.png)

.webp)

Credit scoring refers to the process of evaluating an individual's creditworthiness based on their financial history and behavior. This evaluation results in a numerical score, known as a credit score, which is used by lenders to assess the risk of lending money or extending credit to that individual.

In today's world, your credit score plays a big role in many financial decisions, like getting a loan or credit card. But how exactly is this score calculated? It can seem complicated and confusing, making it hard to know how to improve it. Let us guide you through the modern credit process! We'll break down the credit scoring process into simple steps, so you can understand how it works.

We'll also introduce you to Nected, a tool that can help businesses simplify this process and make better decisions.

What is the Credit Scoring Process ?

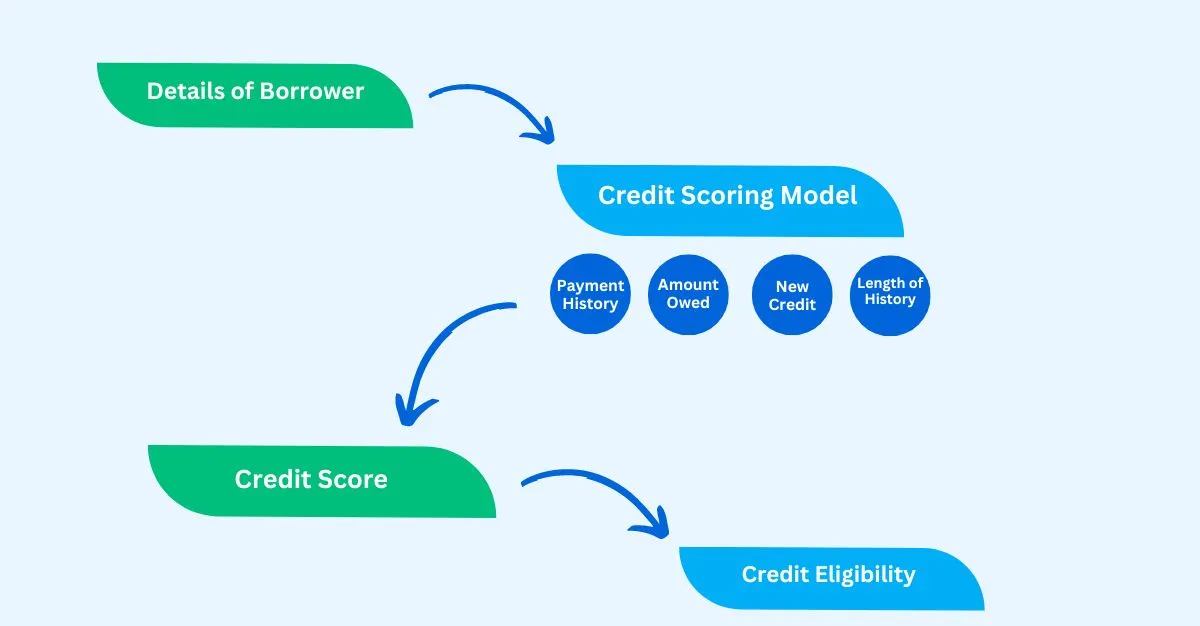

The credit scoring process is a statistical method used by lenders to assess your creditworthiness, or how likely you are to repay a loan. Understanding the credit scoring process and actively managing one's credit can help individuals secure better financial opportunities and access to various products and services in the market.

The process of credit scoring involves the use of statistical analysis by lenders and financial institutions to determine the creditworthiness of individuals or businesses. Credit scoring is based on various factors that influence a borrower's ability to repay a loan. These factors include:

- Payment history (35% for FICO, 40% for VantageScore): This refers to the borrower's track record of making timely payments on debts. Late or missed payments can negatively impact the credit score.

- Amounts owed (30% for FICO, 20% for VantageScore): This factor considers the total amount of debt a borrower has and the portion of their available credit that is being used. High credit utilization rates can lower the credit score.

- Length of credit history (15% for FICO, 21% for VantageScore): The longer a borrower has had credit, the higher their credit score is likely to be. This factor reflects the borrower's experience in managing debt.

