.png)

.webp)

If you own a retail business and handle hundreds and thousands of customers regularly, consider implementing credit score practices in your business for accounts receivable, credit, and collection management. This will help make a more effective credit-based decision based on the credit score of an individual or business and also allow you to provide better customer service. In this blog, Let us see how to create and implement the best customizable credit scoring engine B2B System with the help of Nected’s customizable rules engine.

Customizable Credit Scoring Engines B2B System - Overview

A customizable credit scoring engine in a B2B system is a tool or software platform designed to assess the creditworthiness of businesses applying for credit or loans.

Let us break down the components and key factors of customizable credit scoring engines B2B system in further sections.

What is a Credit Scoring Engine in a B2B System?

A credit scoring engine in a B2B system is a software application or platform designed to evaluate the creditworthiness of businesses applying for credit or loans. Platforms like Nected offer multiple rule-based engines for different use cases that help the business to make valuable analyses and effective decisions based on its decision management system.

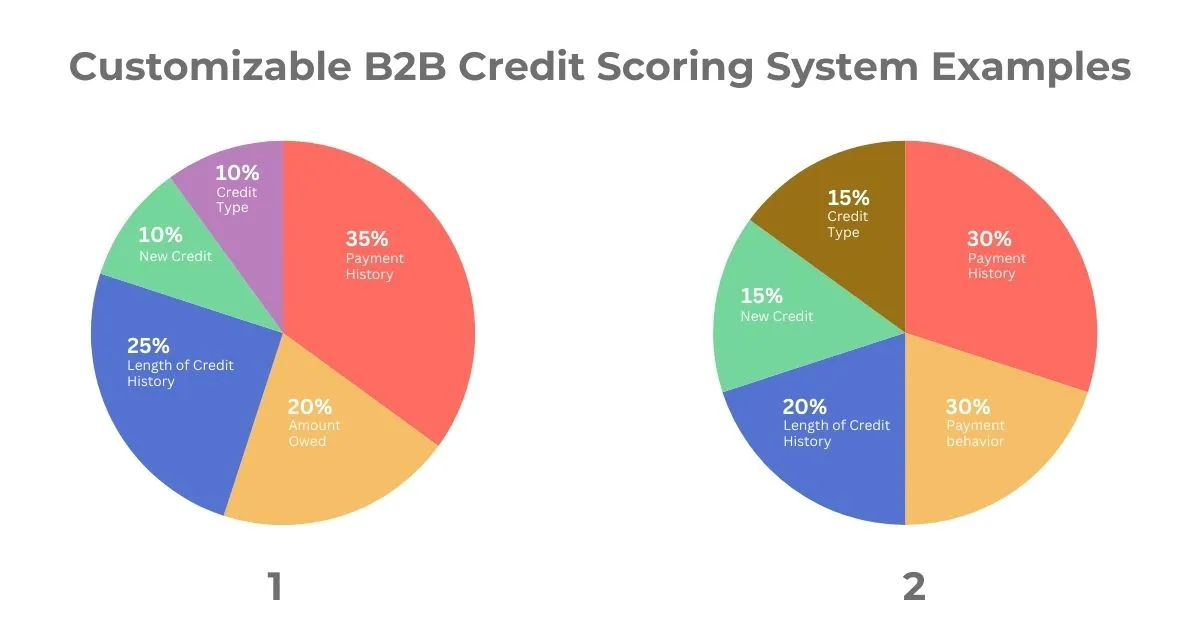

As shown below, Nected’s customizable credit scoring engines B2B system may include factors like the company's financial history, payment behavior, industry trends, new credit, the amount owed, and economic indicators.

In the first pie chart, you can interpret that payment history, length of credit and amount owed play a major role, whereas in the second pie chart we can see that length of credit history and payment behavior are equally considered important. Also, the parameters such as new credit and credit type are given more importance in the second chart whereas in the first chart they are considered only for 10%.

From this, you can infer that each B2B company has their unique implementation ideas for building a credit scoring engine. Nected’s customizable credit scoring engine analyzes various data points related to financial health, payment history, industry trends, and other relevant factors of the business seeking credit.

It generates a credit score or rating that helps lenders or financial institutions make informed decisions about whether to extend credit to the business.

Use cases of Customizable Credit Scoring Engines B2B System

Nected’s customizable credit scoring engine has various use cases, some of which are

- Lending Institutions: Banks, credit unions, and other financial institutions can use customizable credit scoring engines to assess the risk associated with extending credit lines, loans, or other financial products to businesses.

- Trade Credit Providers: Companies that offer trade credit or supplier financing to other businesses can use these systems to evaluate the creditworthiness of their clients and manage credit risk effectively.

- Credit Risk Management: Businesses can utilize customizable credit scoring engines to monitor the creditworthiness of their existing customers, identify potential defaults or delinquencies, and implement proactive risk mitigation strategies.

- Supply Chain Finance: In supply chain finance programs where financial institutions provide financing to suppliers based on the creditworthiness of the buyer, customizable credit scoring engines B2B systems play a crucial role in assessing the risk associated with different parties in the supply chain.

Advantages of Customizable Credit Scoring Engines B2B System

The advantages of customizable credit scoring engines B2B system are

- Nected’s credit score engine improves the efficiency of the credit evaluation process by reducing efforts and speeding the time of decision-making.

- The flexibility of Nected’s rule-based engines allows the business to create a customizable credit score engine based on the specific requirements of the business

- Nected’s rule engines are scalable, they can handle a large number of credit applications at the same time. This reduces the wait time of the applicant.

- Nected’s risk management mechanism identifies and manages credit risk.

