.png)

.webp)

The usual way of deciding how much insurance costs doesn't always work out fairly. It's based on fixed rates decided by age, past events, etc. This approach doesn't consider everyone's unique situation or behavior. So, some people pay more than they should, while others pay less. Seeing these problems, people in the insurance world are curious about dynamic pricing, also called usage-based or personalized pricing. This dynamic pricing in insurance blog will tell you the approach consisting of fancy technology and data analysis to customize insurance costs based on each person's risk.

To learn more about this topic, continue reading this article.

What is dynamic pricing in insurance?

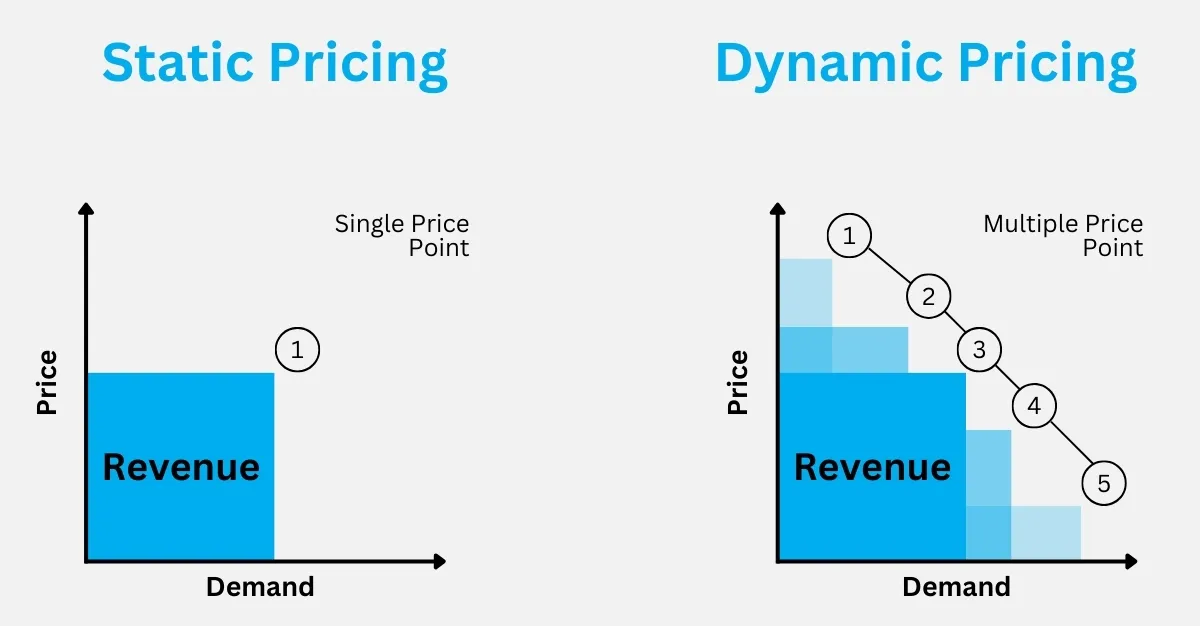

In the insurance industry, dynamic pricing is a pricing strategy that adjusts insurance premiums based on individual risk profiles and real-time data. Unlike traditional fixed pricing models, which apply uniform premiums to all policyholders within a specific category, dynamic pricing tailors premiums to reflect the specific risk that each policyholder presents.

Dynamic pricing leverages technological advancement, such as telematics devices, smartphone apps, and data analytics, to collect and analyze information about individual behaviors, circumstances, and preferences. This data may include driving habits, health metrics, lifestyle choices, and other relevant factors that influence the likelihood of filing a claim.

By analyzing this data, insurers can assess the level of risk posed by each policyholder more accurately and adjust premiums accordingly. For example, safe drivers who demonstrate responsible behavior behind the wheel may receive lower premiums, while risky drivers with a history of accidents may face higher premiums.

Why Dynamic Pricing is Better Than Traditional Pricing models?

