.png)

.webp)

Ever feel like your financial health hinges on a mysterious three-digit number? That's the world of credit scores, a crucial factor influencing loan approvals, insurance rates, and more. Understanding what goes into calculating your score is key to guiding the financial landscape. However, traditional credit scoring methods can be complex. Here's where Nected enters the scene. This innovative platform enables individuals and businesses with a simpler, transparent approach to credit scoring, potentially streamlining the process and nurturing a fairer financial future. Let's delve into the fascinating world of credit scores and explore how Nected can unlock new possibilities for you.

Understanding Credit Scoring Methods

.webp)

Imagine your credit score as a financial report card, a single number between 300 and 850 reflecting your creditworthiness. But how is this score calculated? Various methods analyze factors like payment history, credit utilization (how much credit you use compared to your limit), and debt levels. These methods use complex algorithms to weigh each factor's impact on your score, resulting in a single number summarizing your financial responsibility.

The Power of Credit Scores in Decision Making

Ever wondered why getting approved for a loan can feel like a mystery? Credit scores play a critical role in financial decision-making, impacting your access to loans, interest rates, and even insurance costs. Lenders use your score to assess your risk of repaying debt, similar to how teachers use grades to predict learning potential. A good score translates to lower risk, making you a desirable borrower and opening doors to better deals. Conversely, a low score can limit your options and make borrowing more expensive.

Exploring Types of Credit Scoring Methods

Your credit score is like a financial fingerprint, but how it's generated isn't always straightforward. While traditional methods based on credit bureau data have dominated for years, newer approaches are emerging to offer a more holistic picture. Let's explore some key types of credit scoring methods:

1. Traditional Bureau-Based Models

Think of them as the "classics": FICO and VantageScore are the most well-known examples, relying heavily on data from credit bureaus like Equifax, Experian, and TransUnion.

Each model uses different factors to calculate a credit score, and the weights given to each factor can also vary. Here's a breakdown of the factors and their weights for each model:

FICO SCORE

- Payment history (35%): This is the most essential factor in both models, as it shows how reliably you've made payments on past debts.

- Credit utilization (30%): This refers to how much of your available credit you're using. Lower utilization is generally better.

- Length of credit history (15%): Having a longer credit history can improve your score.

- New credit (10%): Opening too many new lines of credit in a short period can lower your score.

- Credit mix (10%): Having a variety of different types of credit, such as credit cards and loans, can help your score.

VANTAGE SCORE:

- Payment history (40%): Similar to FICO, payment history is the most important factor.

- Age and type of credit (21%): This combines the length of your credit history and the types of credit you have.

- Credit utilization (20%): Similar to FICO, lower utilization is typically preferable.

- Recent behavior (5%): This considers things like missed payments and inquiries into your credit report in the past few months.

- Available credit (3%): This considers how much-unused credit you have, similar to but less important than credit utilization in FICO.

.webp)

As you can see, there are some key similarities between the two models, but also some differences. For example, VantageScore gives more weight to your age and type of credit, while FICO gives more weight to your credit utilization.

It's important to remember that credit scores are just one piece of the puzzle when it comes to risk assessment. Lenders will also consider your income, debt-to-income ratio, and other factors when making a decision about whether or not to approve you for a loan.

Pros & Cons

- Pros: Standardized and widely accepted, offering a long-term perspective on your credit history.

- Cons: One-size-fits-all approach, neglecting alternative factors like rent payments or utility bills. Can be slow to update and lack transparency.

2. Alternative Data Scoring

As traditional methods rely heavily on credit history, they might exclude those new to credit or with limited borrowing experience. This is where alternative methods come in:

- Bank Account Data: Analyzing checking and savings account activity for income stability and responsible financial management. Credit scoring methods in banking are essential for assessing an individual's or a company's creditworthiness.

- Telecommunications Data: Examining payment history for phone and internet bills to assess financial behavior and reliability.