- Credit mix (10% for FICO, 5% for VantageScore): This factor assesses the types of credit a borrower has, such as installment loans (like mortgages and car loans) and revolving accounts (like credit cards and lines of credit).

- New credit (10% for FICO, 5% for VantageScore): This factor takes into account recent credit inquiries and the number of new credit accounts a borrower has opened.

Credit scoring models, such as FICO and VantageScore, use these factors to calculate a credit score, which ranges from 300 to 850 for FICO and 300 to 850 for VantageScore. The higher the credit score, the better the borrower's creditworthiness is perceived, which can lead to better loan terms, such as lower interest rates.

Credit scoring is used in risk-based pricing, where the terms of a loan are based on the probability of repayment. Lenders use credit scoring to assess the risk of lending to a borrower and to determine whether to extend or deny credit. A borrower's credit score can impact their ability to qualify for financial products, such as mortgages, auto loans, credit cards, and private loans.

Challenges in the Credit Scoring Landscape

Despite its effectiveness, the credit scoring process is not without its challenges. These can lead to inaccurate assessments and limit access to financial products for certain individuals. Here are some key concerns:

- Inaccurate Reporting: Errors and inconsistencies in credit reports can significantly impact credit score which may disturb lending decisions. These may arise from human error, outdated information, or even identity theft. It's crucial to regularly review the data for such discrepancies and dispute any inaccuracies promptly.

- Lack of Credit History: Individuals with limited or no credit history, such as young adults or immigrants, may struggle to obtain a score. This can hinder their access to loans, housing, and other financial opportunities. Alternative data sources, such as rent payment history and utility bills, can help establish creditworthiness for these individuals, but their adoption is still evolving.

- Economic Factors: External factors beyond your control, like economic downturns or industry-specific recessions, can impact your credit score. For example, widespread job losses might lead to missed payments or defaults, negatively affecting borrowers' scores despite their past responsible credit behavior. These factors highlight the need for a nuanced understanding of your financial situation when evaluating creditworthiness.

Step-by-Step Implementation of Modern Credit Scoring Models Using No Code Tool

Let’s see the credit scoring process using Nected, a No-code tool:

1. Initiation:

Log in to the Nected's platform to initiate a modern credit scoring model.

2. Project Setup:

Create a new rule focused on building a credit scoring model.

