.png)

.webp)

Credit scoring is a big part of lending now. Banks, fintech apps, insurers, even some retail and telecom teams rely on it to decide who gets credit and on what terms. The core idea is simple enough. The execution is where things usually break.

Nected fits into this space as a modern credit scoring platform built for teams that want more control without building everything from scratch. It handles rule-based scoring, works with different data sources, and gives businesses a practical way to move faster than old-school credit systems.

This post walks through credit scoring, where it’s used, what it solves, and how Nected fits into the picture.

Exploring Credit Scoring

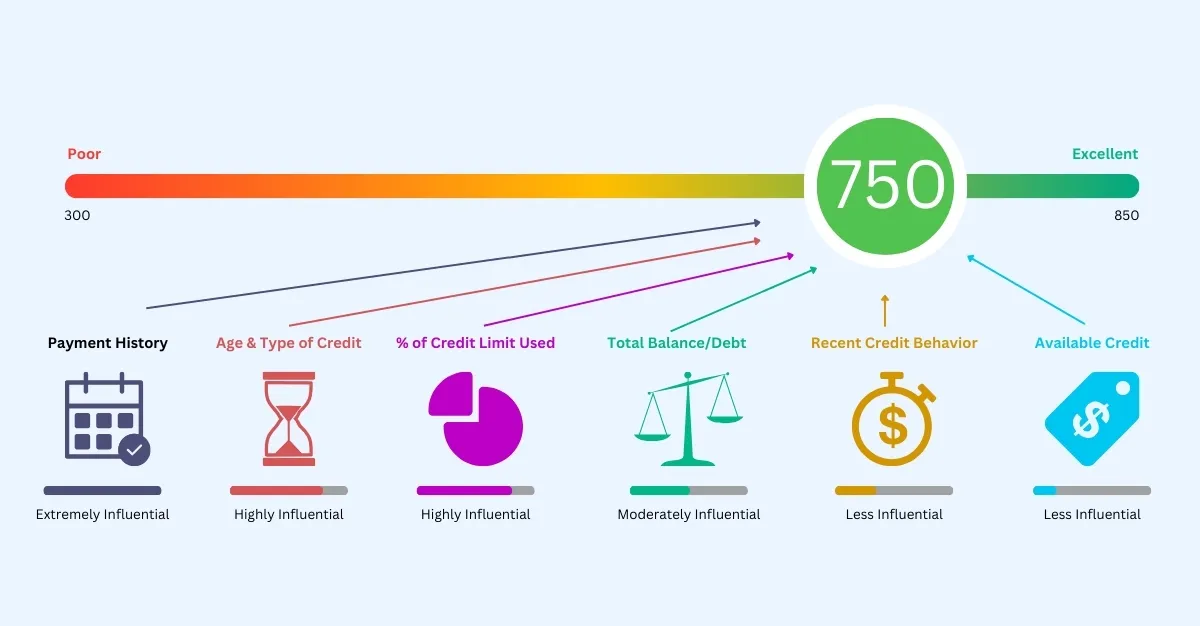

Credit scoring is a method financial institutions use to judge creditworthiness. It looks at different signals and turns them into a score. Lenders use that score to make decisions faster, and with a bit more consistency.

Significance in Financial Assessments

For lenders, this is the backbone of the decision process. A credit score gives them a quick read on risk. Not perfect, but useful. It helps separate low-risk applicants from the ones that need a closer look.

Types of Credit Scoring

Credit scoring comes in a few forms. The two common ones are:

- Generic Credit Scoring: Uses a standard set of rules for a wide group of people or businesses.

- Custom Credit Scoring: Built for a specific industry or use case. This one usually matters more when the default model doesn’t fit well.

Primary Components of Credit Scoring

Most credit scoring models use the same basic ingredients:

- Payment History: Whether someone pays on time.

- Credit Utilization: How much of their available credit they’re using.

- Length of Credit History: How long their accounts have been open.

- Types of Credit in Use: The mix of credit products they have.

- New Credit: Recent inquiries and new account activity.

That’s the usual base. Some models go further and look at recent behavior, available credit, or industry-specific signals. This part often gets ignored, but it matters a lot when you want a score that reflects real usage instead of just a generic profile.