This table will help you understand the benefits of dynamic pricing over traditional pricing models.

| Advantages | Dynamic Pricing in Insurance | Traditional Pricing Models |

| Fairness | Aligns premiums with individual risk profiles. | May lead to some individuals subsidizing higher-risk ones. |

| Flexibility | Adjusts premiums based on changing circumstances and behaviors. | Premiums remain static regardless of changes in risk factors. |

| Personalization | Tailors insurance coverage to individual needs and risk profiles. | Applies uniform premiums to all policyholders. |

| Efficiency | Allows for more accurate risk assessment and management. | May result in mismatches between premiums and claim costs. |

As you saw, dynamic pricing has many benefits but it comes with some challenges as well. Let’s see what are those challenges and how a Low code tool can address that.

Benefits of Dynamic Pricing for Insurers and Customers

Some of you might wonder why I should go for dynamic pricing? This table summarizes the benefits of dynamic pricing for insurance companies and policyholders.

| Benefits | Insurers | Policyholders |

| Improved Risk Management | Better assessment and management of risks. | Fairer pricing based on individual risk profiles. |

| Enhanced Profitability | Optimize revenue streams. | Cost savings through personalized premiums. |

| Competitive Advantage | Gain edge in competitive market. | Greater flexibility and customization. |

| Innovation and Differentiation | Develop new pricing models. | Incentives for risk mitigation. |

Dynamic pricing in insurance has two big benefits. First, it makes things fairer by setting premiums based on each person's risk. Second, dynamic pricing adds flexibility in terms of risk management, profitability, and competitiveness. On the contrary, policyholders benefit from fairer pricing, cost savings, flexibility, and incentives for risk mitigation.

Key Factors Considered In Insurance Dynamic Pricing

The key factors considered in dynamic pricing are as follows:

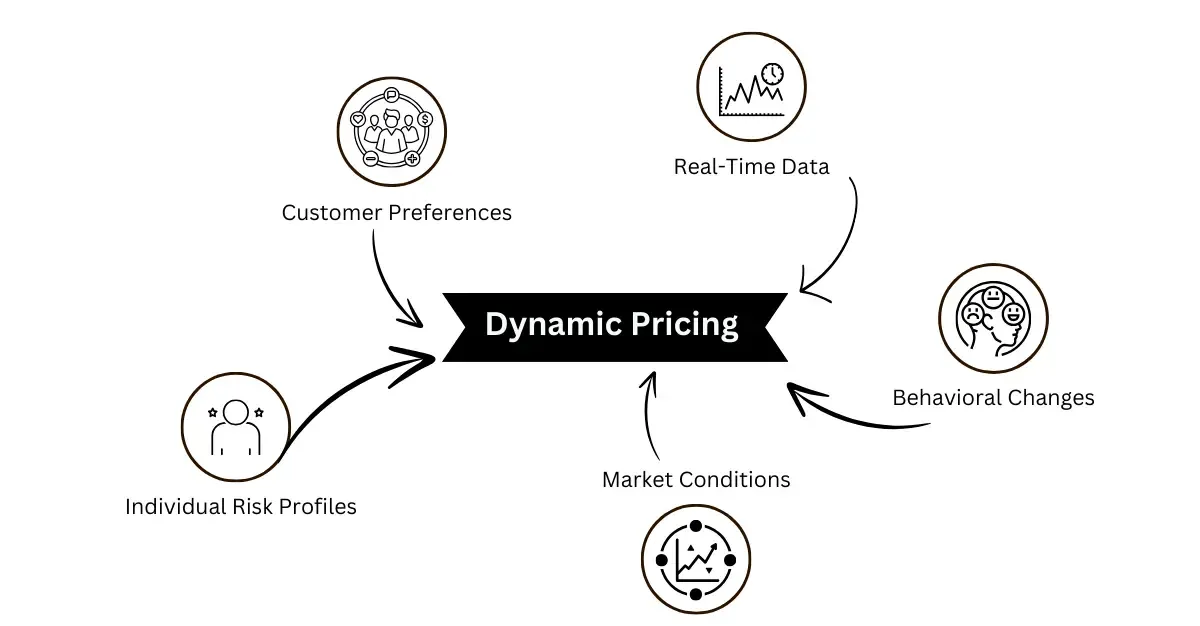

Individual Risk Profiles: Dynamic pricing analyzes individual characteristics, behaviors, and circumstances to assess the level of risk each policyholder presents. It includes factors such as driving habits, health metrics, lifestyle choices, and previous insurance claims history.