- Utility Bill Payment History: Similar to telecommunications data, looking at consistent and timely utility bill payments can build a creditworthiness picture.

- Social Media Data: While still in its early stages, analyzing public social media data for financial responsibility and stability is being explored, raising ethical concerns about data privacy.

Pros & Cons

- Pros: Provide a more comprehensive view of your financial health, potentially benefiting those with limited credit history.

- Cons: Still in their early stages, with potential concerns about data privacy and fairness.

3. Behavioral Scoring

Think of them as focusing on the "present": These methods analyze your recent credit behavior, like new credit inquiries or account closures, to assess risk.

Pros & Cons

- Pros: Offer a real-time snapshot of your current financial situation, potentially benefiting those actively improving their credits.

- Cons: May not capture your long-term financial responsibility, and potential data privacy concerns exist.

4. Open-Source Scoring

Think of them as the "collaborative approach": These methods utilize publicly available data and allow for customization, potentially opening doors for innovation and transparency.

Pros & Cons

- Pros: Offer greater control and understanding of how your score is calculated, promoting fairness and inclusivity.

- Cons: Still in their early stages, with potential challenges in data accuracy and widespread adoption.

What Are the Latest Trends in Credit Score Methodology

Let’s see the latest trends and points to consider of how your credit score is calculated and is evolving! Here's what's new:

- Beyond Credit Reports: Data like utility bills, rent payments, and even social media activity are now used to paint a broader picture of your financial responsibility, especially if you're new to credit.

- Smarter Algorithms: Machine learning helps predict your loan repayment ability by analyzing subtle patterns hidden to humans, making scoring more flexible and accurate.

- Reaching the "Invisible": Credit scoring systems are being designed to assess people without a traditional credit history, promoting financial inclusion.

- Beyond Numbers: Analyzing your online behavior can offer insights into your financial habits and attitudes, creating a more complete picture.

- Fairness First: Transparency and explainability are crucial to ensure models are free from bias.

- Instant Gratification: Digital solutions provide near-instant credit scoring, speeding up loan approvals.

- Personalized Products: Loan options are tailored to your individual risk profile, benefiting both lenders and borrowers.

By understanding these trends, you can navigate the evolving world of credit scoring with confidence!

Choosing the Right Credit Scoring Method

When choosing a credit scoring method, several points should be considered to ensure its effectiveness and relevance.

- Dedicated Focus & Expertise: Choose a method backed by a dedicated team of experts with the necessary technology to ensure effectiveness.

- Collaborative Development: Opt for methods developed and assessed through well-connected working groups for comprehensiveness

- Beyond Decision-Making: Consider methods that factor in more than just loan approvals, like pricing and regulatory capital.

- Adapting to Change: Select a method that can evolve alongside the expanding role of credit scoring in various financial processes.

- Data & Technology Driven: Favor methods leveraging increased data access, computing power, and the evolving financial landscape.

Nected: Revolutionizing Credit Scoring with 5 Key Advantages

.webp)

Want to ditch outdated and opaque credit scoring methods? Here's how Nected stands out:

- Fast & Effortless: Forget months of development. Nected streamlines the process, saving you time and resources in building effective credit scoring models.

- Tailored Scoring: No more one-size-fits-all models. Nected lets you design customized rules, ensuring your credit scoring reflects your unique needs and preferences.

- Grows with You: Whether you handle a handful or hundreds of applications, Nected scales effortlessly to accommodate your growing data volume.

- Transparency Unlocked: No more black boxes! Nected's rule-based approach makes it clear how each factor contributes to the score, building trust and understanding.

- Designed for Everyone: The user-friendly interface welcomes professionals of all technical backgrounds, making Nected accessible and intuitive for everyone.

Embrace a modern, efficient solution for credit scoring. Nected combines advanced capabilities with user-friendly design to empower you with clear, reliable, and tailored credit assessments.