How Your Credit Score Is Calculated?

A credit score is usually built from a weighted mix of factors. Different models weight them differently, but the logic stays mostly the same:

- Payment History: Missed payments and on-time payments.

- Credit Utilization: How heavily credit lines are used.

- Length of Credit History: How long the borrower has been active.

- Types of Credit in Use: Cards, loans, and other account types.

- New Credit Inquiries: Recent applications for new credit.

Some platforms, including Nected, let businesses customize these inputs. That helps when a standard model doesn’t match the way a specific business actually evaluates risk.

Credit Scoring Approaches Guidelines

Different businesses need different scoring setups. The two common approaches look like this:

- Generic Credit Scoring:

- Overview: A standard model used across a broad audience.

- Pros: Fast to set up, cheaper to run, and easy to apply at scale.

- Cons: Can miss the details that matter in niche or complex cases.

- Custom Credit Scoring:

- Overview: A tailored model that uses business-specific rules and data.

- Pros: More precise, more flexible, and usually better for specialized lending.

- Cons: Takes more time and more work to build well.

Nected supports both. That gives teams room to start simple and move toward custom rules when the use case calls for it.

Industries and Functions Leveraging Credit Scoring

Credit scoring shows up in more places than people expect. Finance is the obvious one, but it’s not the only one.

- Banking and Finance:

Banks use credit scores to decide on loans, credit cards, and other lending products. It keeps approvals faster and helps cut down on bad debt.

- Insurance:

Insurers use credit-based scoring to estimate risk and set premiums. In some markets, that can change what a customer pays by a lot.

- Retail:

Retailers use it for store credit, installment plans, and account limits. It’s usually less about prediction and more about not overextending the customer.

- Real Estate:

Mortgage lenders rely on credit scores to assess buyers. A stronger score can mean better rates and fewer hurdles.

- Employment Screening:

Some employers check credit history for roles that involve money handling or sensitive financial access. Not every role, obviously. But in the right context, it’s part of the screen.

Real-world Examples

- Auto Financing: Car dealers use credit scores to judge loan eligibility and pricing.

- Telecommunications: Mobile providers may use it to decide between postpaid and prepaid plans.

- Utilities: Some utilities use it when deciding whether to ask for a deposit.

These examples show how widely the model gets used. Different industry, same basic problem: how much trust should you extend up front?

Read Also: Understand Credit Scoring Methods And Unlock Your Financial Success

What Problems Does Credit Scoring Solves?

Credit scoring is really a risk filter. It helps companies make better calls without dragging every decision through manual review.

Business-End Problems

- Risk Mitigation: It helps lenders reduce defaults by flagging risky applicants early.

- Efficient Decision-Making: Loan decisions move faster when there’s a score to work from.

- Portfolio Management: Banks can spread exposure across different risk bands instead of guessing.

Customer-Centric Issues

- Access to Credit: Applicants get a clearer path to approval when the process is standardized.

- Fairness and Objectivity: Scores reduce the randomness that comes with manual judgment.

- Interest Rates and Terms: Better scores often mean better pricing.

So the system helps both sides. Lenders get control. Customers get faster decisions, and often a cleaner path to better terms.

Core Technicalities of Credit Scoring Implementation

Once you get past the concept, the technical setup matters a lot more than people expect.

Key Parameters and Considerations

- Credit Score Range: Know what a high or low score actually means.

- Weightage of Factors: Some inputs matter much more than others.

- Scalability: The model should hold up when application volume spikes.

- Regulatory Compliance: The logic has to stay transparent and defensible.

That’s the part teams often underestimate. A scoring model can look fine in testing and still fail in production if the data flow, rules, or compliance layer isn’t solid.

Top 5 Credit Scoring Platform & Tools in 2026

Credit scoring tools aren't all doing the same thing. Some are fixed models — you send data, you get a score. Others are full analytics platforms built for enterprise risk teams. A few are flexible enough to let you define your own scoring logic entirely. Which one makes sense depends on what you're actually trying to build and how often your rules change.

Here's a practical look at the five worth knowing in 2026.