Real-Time Data: It relies on real-time data collection and analysis to continuously evaluate and adjust insurance premiums. This data may be gathered through telematics devices, smartphone apps, or other technologies that track and monitor relevant metrics.

Behavioral Changes: Dynamic pricing takes into account alterations in behavior or situations that influence levels of risk. For example, improvements in driving habits or health outcomes may lead to lower premiums, while riskier behavior could result in higher premiums.

Market Conditions: Dynamic pricing takes into account external factors such as market trends, regulatory changes, and economic conditions that may impact insurance risk and pricing.

Customer Preferences: Dynamic pricing takes into consideration customer preferences and willingness to share data in exchange for personalized insurance pricing. Insurers may offer incentives or rewards to encourage policyholders to participate in dynamic pricing programs.

How does Nected address the challenges posed in Dynamic Pricing?

There are still some major concerns and challenges in dynamic pricing. You must adhere to certain policies and create a fair dynamic pricing strategy.

This table will help you understand the challenges in dynamic pricing model deployment and how Nected can assist you in overcoming them with robust mechanisms and tools.

| Challenges | How Nected Addresses it | |

| Customer Perception and Fairness | Customers may feel unfairly treated due to fluctuating prices or demographic-based pricing. | You can use Nected to ensure transparency by clearly communicating factors influencing price changes and offering personalized discounts to mitigate perceived unfairness. |

| Data Privacy and Security | Collecting and analyzing customer data for dynamic pricing poses privacy and security risks. | Nected prioritizes robust data encryption, strict access controls, and compliance with regulations like GDPR, ensuring customer data is protected. |

| Algorithm Bias | Dynamic pricing algorithms may exhibit bias, leading to unfair treatment of certain customer segments. | Using Nected, you can conduct regular audits to identify and mitigate biases, incorporate fairness considerations into algorithm development, and provide channels for reporting and addressing bias concerns. |

| Competitive Pricing and Strategy | Competitors' reactions to dynamic pricing strategies can lead to price wars or negative customer perception. | Nected offers competitive analysis tools to monitor rivals' pricing strategies, allowing for adjustments. It emphasizes value differentiation over price and highlights unique features or services. |

| Operational Complexity | Implementing and managing dynamic pricing can be operationally complex. | Nected simplifies the process with user-friendly interfaces, automation tools, and comprehensive training and support for users. |

| Regulatory Compliance | Dynamic pricing must comply with various legal and regulatory frameworks. | Nected stays updated on regulations, aligns pricing practices with legal requirements globally, and collaborates with legal experts to ensure compliance, building trust among users. |

As we saw from the table, the various challenges that we came through while implementing a traditional dynamic pricing model, and how Nected addresses these challenges with ease.

In the subsequent section, we will get to know how to implement a dynamic pricing model for insurance with a low code tool like Nected.

Create a Dynamic Pricing Model For Insurance with Nected

If you want to set detailed dynamic pricing for your business, Nected can help you. The tool enables you to develop and implement dynamic pricing models effortlessly, eliminating the need for extensive coding typically associated with in-house dynamic pricing development.

Renowned for its innovative approach, Nected offers a low-code/no-code rule engine, simplifying integration with various data sources.

For example, if you want to set a dynamic pricing strategy for car insurance in your company, you can set it easily using different parameters.