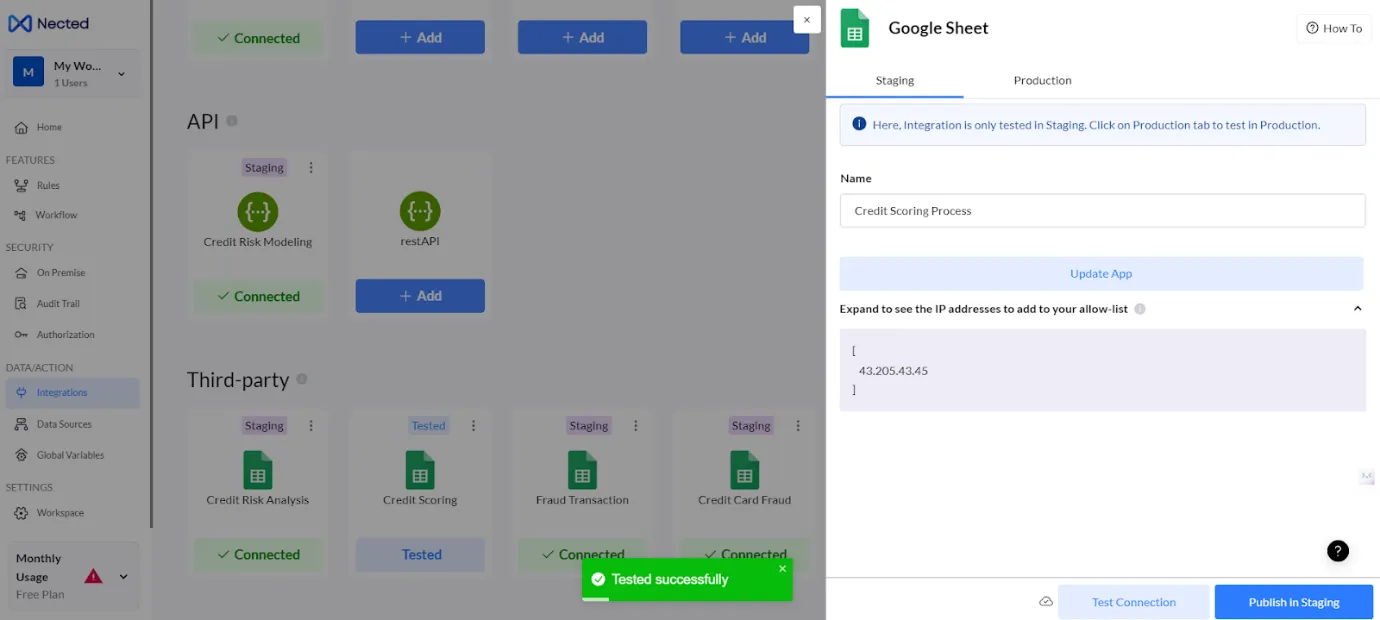

3. Data Integration:

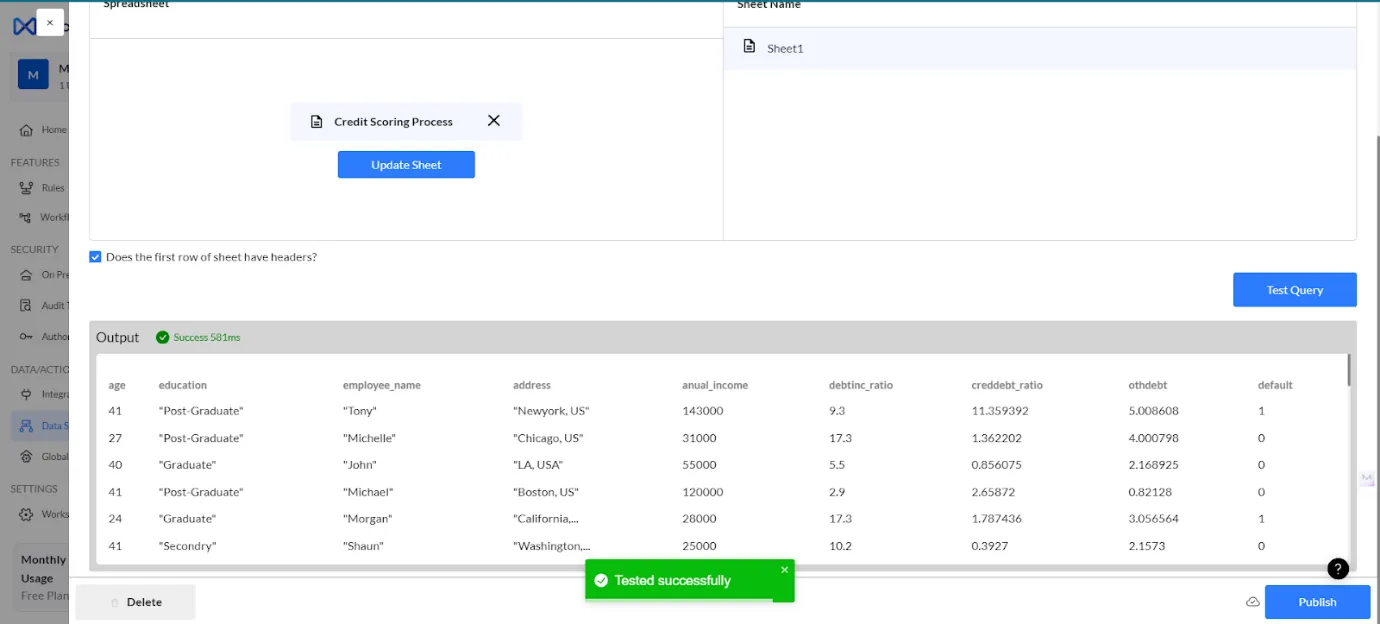

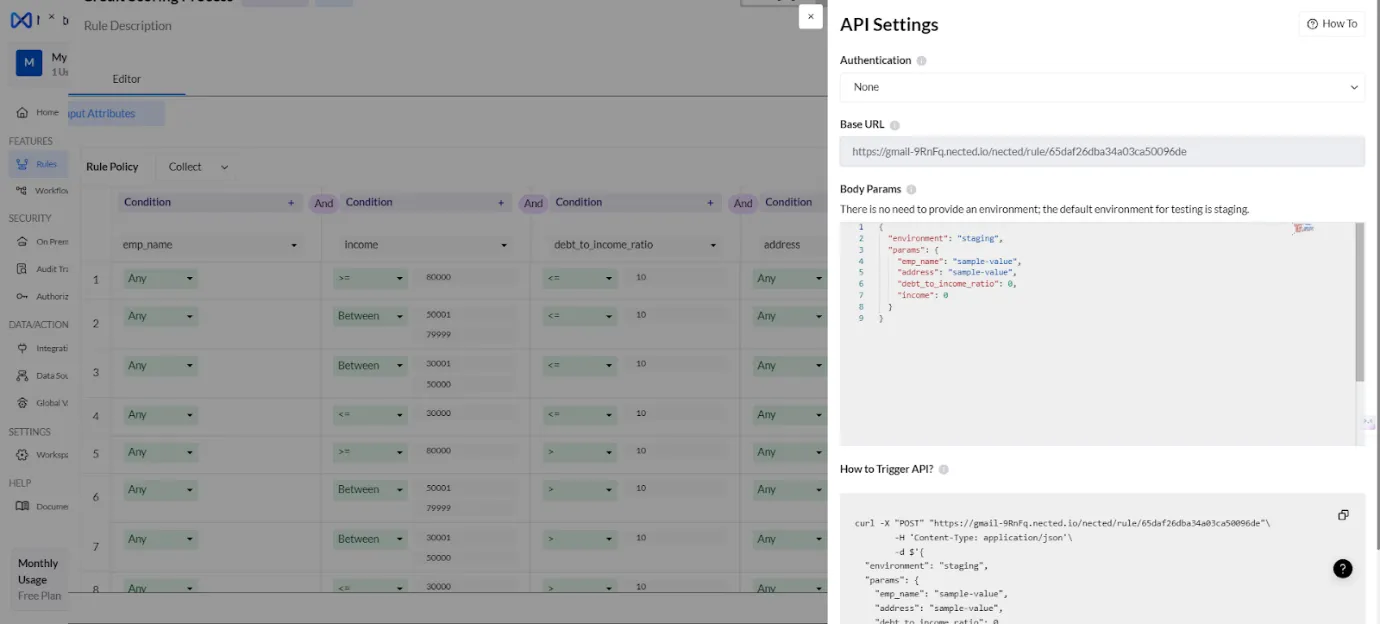

Nected offers a versatile data integration system that allows you to connect with various sources to gather relevant information for your credit scoring model. You can easily assemble relevant data for analysis, including payment history, credit utilization, and credit history length.

After integration, the collated data can be used further in building the system.