Challenges in Traditional B2B Credit Scoring Engine

Traditional B2B credit scoring system engines have various limitations like

- Data availability and quality

- Complex business relationships

- Industry-specific risks

- Lack of customization.

These limitations are mostly because the traditional B2B credit system relies on historical financial data for future creditworthiness analysis. The system fails when numerous credit applications are made at the same time because it does not produce effective results in most cases.

Nected’s rule-based approach helps the business overrule the traditional B2B credit scoring system's limitations. Now let us see how to integrate Nected’s customizable credit scoring engines B2B system.

Read Also: Credit Scoring Python: A Comprehensive Guide

Customizing a B2B Credit Scoring Engine Using Nected

Nected provides a customizable rule engine that can be suitable for any industry making it more adaptable and effective for all kinds of use cases in the business.

Before exploring the customization of the credit scoring engine, let us understand how Nected’s credit scoring engine works. Nected’s rule engine initialization begins with the rule creation. There are predefined rule templates that are already available in the rule engine and can be optimized for specific business requirements; this shows the versatility of Nected’s rule engine.

Consider a scenario where a financial organization tries to identify high-risk business applicants for small business loans. In this scenario, a B2B organization examines the credit score of the business applicants to identify their eligibility for the business loan.

Prerequisites: Before creating a customized rules engine for a specific scenario. Consider these factors

- First, it is important to identify the key metrics of the scenario. This helps to design an effective rule engine that can produce a more accurate outcome

- Once the metrics are identified, gather relevant financial data that allows Nected’s customizable credit score rule engine to produce a credit score.

- The final and important process is to determine the threshold for the applicants. In this scenario, determine the maximum allowable debt-to-income ratio or minimum acceptable credit score for business loan eligibility.

These processes will speed up the entire implementation process of the rule engine and enable you to make better decisions while approving the applicant for the business loan.

After satisfying the prerequisites, the only thing left is to create the customizable credit score engine B2B system. All you have to do right now is define the condition and attribute, feed the data source, and then Nected will handle the rest.

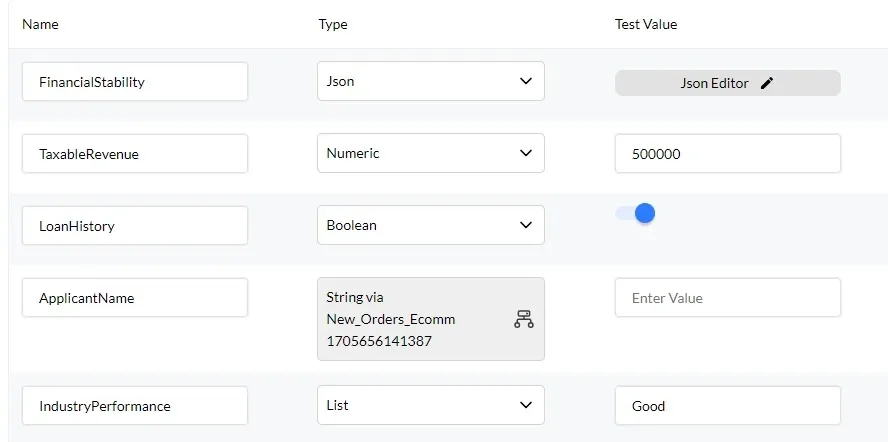

Defining the rule parameter: In this scenario, define the parameters related to identifying the high-risk applicant such as applicant name, financial stability, loan history, industry performance, and taxable revenue. These parameters can be customized in the future based on the requirement.

Customize Rule Logic: Nected’s workflow is flexible because it allows the business to customize the evaluation logic. In this scenario, it is triggering the alerted mechanism for anomalies in the applicant’s financial data such as consistent late payments or declining revenue trends.

Test and Validate: After setting up the rules parameter and rules logic, Nected also allows the business to check the performance of the customized credit score rules engine with the help of customized test data to validate its accuracy in identifying high-risk applicants and ensuring compliance with predefined threshold and the business can adjust rules as needed based on testing outcomes to optimize performance and automate the entire process.

Additionally, It will establish a real-time monitoring system to record the workflow of the customizable credit score engine.

To get an in-depth understanding of how to implement a credit scoring engine. Visit here.

Read Also: Credit Scoring Process - How Credit Scoring Is Done?

Conclusion

In conclusion, the customizable credit scoring engine B2B system using Nected provides many advantages to businesses in different sectors. Businesses can effectively assess companies' creditworthiness, manage risks, and make correct decisions with Nected’s rule-based approach and smooth data integration capabilities. The use cases of Nected’s customizable credit scoring engine are employed in credit institutions, trade credit providers, and credit risk management by showing good variety and applicability in various cases.

Nected solves the problems of traditional B2B credit scoring systems as it provides flexibility and efficient risk management mechanisms. Nected is designed to help businesses optimize the credit evaluation process and make better decisions which allows them to achieve sustainable growth and success in the competitive market.

FAQs

Q1. What is a credit scoring engine?

A credit scoring engine is a software system that evaluates an individual's creditworthiness based on various financial factors such as credit history, debt-to-income ratio, payment history, and other relevant metrics. It generates a credit score, which is a numerical representation of the individual's credit risk, helping lenders make informed decisions about extending credit.

Q2. How does a customizable credit scoring engine differ from a standard credit scoring system?

While a standard credit scoring system typically follows a fixed set of rules and algorithms, Nected’s customizable credit scoring engine allows for greater flexibility and adaptability. Users can modify the scoring model by adding, removing, or adjusting variables such as credit history length, payment behavior, income levels, and other relevant factors. This customization empowers organizations to fine-tune their credit evaluation process to align with their specific business objectives and risk management strategies.

.webp)

.svg.webp)

.webp)

%20(1).webp)