Step 1: Assigning attributes

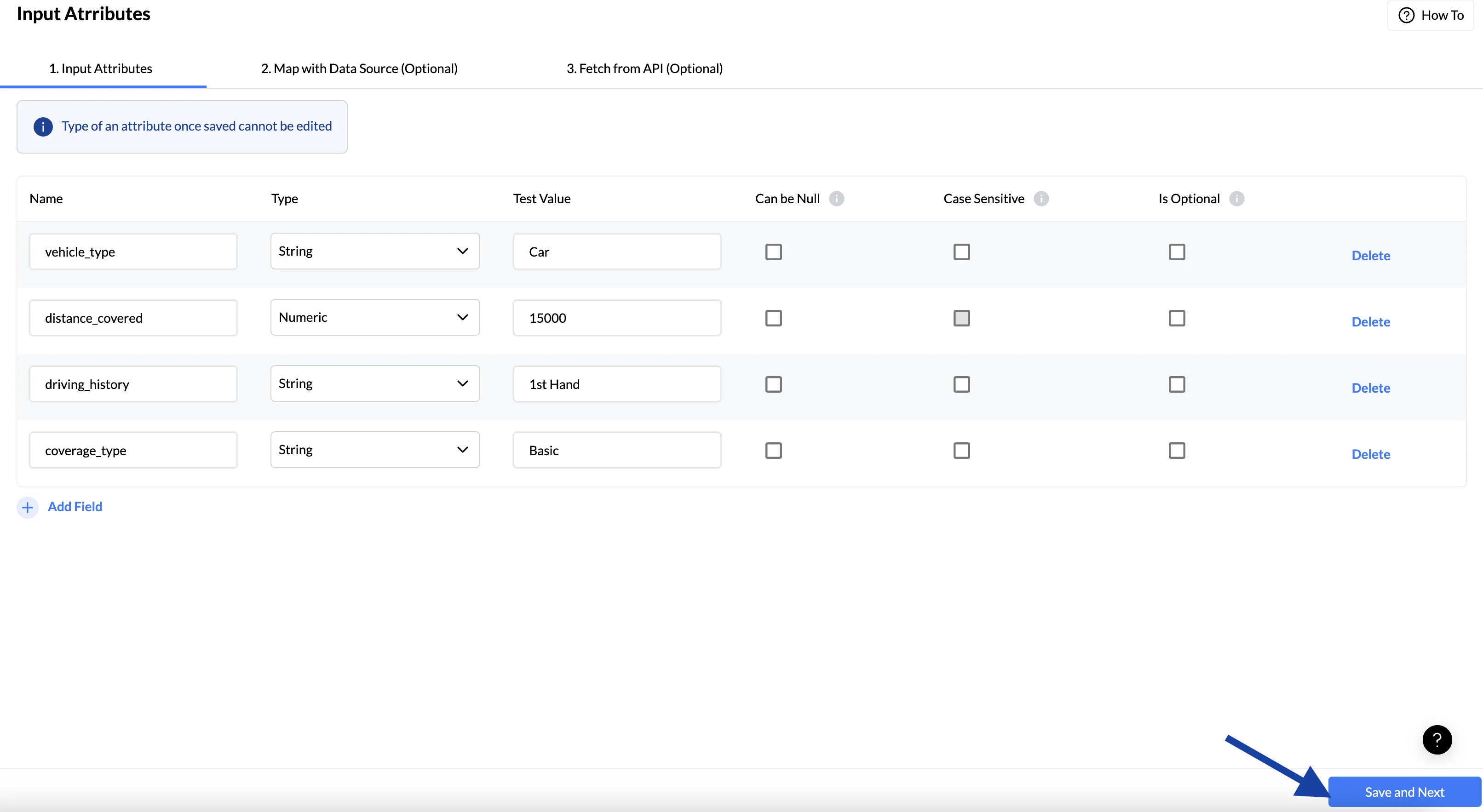

After logging in, navigate to the attributes section and select the parameters you want to build the model with.

In this example, we have selected the following parameters for creating the rule set:

- Vehicle Type: Whether the insured vehicle is a car, motorcycle, truck, or SUV.

- Distance Covered: The total distance traveled by the insured vehicle within a specific timeframe, influencing the risk assessment and insurance premium calculation.