Deploying Credit Scoring with Nected: A Detailed Walkthrough

Forget complex coding! Nected's user-friendly interface empowers you to build and deploy custom credit scoring models quickly and efficiently. Save time, resources, and gain a competitive edge in the market.

Step 1: Navigating the Nected Interface

.webp)

Begin by logging into the no-code/ low-code Nected platform.

Step 2: Launching a New Project

.webp)

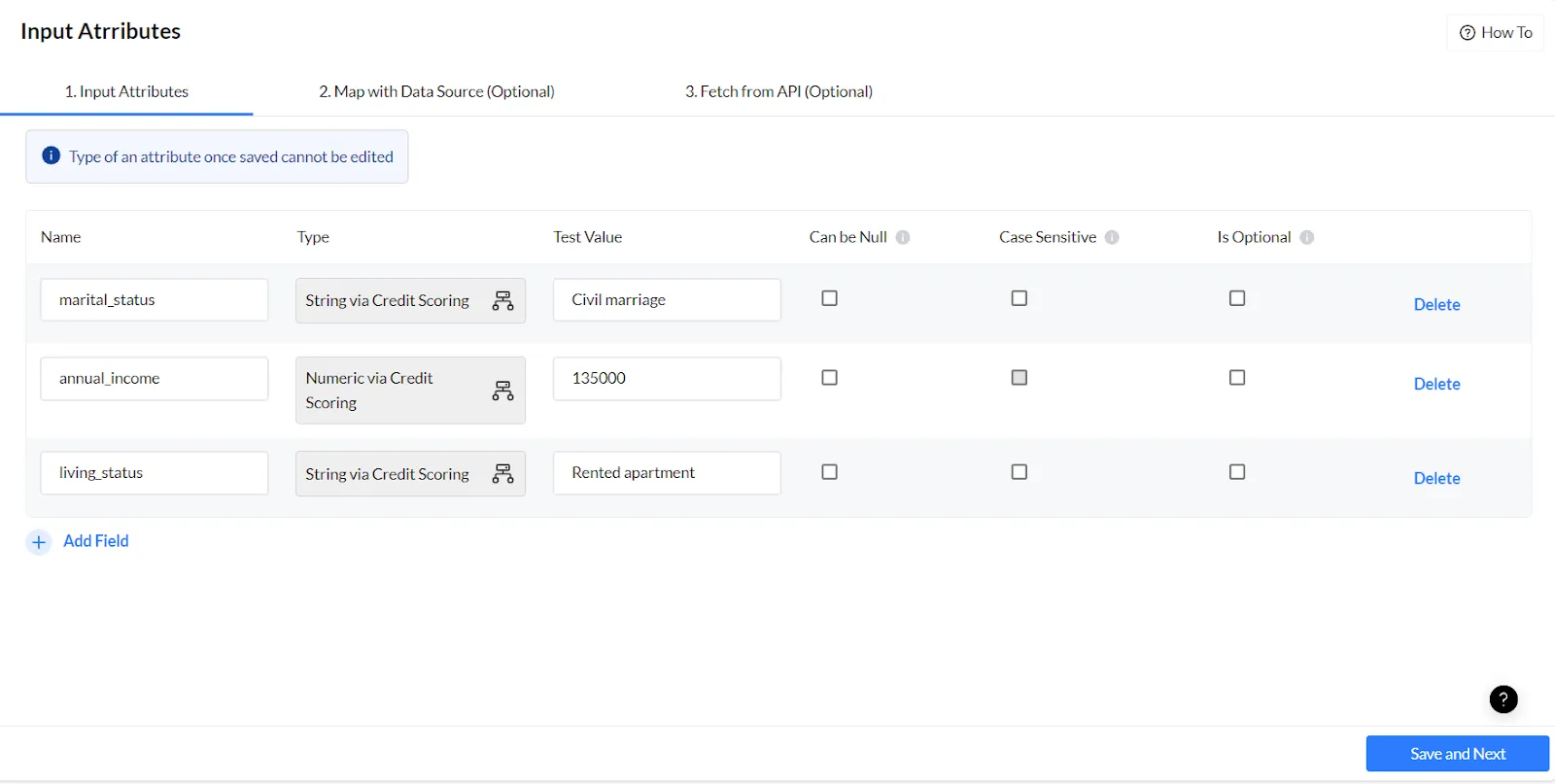

Establish a new rule within Nected tailored to your credit scoring initiative. Outline the project's scope, goals, and the precise criteria you aim to incorporate into your credit scoring framework.

