurate pricing, and streamlined processes. By automating underwriting tasks, organizations can save costs, ensure compliance, and enhance the overall customer experience. Its role in decision support and analytics helps in making informed decisions and managing risks effectively.

Challenges in Traditional Underwriting Process

Traditional underwriting processes often face several challenges that hinder efficiency and effectiveness. Here are some common challenges associated with traditional underwriting:

1. Manual Data Entry: Traditional underwriting involves time-consuming manual data entry, leading to errors and inconsistencies.

2. Limited Scalability: Traditional methods may struggle to handle large volumes of applications efficiently.

3. Lack of Automation: Manual tasks in traditional underwriting reduce productivity and increase the risk of errors.

4. Inflexible Workflows: Rigid workflows hinder adaptability to changing business requirements.

5. Compliance Challenges: Difficulty in keeping up with evolving compliance standards increases the risk of non-compliance.

Overall, the challenges associated with traditional underwriting highlight the need for modernization and digital transformation in the insurance industry. By adopting innovative technologies like Nected, insurers can overcome these challenges and streamline their underwriting processes for improved efficiency and accuracy.

Why Do Businesses Leverage Underwriting Softwares?

Businesses are increasingly turning to underwriting software for several key reasons:

1. Efficiency Boost: Automation of manual tasks accelerates processes, reducing processing times significantly.

2. Accuracy Enhancement: Advanced algorithms and data analytics ensure more precise underwriting decisions, minimizing errors.

3. Improved Risk Management: Comprehensive risk visibility and analysis tools enable quick risk identification and proactive mitigation.

4. Compliance Streamlining: Built-in compliance features automate checks and documentation processes, ensuring adherence to industry standards.

5. Scalability and Flexibility: Underwriting software can be scaled easily to meet evolving business needs and offers customizable features to tailor workflows accordingly.

Underwriting software drives operational efficiency, risk mitigation, compliance adherence, and adaptability to market changes, giving businesses a competitive edge and facilitating long-term success & enables businesses to automate even more complex underwriting tasks and processes, further enhancing accuracy and efficiency.

To summarize, businesses are leveraging underwriting software for a variety of reasons, including efficiency improvement, accuracy enhancement, cost savings, scalability, compliance adherence, and customer satisfaction. By automating manual underwriting tasks, businesses can streamline processes, reduce errors, and allocate resources more effectively.

Key features of an Underwriting Software

The key features of an underwriting software are as follows:

1. Risk Assessment Algorithms: Underwriting software employs sophisticated algorithms to analyze various risk factors associated with insurance or lending, such as applicant demographics, credit history, and policy details. These algorithms help underwriters evaluate risk levels accurately and make data-driven decisions.

2. Data Analytics Capabilities: Underwriting software integrates with data analytics tools to process large volumes of data efficiently. By leveraging analytics, underwriters can identify patterns, trends, and correlations in the data, enabling them to make more insightful risk assessments and pricing decisions.

3. Customizable Rules Engines: Underwriting software allows users to define and customize underwriting rules based on specific business requirements and risk tolerance levels. These rules engines automate decision-making processes, ensuring consistency and compliance with regulatory standards.

4. Integration with External Data Sources: Underwriting software seamlessly integrates with external data sources, such as credit bureaus, government databases, and third-party services, to access additional information relevant to the underwriting process. This integration enhances the depth and accuracy of risk assessments.

5. Document Management: Underwriting software provides document management capabilities to streamline the collection, storage, and retrieval of relevant documents and records. This feature ensures that underwriters have access to all necessary information to make informed decisions.

6. Communication and Collaboration Tools: Underwriting software often includes communication and collaboration features, such as messaging systems and task assignment capabilities, to facilitate efficient communication among underwriting teams. This fosters collaboration and ensures that tasks are completed in a timely manner.

7. Reporting and Analytics: Underwriting software generates comprehensive reports and analytics dashboards to track key performance metrics, monitor underwriting efficiency, and identify areas for improvement. These insights help organizations optimize their underwriting processes and enhance overall operational effectiveness.

8. Compliance Management: Underwriting software includes features to ensure compliance with regulatory requirements and internal policies. It automates compliance checks, monitors regulatory changes, and generates compliance reports to mitigate compliance risks effectively.

These key features collectively empower underwriters to assess risks accurately, streamline processes, improve efficiency, and maintain compliance with regulatory standards.

Who needs an Underwriting software?