4. Model Building:

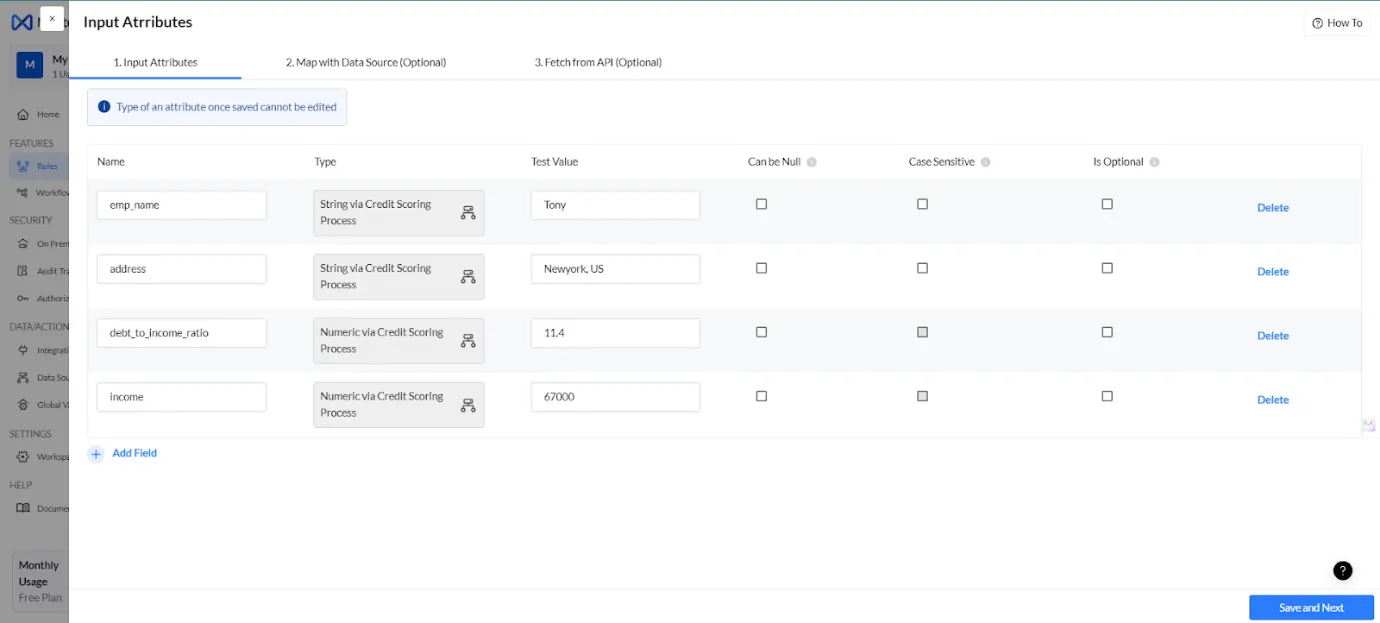

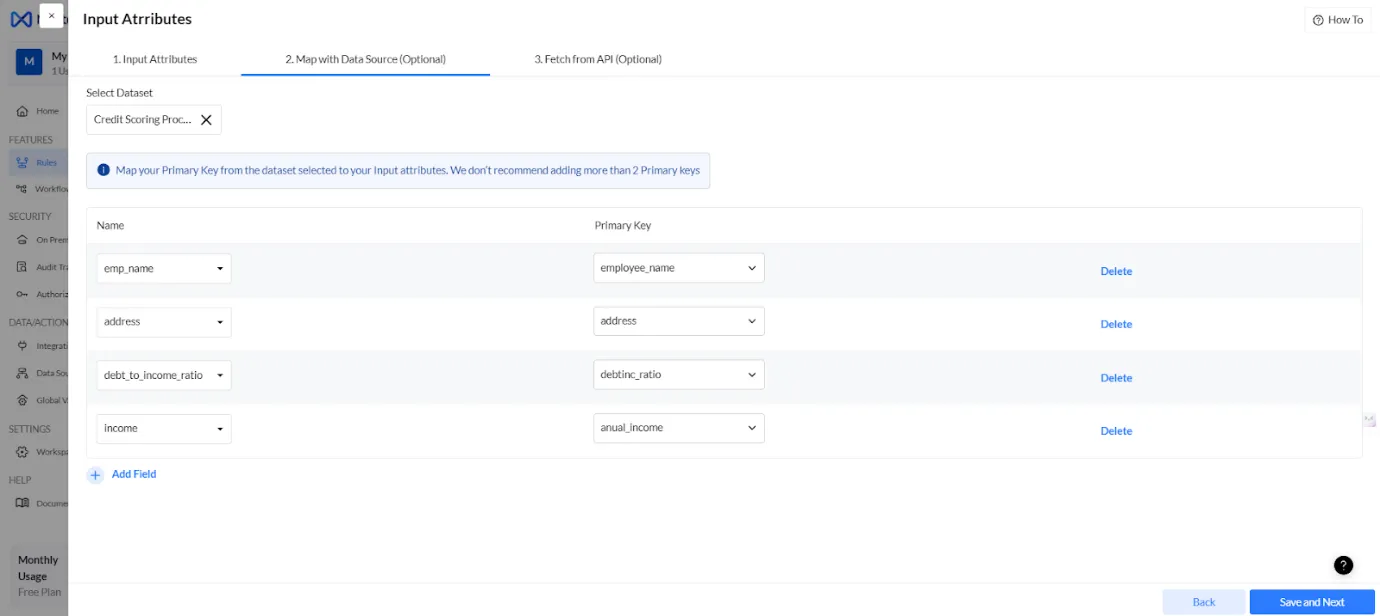

Utilize the platform's rule-based system to construct a credit scoring model. Define rules based on credit rating process steps and the gathered data points such as payment history, credit utilization, and length of credit history.