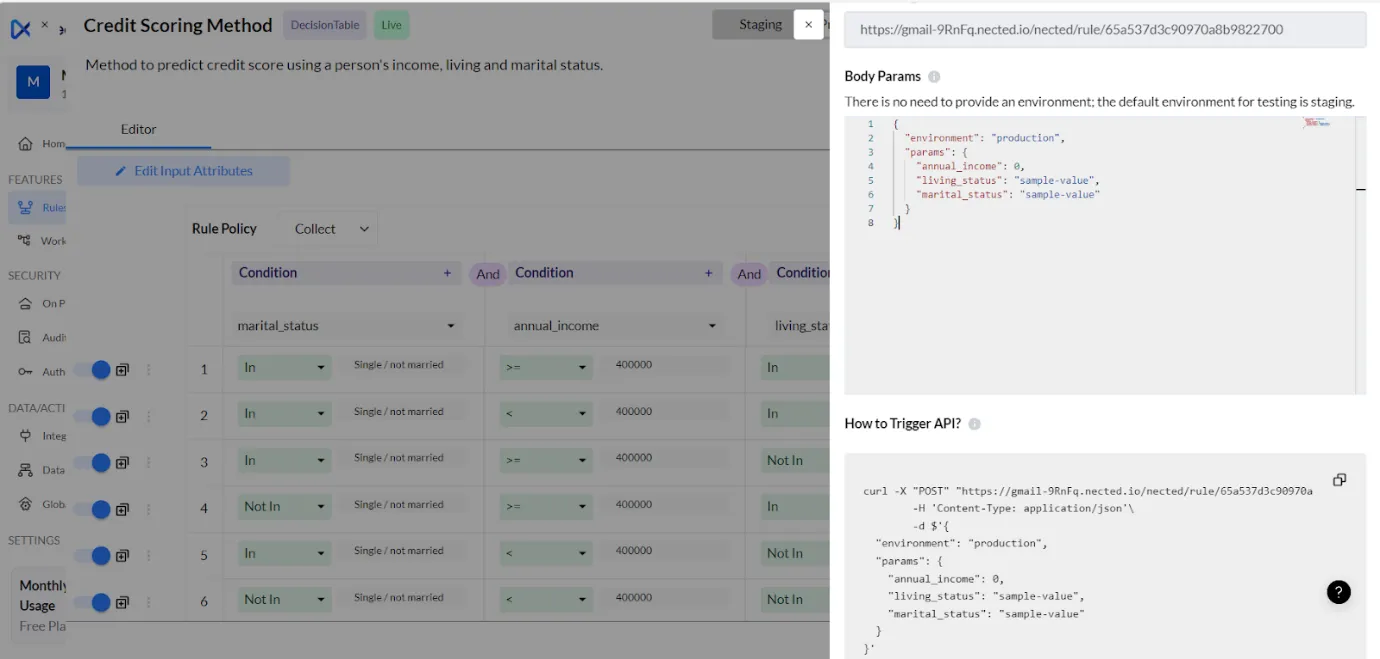

Step 3: Crafting Rule-Based Models

.webp)

Utilize Nected's rule-based methodology to design credit scoring models. Establish rules according to chosen features and criteria. Nected's low-code environment simplifies rule formulation, eliminating the necessity for complex coding abilities.