Insurance underwriting software is essential for entities like insurance companies, underwriting agencies, and insurance brokers. Additionally, businesses in industries such as healthcare, finance, and real estate benefit from underwriting software to assess risks associated with their operations and secure appropriate insurance coverage.

You might wonder for what purpose they need it? Let’s explore that further.

When to Use Underwriting Software?

There are various use cases where underwriting software becomes a necessity for businesses. Here are some general use cases for when companies require an underwriting software:

1. New Policy Applications: Underwriting software is used when individuals or businesses apply for new insurance policies. The software assesses the applicant's risk profile, determines eligibility, and generates underwriting decisions.

2. Policy Renewals: Insurance companies utilize underwriting software when renewing existing policies. The software reviews policyholder data, evaluates any changes in risk factors, and adjusts coverage terms or premium rates accordingly.

3. Claims Processing: Underwriting software plays a role in claims processing by analyzing claim information, assessing liability, and determining coverage eligibility. It helps expedite the claims settlement process while ensuring accurate and fair outcomes.

4. Risk Management: Insurance underwriting software is used for ongoing risk management activities. It monitors policyholder data, identifies emerging risks, and implements proactive measures to mitigate potential losses.

5. Compliance and Regulation: Insurance companies rely on underwriting software to ensure compliance with regulatory requirements and industry standards. The software applies underwriting rules and guidelines in accordance with applicable laws and regulations.

These are just a few examples of how underwriting software is used across various stages of the insurance lifecycle. For more detailed insights, you can explore our blog on top underwriting insurance softwares, which delves into specific software solutions and their features.

How to choose the right underwriting software?

When selecting the right underwriting software for your organization, it's crucial to consider several key factors to ensure it meets your specific needs and requirements. Here's a guide to help you make the right choice:

1. Assess Functionality: Evaluate the software's ability to handle complex underwriting tasks, such as risk assessment algorithms, data validation, and policy customization.

2. Data Integration: Look for software that seamlessly integrates with your existing data sources, including CRM systems, databases, and external APIs, to ensure efficient data management and processing.

3. Review Automation Capabilities: Consider the software's automation features, such as rule-based decision engines, workflow automation, and document generation, to streamline underwriting processes and reduce manual effort.

4. Customizability: Ensure the software offers customization options to tailor workflows, rules, and user interfaces to match your specific underwriting requirements and preferences.

5. Security Measures: Prioritize software that implements robust security measures, including data encryption, access controls, and compliance with industry standards such as GDPR and HIPAA, to protect sensitive underwriting data.

6. Scalability: Choose software that can scale to accommodate your growing business needs, including increased transaction volumes, expanded product lines, and additional underwriting complexities.

7. Cost Consideration: Assess pricing structures, including upfront costs, subscriptions, and implementation expenses. Choose a solution balancing affordability with essential features and consider long-term savings through efficiency gains.

How to Implement the Underwriting process using Nected?

Underwriting software streamlines specific tasks within the underwriting process, and Nected's intuitive editor simplifies this by offering tools to design these processes with precision and adaptability.

Let us take a look on how you can use Nected's low code no code rule engine for underwriting purpose:

Step 1: Begin by integrating relevant data sources into Nected, such as customer information, claims history, and risk assessment data. This step ensures that all necessary information is accessible within the platform for underwriting analysis.