Set Input attributes according to your specific requirements.

The platform's user-friendly interface allows you to create these rules without needing extensive coding knowledge.

This approach enables the creation of customized credit scoring models tailored to specific needs.

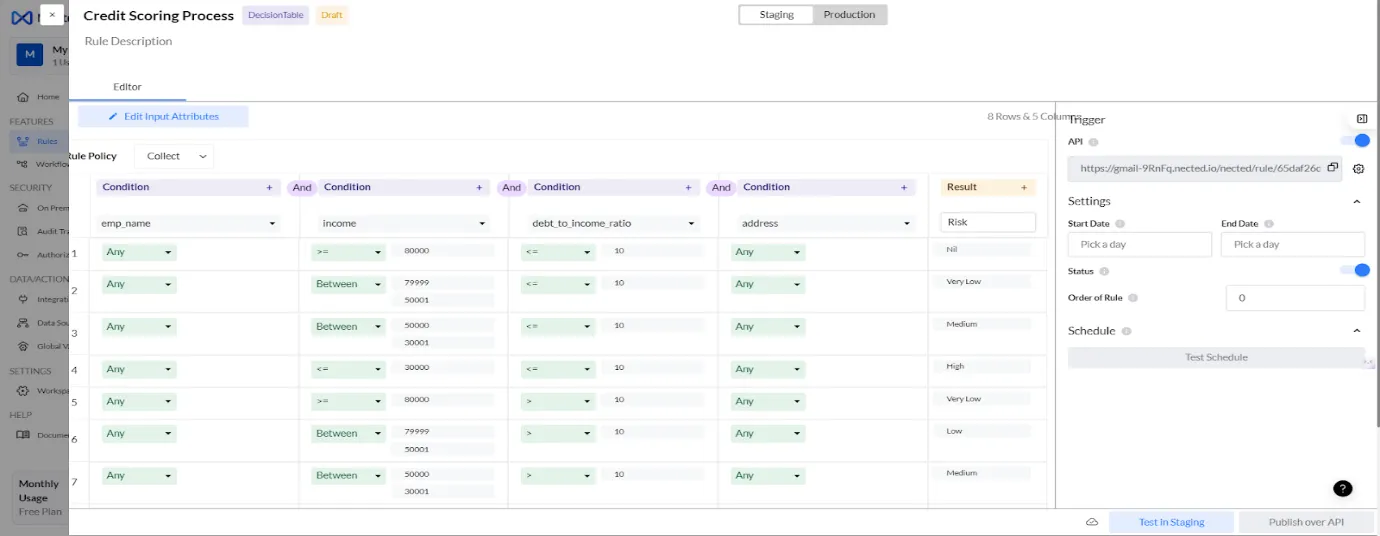

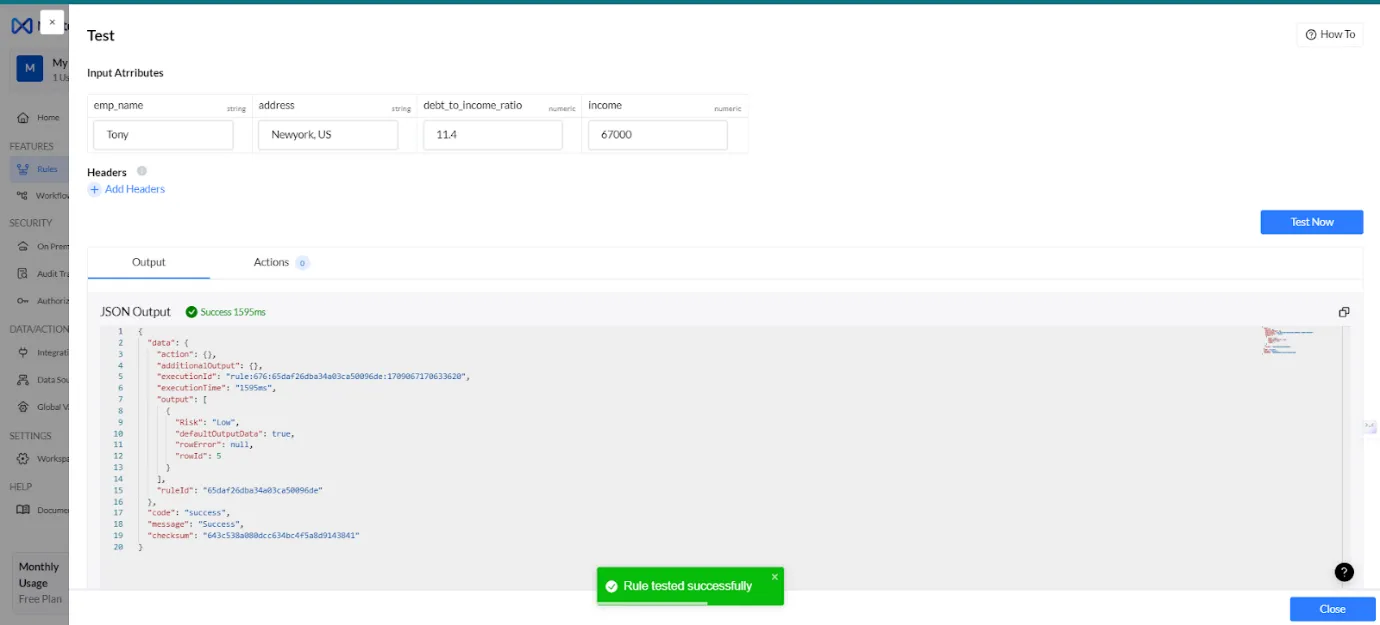

5. Evaluation and Refinement:

Test the developed model within the platform to assess its accuracy and reliability. Ensure the model effectively predicts creditworthiness and delivers valuable insights.

This testing phase allows for identifying and correcting any potential issues or inaccuracies in the model, guaranteeing it delivers accurate results and provides valuable support.