1. Nected

Nected is a low-code/no-code decision management platform that works well as a credit scoring engine when you need custom scoring logic, fast rule changes, and clear visibility into how decisions are being made. It's not a bureau-style scoring product — it's a platform for building and managing your own scoring workflow.

The practical advantage is speed. When underwriting rules change — and in lending, they change often — teams don't need to wait on a development cycle. Business users can update logic directly. Developers stay focused on actual engineering work.

Key Features:

- Rule-based scoring workflows with visual rule editor

- Low-code and no-code setup — accessible to non-technical teams

- Custom input attributes for scoring logic

- Multiple data connectors and API integrations

- Built-in testing and validation before deployment

- Rule chaining for multi-step credit decisioning

- Version control and audit trails

- Real-time rule execution with low latency

- Cloud and self-hosted deployment options

Use Cases:

- Custom loan approval workflows

- Fintech lending decisioning

- Behavioral and alternative credit scoring

- Underwriting logic management

- Credit risk tiering

Pros:

- Faster setup than building a scoring system from scratch

- Rule changes don't require engineering involvement

- Decision logic is transparent and auditable

- Handles both scoring and workflow automation in one platform

- Scales without adding architectural complexity

- Experimentation support — test rule changes before rolling out

Cons:

- Not a traditional fixed scoring model — requires thoughtful rule design to get good results

- Teams expecting a plug-and-play bureau score will need to adjust expectations

- Advanced features take some time to explore fully

Nected is the strongest fit when the goal is building or managing a custom credit scoring workflow rather than consuming a fixed score. For teams where scoring logic is a moving target, it's hard to beat on flexibility and iteration speed.

2. FICO Score

FICO is probably the most recognized name in credit scoring globally. Lenders use it as a standard reference. Regulators understand it. Consumers have heard of it. That familiarity carries real weight in traditional lending contexts.

The model itself is well-established — built on payment history, utilization, credit history length, account mix, and recent inquiries. It doesn't change often, which is both its strength and its limitation.

Key Features:

- Well-established, widely validated scoring model

- Standardized risk evaluation across lenders

- Strong historical credibility and lender adoption

- Used as a benchmark in most traditional credit decisions

Use Cases:

- Consumer lending decisions

- Mortgage underwriting

- Credit card approvals

- Benchmark reference for risk tiering

Pros:

- Trusted and recognized by financial institutions

- Easy to interpret and explain in lending contexts

- Useful as a common benchmark across systems

- Regulatory familiarity — less friction in compliance conversations

Cons:

- Very limited customization — the model is what it is

- Not useful when a business needs tailored or alternative scoring rules

- Slow to adapt to changing borrower profiles or new data types

- Doesn't work for thin-file or new-to-credit populations where bureau data is sparse

FICO is solid when you need a known, trusted reference score. It's the wrong tool when your business needs scoring that can adapt to specific use cases or change with market conditions.

3. Experian Decision Analytics

Experian Decision Analytics is more of a decisioning and analytics platform than a simple scorecard. It's aimed at lenders who need broader risk modeling, data-driven credit decisions, and integration with Experian's underlying credit data. This is where things usually get heavier in terms of implementation.

Key Features:

- Credit risk analytics with custom model support

- Decisioning workflows integrated with credit data

- Scorecard development tools

- Access to Experian's bureau data

- Strategy management for credit decisioning

Use Cases:

- Advanced credit risk modeling for established lenders

- Portfolio risk management

- Multi-bureau decisioning workflows

- Regulatory stress testing

Pros:

- Strong analytics capabilities for complex credit environments

- Useful for organizations already working deep in credit data

- Custom model support gives more flexibility than a fixed score

- Integration with Experian's data assets

Cons:

- Implementation tends to be heavy — not a quick setup

- Requires analytics expertise to configure well

- Less approachable for smaller or faster-moving teams

- Can feel like more platform than you need for straightforward scoring

Makes sense when analytics depth is genuinely needed. For teams that mainly want faster rule changes and cleaner workflow control, it's usually more than the situation calls for.

4. Equifax Ignite

Equifax Ignite is built around credit risk assessment using large-scale data and enterprise-grade infrastructure. The main draw is data breadth — Equifax's underlying data assets combined with analytics tooling designed for high-volume decisioning environments.