- Driving History: History of accidents, traffic violations, or claims made by the policyholder.

- Coverage Type: The level of coverage selected by the policyholder, such as basic, comprehensive, or premium.

These parameters help determine your insurance premium.

Step 2: Setting the conditional logic

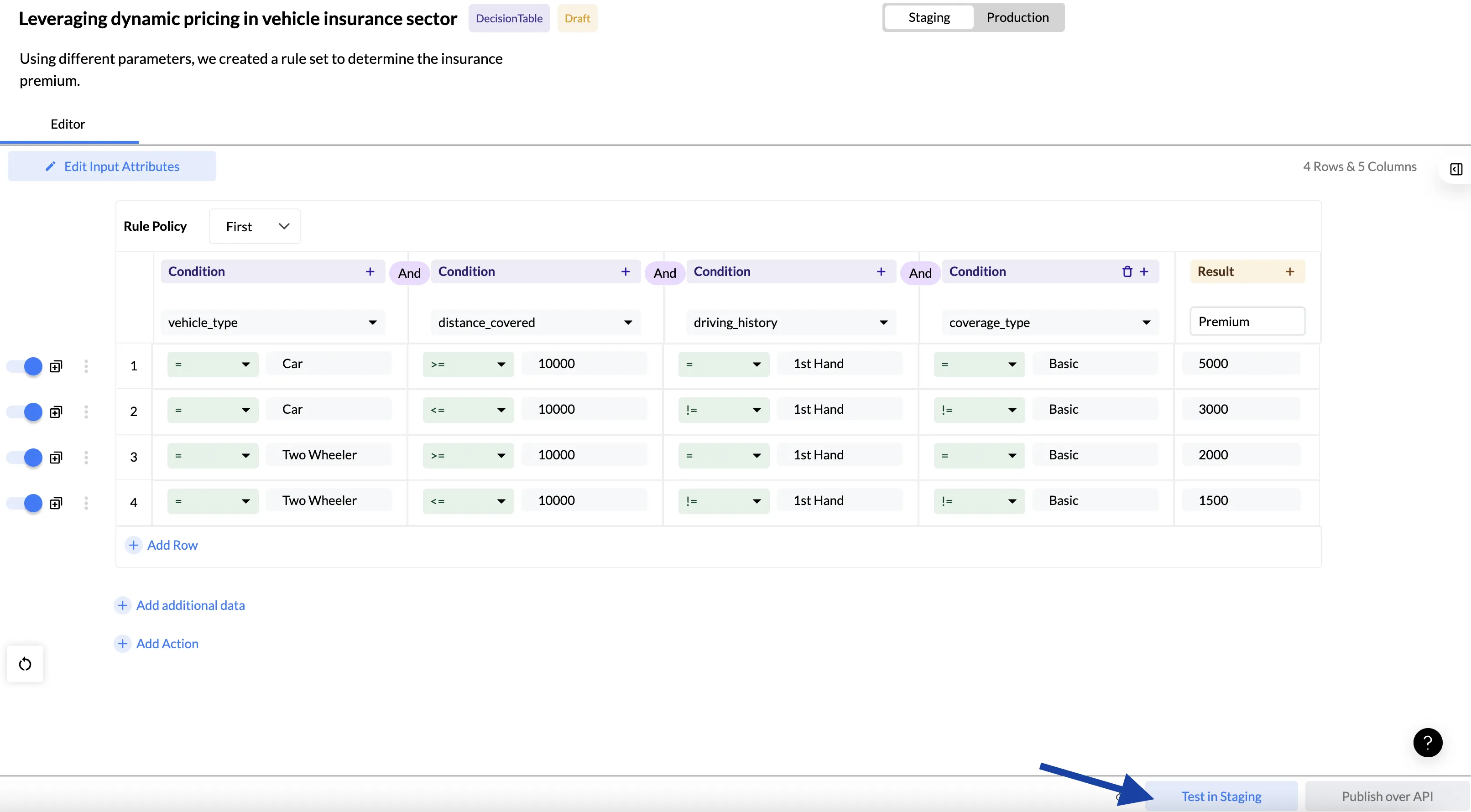

It is the most critical phase, where you will set the conditional logic and define your scoring mechanism to help evaluate the overall system.