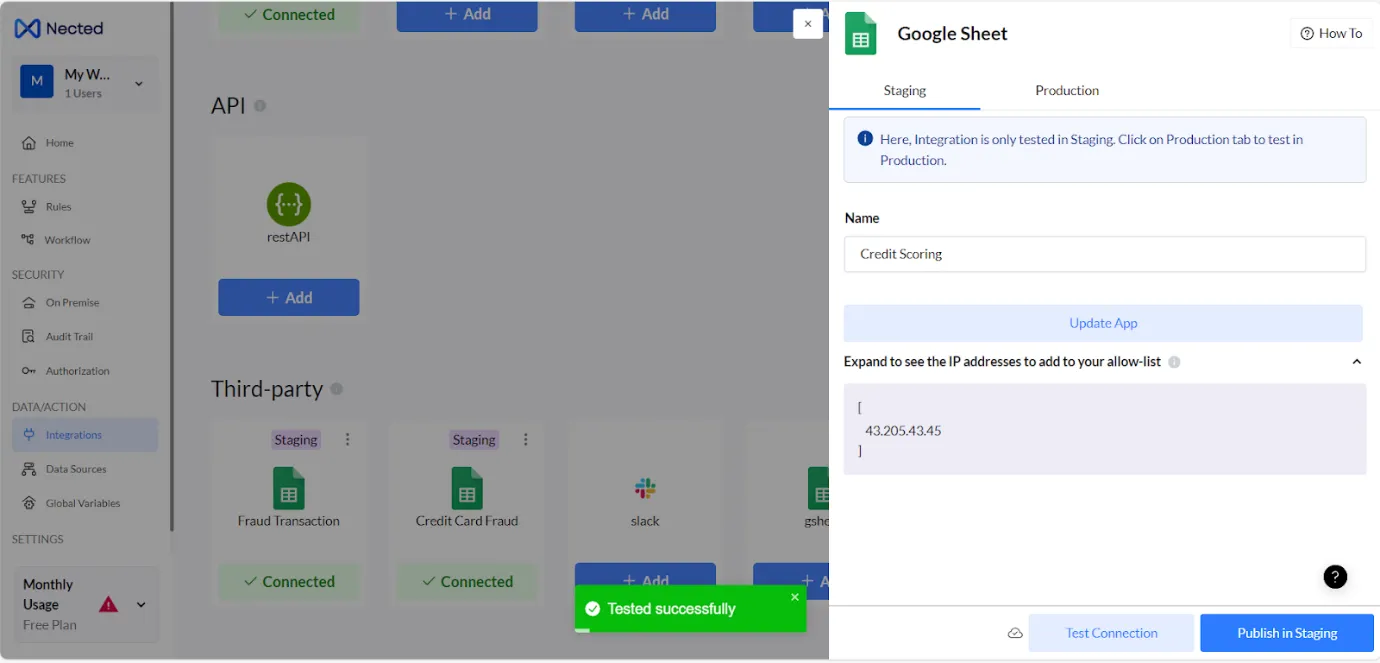

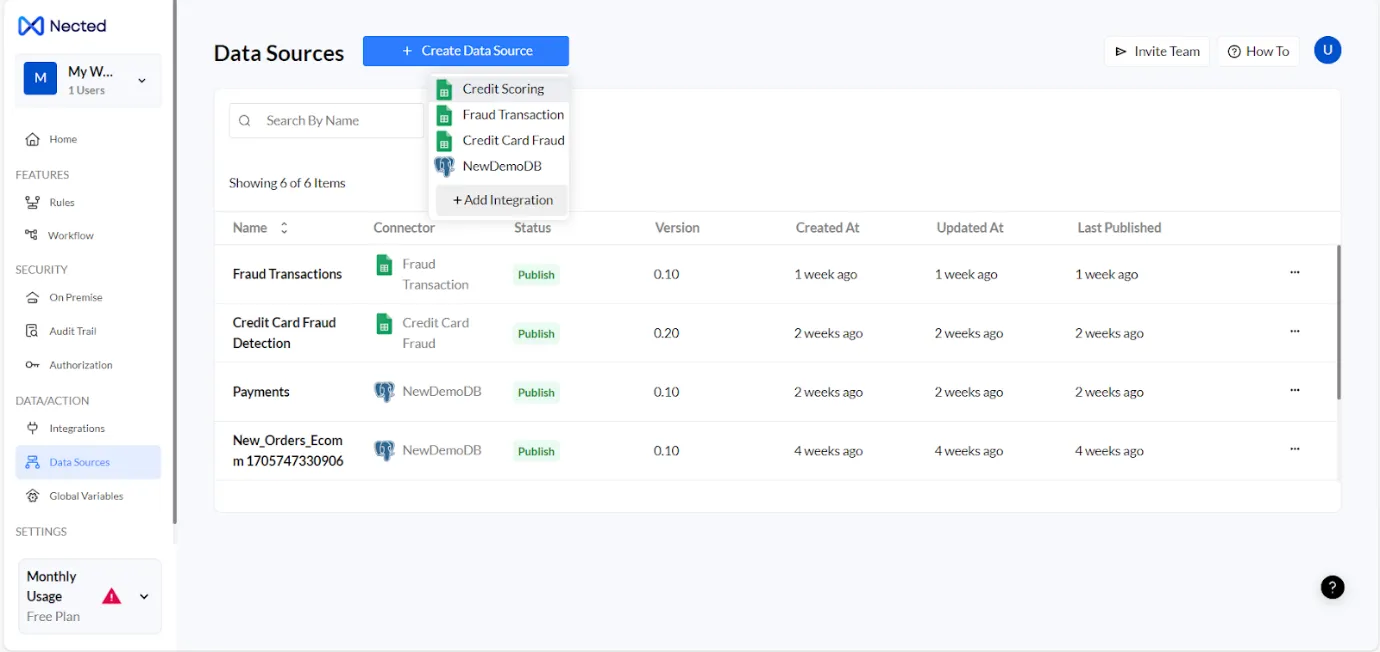

Step 4: Integrating Data

Effortlessly incorporate a range of data streams into Nected. Whether it's financial records, payment patterns, or other pertinent details, Nected supports diverse data types, guaranteeing a holistic approach to credit evaluation.