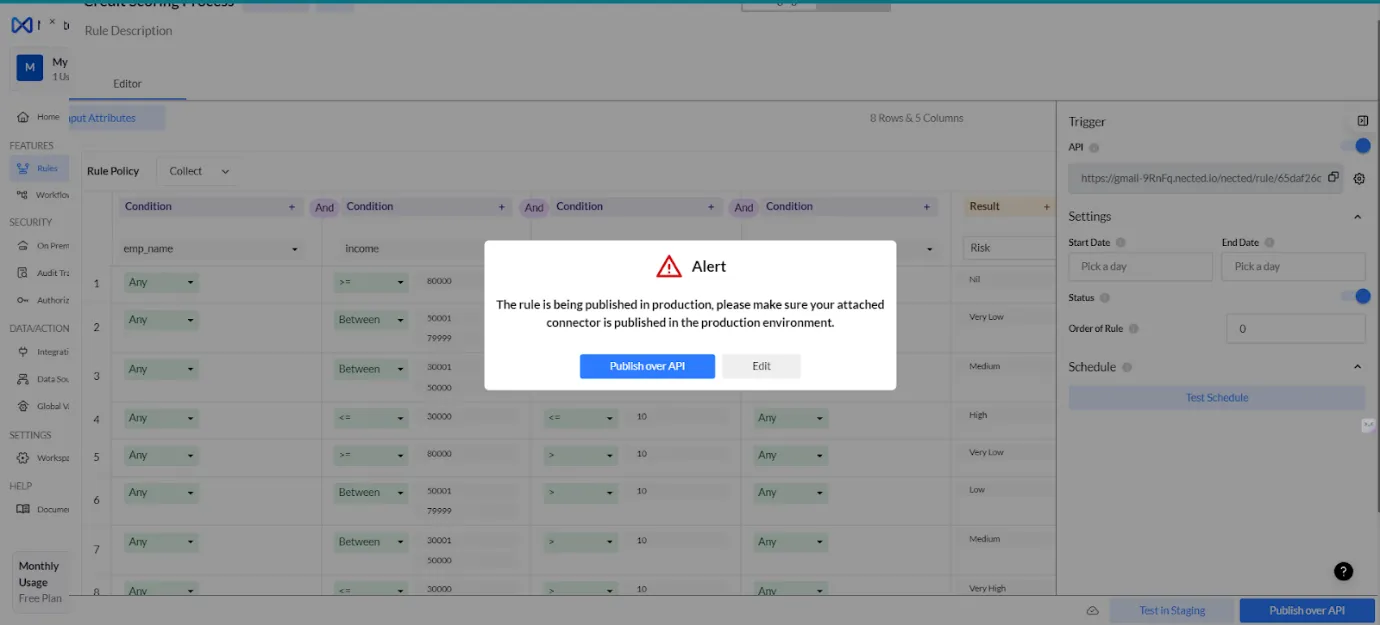

6. Deployment:

Once satisfied with the model's performance, deploy it seamlessly using the platform's deployment capabilities. This ensures a smooth transition from development to practical application, allowing the model to be readily used for credit scoring purposes.

Publish the rules in production with just a click.

By following these steps, you can leverage Nected's no-code/low-code approach to seamlessly integrate various data sources into your credit scoring model. This allows you to create a more comprehensive and nuanced assessment of borrower creditworthiness.

How does Nected successfully address various challenges?

Nected offers a comprehensive suite of tools to streamline and empower your credit scoring process.

Here's how Nected tackles the challenges commonly faced by businesses:

- Seamless Data Integration: Nected eases the process of data gathering, eliminating data acquisition and integration hurdles. Additionally, Nected offers a smooth integration process ensuring compatibility with your existing CRM or ERP systems.

- Automated Decision Logic: You can design and configure automated decision rules within Nected's platform for consistent and swift credit assessments.

- Continuous Monitoring & Compliance: Nected allows for continuous monitoring of your custom models' performance, supporting ongoing refinement to ensure optimal accuracy and adherence to regulations like the Fair Credit Reporting Act (FCRA) and Equal Credit Opportunity Act (ECOA).

- Deployment and Expertise: Nected simplifies deployment by providing support for your development teams. It also addresses the challenge of finding specialized talent by offering an intuitive platform with a minimal learning curve.

- Cost-Effective Cloud Solution: Nected eliminates the high costs associated with traditional credit scoring system development, making it accessible for businesses of all sizes. Cloud-based deployment further reduces infrastructure expenses.

- Ethical Framework: Nected prioritizes ethical considerations by establishing clear guidelines for data privacy, mitigating bias, and ensuring model transparency through regular audits.

These challenges are easily overcome by Nected through strategies like seamless integration and full control over data, audit trail, providing easy integration, least learning curve, easy management, and establishing ethical guidelines for credit scoring models.

Conclusion

In conclusion, you wandered over the various technicalities involved in the modern credit scoring process and also the factors affecting the credit scoring process. You also saw the challenges posed during the process and how Nected addresses those challenges easily. Credit scoring plays a crucial role in the financial assessment process, and selecting the right solution is essential for businesses.

Nected emerges as a frontrunner in this domain, offering a low-code, no-code rule engine that empowers businesses with flexibility, adaptability, and a user-friendly interface. Nected’s ability to address credit scoring complexities and its innovative approach makes it an optimal choice for businesses seeking a reliable and efficient credit scoring platform.

FAQ’s

Q1. Which factors have an impact on credit scores?

Your payment history holds the weight when calculating a credit score, followed by your credit utilization rate, length of credit history, variety of credit accounts held, and recent inquiries made.

Q2. Is there a distinction between a credit score and a credit report?

Indeed, your credit score is a condensed figure derived from the details in your credit report. The report provides an overview of your borrowing history, including accounts, repayment patterns, and outstanding debts.

.webp)

.svg.webp)

%20Medium.jpeg)

%20(1).webp)