Here, you can utilize the already set attributes, link them using the AND-OR logical rules, and assign them to a final value named score, as shown in the example.

Now, click the “Test in Staging” and proceed to the next step.

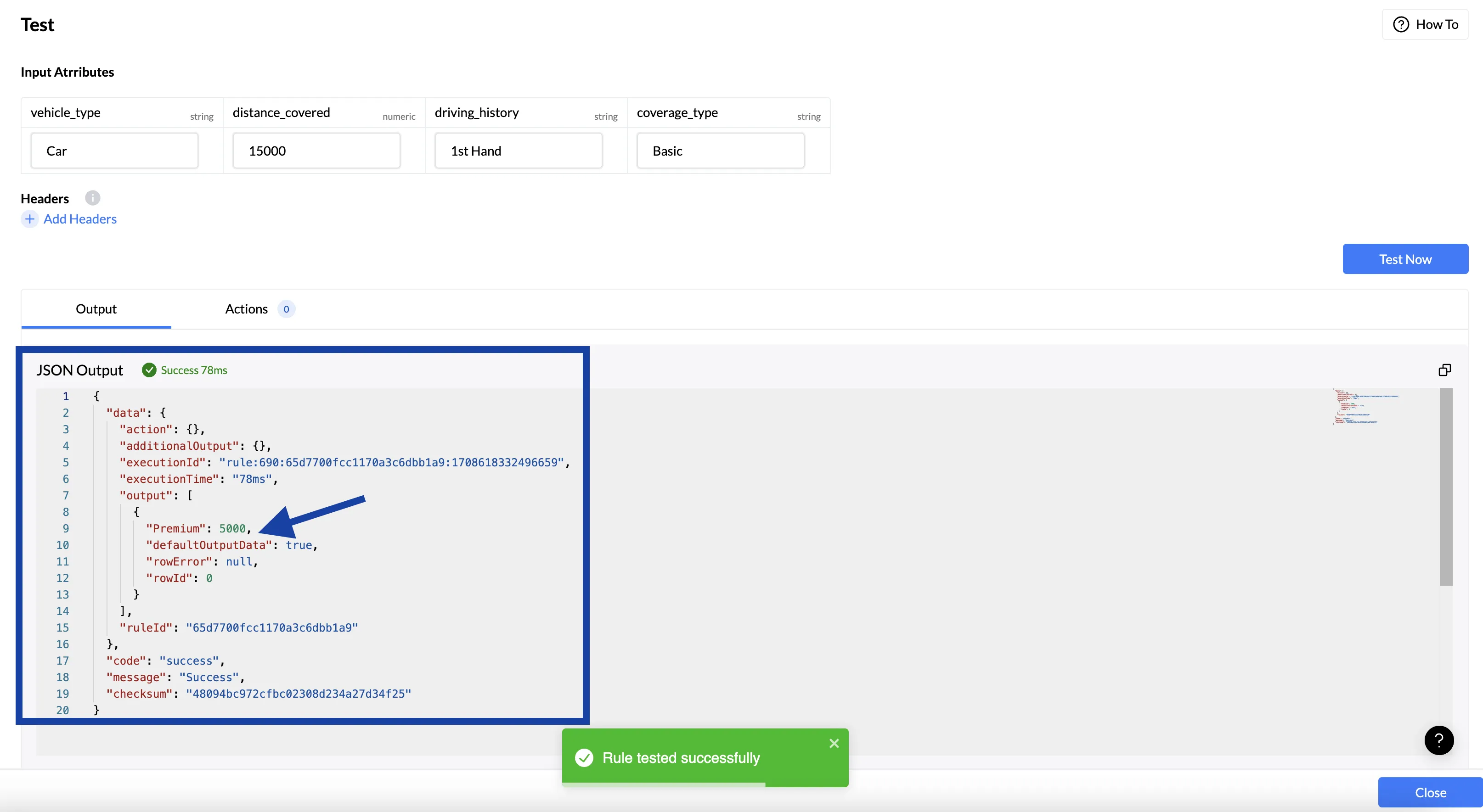

Step 3: Testing and confirmation

In the input attributes section, you can input the desired data and check the insurance premium for the vehicle insurer. In this example, you have used the data as,