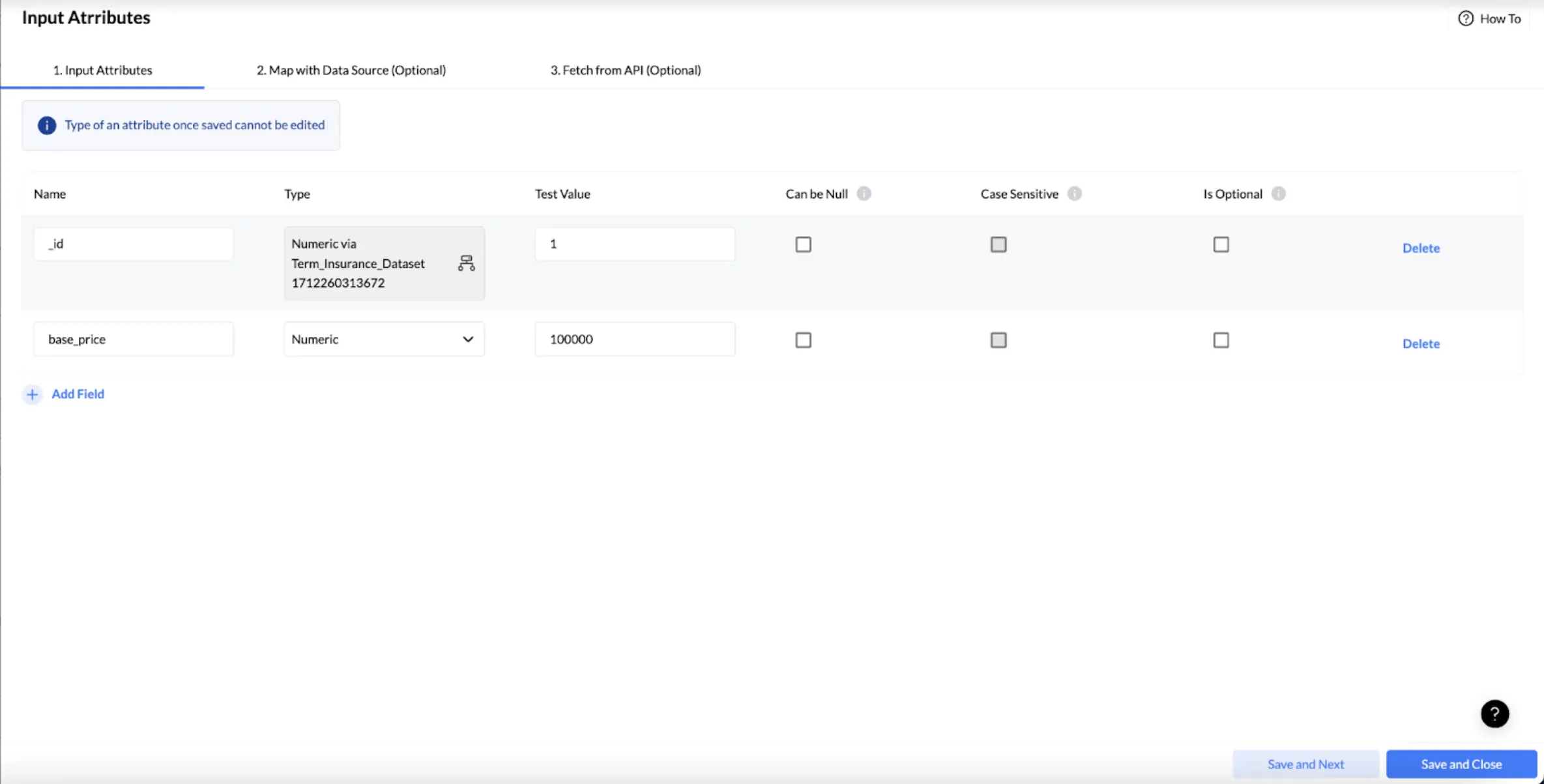

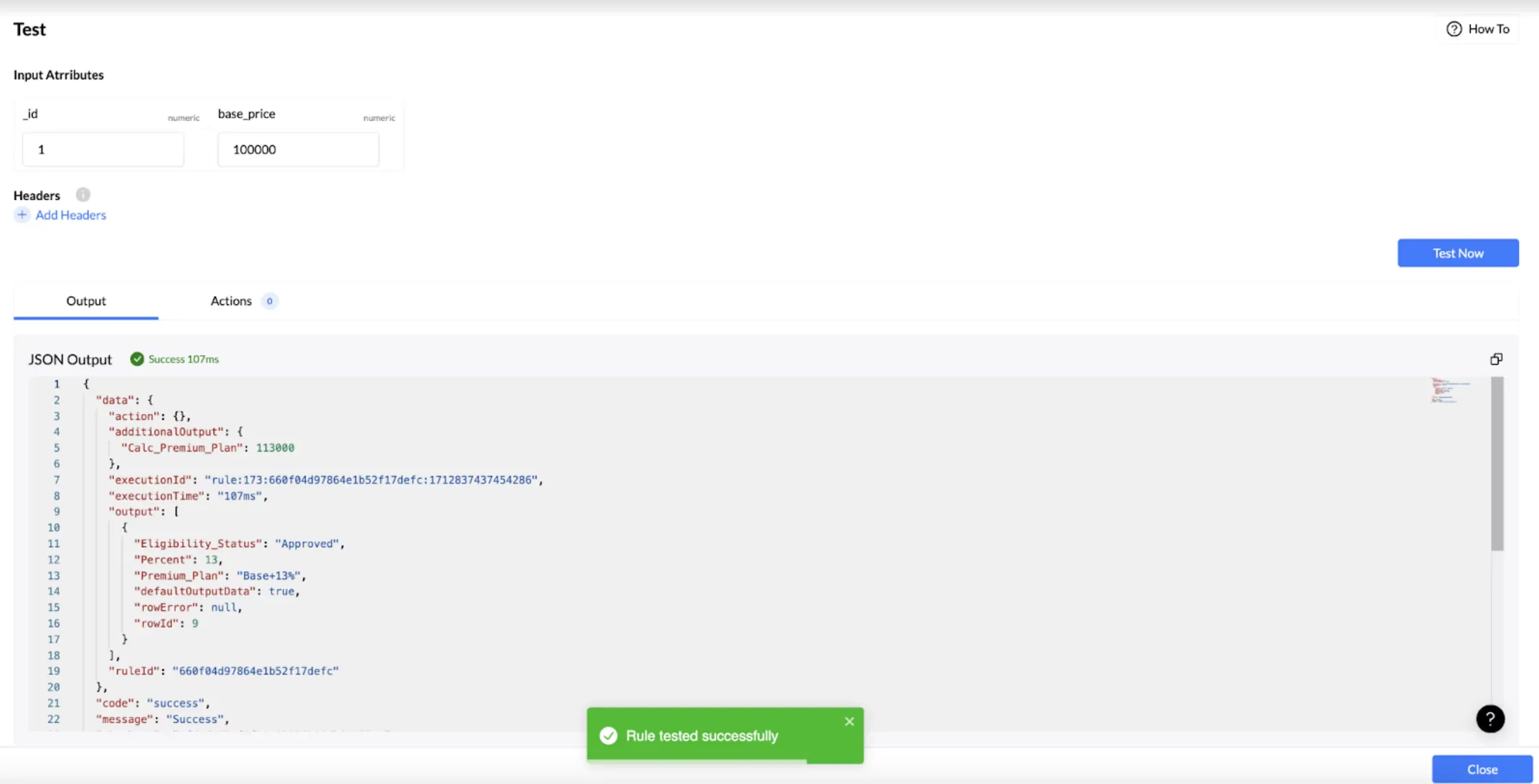

Step 2: Utilize Nected's intuitive interface to configure underwriting rules based on predefined criteria and risk factors. Define rule sets for various underwriting scenarios, specifying conditions and actions for automated decision-making. Refer the image below to see the conditions decided for a life insurance underwriting.

Step 3: Once rules are configured, Nected automates the underwriting process, applying rules to incoming data and generating decisions in real-time. Automated notifications and alerts ensure that underwriters are promptly informed of any exceptions or manual review requirements.

Nected, with its intuitive interface, powerful automation capabilities, and cost-effective solutions, emerges as a frontrunner in the realm of underwriting software. By leveraging Nected's advanced features, insurance companies can enhance their underwriting processes, improve efficiency, and stay ahead in today's dynamic insurance landscape.

Conclusion

In conclusion, the adoption of underwriting software marks a pivotal shift in the insurance industry, streamlining processes, enhancing accuracy, and boosting efficiency. We have also seen the shift from traditional underwriting to the modern no code underwriting process. No Code tool like Nected empowers insurance companies to navigate the complexities of underwriting with confidence. As technology continues to reshape the insurance landscape, Nected remains at the forefront, driving innovation and delivering unparalleled value to its users.

Enhance your underwriting efficiency with Nected. Signup today!

FAQs

Q1. What technology do underwriters use?

Underwriters use a variety of technologies, including underwriting software, data analytics tools, and digital platforms, to assess risks, evaluate applications, and make informed decisions about insurance policies.

Q2. What is the underwriting system in insurance?

The underwriting system in insurance refers to the process of evaluating risks associated with insuring individuals, properties, or events. It involves analyzing various factors such as demographics, health status, and past claims history to determine the eligibility and pricing of insurance policies.

Q3. Can underwriting processes be done using coding?

Yes, underwriting processes can be coded using traditional programming languages. However, utilizing coding requires significant technical expertise and time investment, making it less accessible and efficient compared to using low-code or no-code platforms like Nected.

.svg.webp)

.webp)

.jpg)

%20(1).webp)