Key Features:

- Big-data credit risk assessment at scale

- Data integration across multiple sources

- Real-time and near-real-time decisioning capabilities

- Risk analytics tooling for enterprise environments

- Access to Equifax's bureau and alternative data

Use Cases:

- Enterprise-scale lending operations

- Real-time credit decisioning for high-volume portfolios

- Multi-source data integration for risk models

- Large financial institutions with complex data environments

Pros:

- Strong for organizations with serious data scale needs

- Real-time decisioning infrastructure

- Broad data coverage across bureau and alternative sources

- Enterprise-grade reliability

Cons:

- Complex to implement — this part often gets underestimated

- More platform than most teams need for simpler scoring use cases

- Less flexible than a rule-first approach when business logic changes frequently

- Smaller teams generally don't need this much machinery

Equifax Ignite makes sense when the operation is already large and the data stack is serious. For anything below that scale, it tends to be more infrastructure than the problem requires.

5. CreditVidya

CreditVidya focuses on alternative credit scoring — specifically for markets where traditional bureau data is thin, incomplete, or simply doesn't exist for a large portion of the population. It's a specialized tool solving a specific problem.

In markets like India, where a significant portion of potential borrowers have little or no credit history, bureau scores don't tell the full story. CreditVidya uses alternative data signals to build risk profiles for thin-file and new-to-credit customers.

Key Features:

- Alternative data-based credit scoring

- Underwriting support for thin-file borrowers

- Risk assessment models designed for limited bureau data environments

- Useful for new-to-credit and underserved customer segments

Use Cases:

- Lending in emerging markets with limited bureau coverage

- New-to-credit customer onboarding

- Alternative underwriting for fintech lenders

- Expanding credit access beyond traditional profiles

Pros:

- Solves a real problem that bureau-based tools can't address

- Supports broader credit access for underserved populations

- Relevant for lenders targeting non-traditional borrower segments

Cons:

- Heavily dependent on the quality and availability of alternative data

- Less general-purpose than rule engines or enterprise credit platforms

- May need significant tuning for different lending contexts and markets

- Not the right fit when bureau data is actually available and sufficient

It solves a genuine problem, especially in markets where traditional scoring leaves large populations underserved. Outside of that specific context, it's more specialized than most lending teams need.

Tool Comparison: Nected vs. Alternatives for Credit Scoring

Choosing the right credit scoring tool depends on what you’re actually trying to do. Some teams want a fixed score. Others want to build scoring logic that can change with the business.

The right tool depends on what you're actually trying to do. If you need a fixed benchmark that every lender already understands — FICO. If you're running enterprise analytics at serious scale — Experian or Equifax. If you're serving markets where bureau data is sparse — CreditVidya.

But if the goal is building credit scoring logic you can actually control, update quickly, and audit clearly — without a long implementation cycle or engineering dependency for every rule change — Nected is the cleaner fit.

Conclusion

Credit scoring has moved way beyond a static number. The useful tools now are the ones that can adapt, integrate cleanly, and keep the decision logic understandable. Nected does that well, especially for businesses that want a credit scoring platform they can shape around real operations instead of forcing their process into a rigid model.

Nected gives teams a practical way to build credit scoring workflows that are easier to manage and easier to change when the business changes.

FAQs

Q1. What makes credit scoring essential for businesses?

Credit scoring gives businesses a structured way to judge credit risk. That means better lending calls, fewer bad approvals, and less guesswork.

Q2. Can Nected be customized to suit unique business needs in credit scoring?

Yes. Nected lets teams adjust rules, inputs, and scoring logic based on their own needs. That’s the main reason people use it.

Q3. What are the key factors that influence a credit score?

Payment history, credit utilization, credit history length, types of credit in use, and recent credit inquiries are the main ones.

Q4. How do businesses benefit from using credit scoring models?

They make faster decisions, reduce default risk, and keep the process more consistent. That part often gets ignored, but it matters a lot once volume picks up.

Q5. Can credit scoring models be customized for specific industries?

Yes. That’s often the better move, especially when a generic score doesn’t match the risk pattern in a specific industry.

.svg.webp)

.webp)

.webp)

%252520(1).webp)

%20(1).webp)