- Vehicle Type: Car

- Distance Covered: 15000

- Driving History: 1st Hand

- Coverage Type: Basic

After inserting the data, click on the "Test Now" option and wait for the result. If it shows the message "Rule Tested Successfully" in the green marked area and the score in the JSON output channel, then your test is successful.

Also, you can retrieve the attribute values, check for different data, and use it for various purposes as required.

If you're interested in developing a dynamic pricing model for eCommerce, check out this article detailing how Nected assists in building dynamic pricing strategies tailored for eCommerce businesses.

Comparison between the Top Dynamic Pricing solutions

Let’s take a quick look at the comparison of dynamic pricing solutions -

| Nected | Pricefx | Zilliant | PROS Pricing | |

| Features | Dynamic pricing solution, Low-code/No-code rule engine | Comprehensive dynamic pricing solutions | AI-driven price optimization | Suite of tools for pricing optimization |

| Benefits | Rule-based dynamic workflows and personalized pricing based on customer behavior | Real-time recommendations based on market data | Personalized pricing based on customer behavior | AI and machine learning for predictive pricing |

| Integration | Integrates with CRM, ERP, and eCommerce platforms | Integrates with CRM, ERP, and eCommerce platforms | Integrates with leading CRM and ERP systems | Integrates with CRM, ERP, and eCommerce platforms |

| Customer Base | All sizes of industries in eCommerce, credit, and retail sectors. | Large enterprises across industries | Companies in manufacturing, and distribution | Global enterprises across industries |

| Flexibility | High | High | Moderate | Moderate |

| Transparency | High | Average | Average | Average |

If you're seeking an efficient solution for creating dynamic pricing strategies tailored to various insurance products for your business, Nected is your optimal choice. This tool empowers you to establish diverse rules and construct workflows specifically designed for dynamic pricing.

Conclusion

Dynamic pricing represents a significant step in enhancing fairness and flexibility within the insurance industry. By customizing premiums to individual risk profiles and adjusting them in real-time based on changing circumstances, dynamic pricing ensures that insurance costs accurately reflect each policyholder's actual risk.

Furthermore, dynamic pricing introduces much-needed flexibility into the insurance market, allowing premiums to adapt to evolving risk factors and consumer behaviors. It benefits policyholders by providing them with more relevant and cost-effective coverage and enables insurers to manage risks better and remain competitive in a dynamic marketplace.

Dynamic pricing can revolutionize the insurance industry, making it more consumer-centric, responsive, and efficient. By embracing this innovative approach, insurers can better meet the evolving needs of policyholders while fostering a more equitable and transparent insurance ecosystem.

Frequently asked questions [FAQ]

Q: How does dynamic pricing contribute to fairness in insurance premiums?

Dynamic pricing ensures fairness by adjusting premiums based on individual risk profiles. Safer drivers or healthier individuals pay lower premiums, while riskier ones pay more. This aligns costs more closely with actual risk, making insurance fairer for everyone.

Q: Are there any potential drawbacks or concerns associated with dynamic pricing in insurance?

While dynamic pricing offers benefits, there are concerns. Privacy issues arise from collecting personal data to set premiums. Plus, some may struggle with understanding how it works or accessing the technology needed. This could lead to inequalities in pricing.

Q: Is dynamic pricing available for all types of insurance policies?

Dynamic insurance pricing is gaining popularity across various insurance types, from auto and home to health and life insurance. Availability depends on factors like company policies, regulations, and technology. Expect its use to grow as technology advances and demand for personalized pricing increases.

.svg.webp)

%252520(1).webp)

%252520(1).webp)

%20Medium.jpeg)

%20(1).webp)