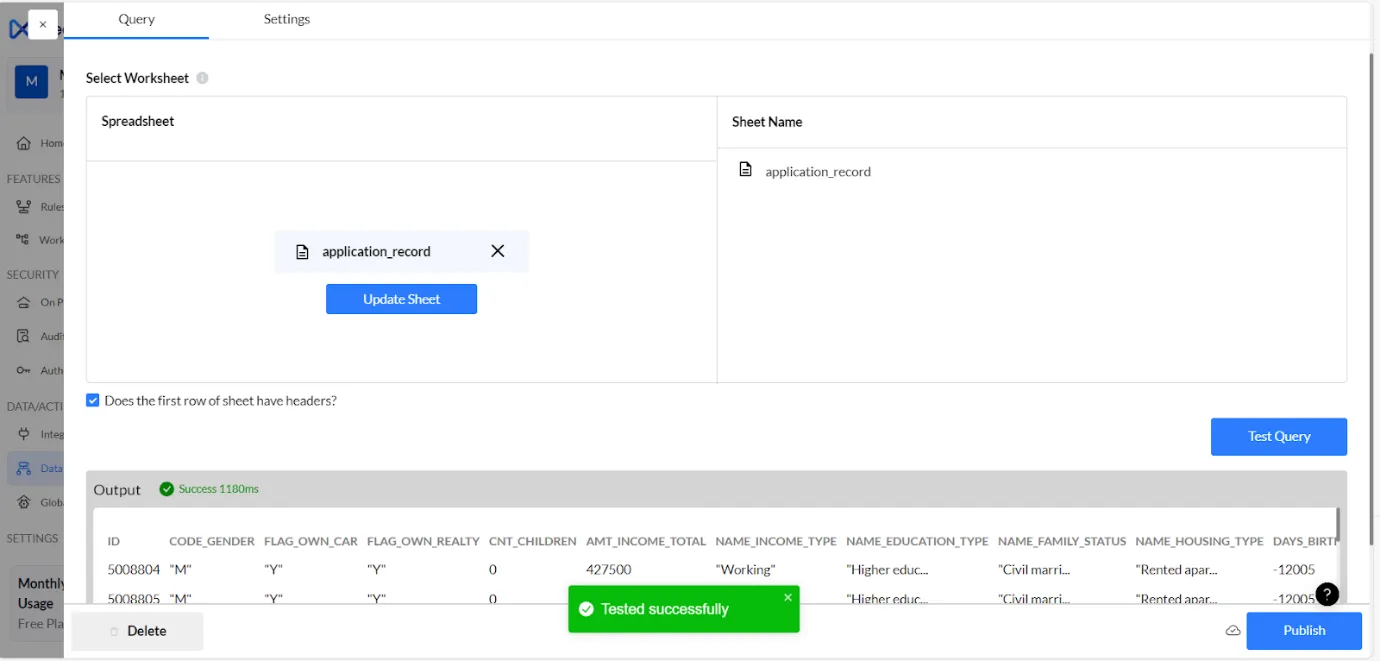

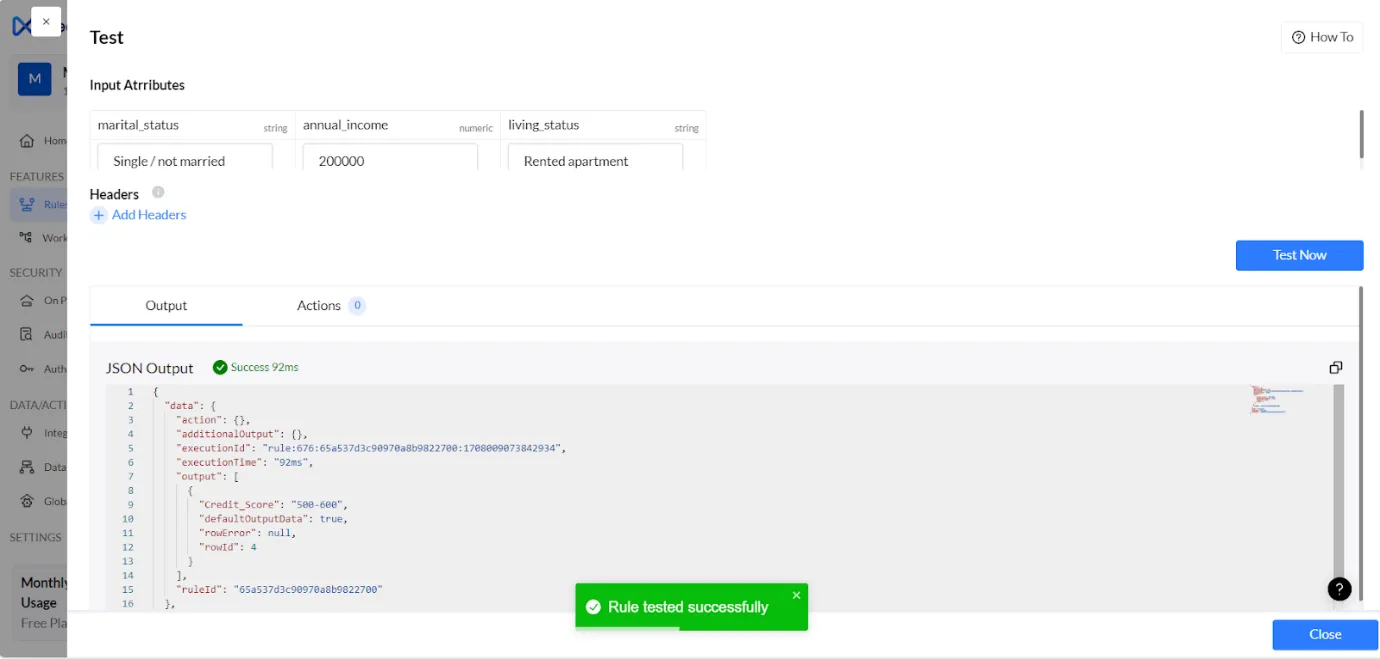

Step 5: Testing and Validation

Evaluate the credit scoring model in Nected by utilizing data. Verify the model's precision and dependability to ensure it conforms to anticipated results.

Step 6: Deployment

After completing the testing phase to your satisfaction, smoothly implement your credit scoring model using Nected. The platform's deployment features guarantee a quick shift from development to real-world application.

Watch this video to get more deeper insights on creating credit scoring rules with Nected.

Building Credit Scoring Systems: Using Nected's Rule Engine and Workflow Automation

Credit Scoring Challenges and Nected Solutions

Challenges:

- Privacy & Security: Credit scoring raises concerns about protecting sensitive financial data from breaches and misuse.

- Bias & Discrimination: Algorithms could perpetuate unfairness towards specific groups if not carefully designed.

- Data Quality: Missing or inaccurate information can impact scoring accuracy and fairness.

Nected Solutions:

- Data Safety: They prioritize data privacy and security through robust measures.

- Fairness: Nected.ai's algorithms are designed to minimize bias and discrimination.

- Data Integration: They integrate with tools to improve data quality and availability.

Real-World Impact:

- Auto Financing: Credit scores influence loan terms and eligibility for car purchases.

- Telecommunications: They impact access to phone plans and services.

- Utilities: Credit scores can affect security deposits for utilities like electricity.

Problem-Solving Power:

- Risk Reduction: Credit scoring helps businesses, especially lenders, avoid risky loans and defaults.

- Faster Decisions: It speeds up loan applications and improves customer experience.

- Smarter Portfolio Management: Banks can manage risk better by diversifying portfolios based on credit scores.

Remember: Credit scoring is a powerful tool for both businesses and individuals, but it needs to be handled responsibly and ethically.

Conclusion

By streamlining complex processes, enhancing decision-making capabilities, and improving risk assessment, Nected credit scoring method has transformed the way financial institutions and lenders approach credit scoring. The future of credit scoring with Nected is bright, with the platform's customizable solutions and commitment to data privacy and security paving the way for more accurate and efficient credit assessments.

By leveraging Nected innovative technology, financial institutions and lenders can make informed decisions about extending credit, reducing the risk of default and non-payment, and promoting financial stability and economic growth.

FAQ’s

Q1. What are the limitations of credit scoring?

Credit scoring does not provide an estimate of a borrower's default probability. It merely assesses a borrower's riskiness from highest to lowest. As such, credit scoring suffers from its inability to determine whether Borrower A is twice as risky as Borrower B. Another interesting limit to credit scoring is its inability to explicitly factor in current economic conditions

Q2.How does credit scoring affect financial inclusion?

Credit scoring can improve financial inclusion by providing lenders with a more comprehensive view of an individual's financial health, potentially benefiting those with limited credit history. However, it's essential to ensure that credit scoring methods are fair and inclusive, and that they do not perpetuate historical biases

Q3. How does credit scoring affect risk assessment?

Credit scoring significantly influences risk assessment by providing lenders with a numerical representation of an individual's creditworthiness. A higher credit score indicates a lower risk of default, making it more likely for lenders to approve loans with favorable terms. Conversely, a lower credit score suggests a higher risk, potentially leading to loan denials or higher interest rates. By incorporating credit scores into their risk assessment processes, lenders can make more informed decisions, mitigate potential losses, and maintain a balanced portfolio.

.svg.webp)

.webp)

.jpg)

%20Medium.jpeg)

%20(1).webp)