.png)

.webp)

In the intricate world of banking, where precision and consistency are paramount, the use of rule engines has emerged as a critical technological underpinning. Rule engines, in essence, are software systems designed to automate decision-making processes by applying a set of predefined rules and logical conditions. These rules act as the guiding principles that enable banks to navigate the labyrinth of financial operations, ensuring compliance, efficiency, and reliability.

In the following exploration, we delve into the significance of rule engines within the banking industry. We unravel the various types of rule engines at play and illuminate their indispensable role in shaping how banks operate, make decisions, and deliver services. From safeguarding against fraud to streamlining customer interactions, rule engines have become the silent architects behind many facets of modern banking, driving accuracy and consistency in an ever-evolving financial landscape.

What is a Business Rule Engine in Banking?

The concept of a business rule engine in banking involves the application of a rule-based approach to decision-making within the automation process, considering customer, transaction, risk, and operational data. Banking organizations deploy rule engines to ensure that their policies are executed in an appropriate manner during their lending, compliance, fraud management, underwriting, collections, and client onboarding processes.

The rule engine helps banks separate the execution of policies from the process of creating such decisions, ensuring that the policies remain independent. It allows policies to be made, changed, and managed easily.

With changing regulations, markets, and customer demands, banking organizations have to ensure that the decisions they make are correct.

Why Banks Use Rule Engines

There are many banking processes that need daily decision-making, which include granting loans, checking the creditworthiness of customers, transaction monitoring, compliance, etc. Making such decisions manually, as well as hardcoding the logic into the application itself, may lead to inefficiency and operational risks.

The use of business rules engines makes decision logic management more effective because banks will be able to implement the decision logic once, but use it everywhere. This allows for improving the quality of decisions and responding to changing business needs.

Business Rules vs Hardcoded Banking Logic

Traditional banking systems often rely on hardcoded conditions embedded within applications. However, the use of these methods makes it hard to update policy rules since any changes need development, testing, and implementation processes to be done. The Business Rules Engine isolates the decision-making logic from the application logic.

The rule changes are done independently of the system by business personnel and can be quickly updated to suit the latest regulations and loan policies.

How a Business Rule Engine Works in Banking

The rule engine functions through the evaluation of banking data according to pre-set rules. It makes decisions based on such evaluations. The method ensures that banks can automate the enforcement of policies, minimize manual evaluations, and enforce consistency in the workflow.

For example, whether making an evaluation for a loan application or compliance, the rule engine is involved in a structured decision-making process.

Rule Definition and Management

The first step is defining the banking policies as flexible business rules. These rules can be, for example, lending rules, threshold values to determine fraudulent transactions, customer onboarding guidelines, or risk-related guidelines.

The business and risk managers use the central repository of rules where they can configure policies independently of the application code.

Rule Evaluation Process

Upon the occurrence of an event such as a transaction by a client, the rule engine will retrieve data and compare it against the existing rules.

For instance, a loan application can be evaluated based on the customer’s income, credit rating, debt-income ratio, employment record, and risk profile. The rule engine analyzes the input and finds out whether the requirements for loaning have been met.

Automated Decision Execution

After evaluating applicable rules, the engine executes predefined actions based on the outcome. Possible actions include:

- Approving or rejecting a loan

- Escalating applications for manual review

- Flagging suspicious transactions

- Triggering compliance checks

- Sending customer notifications

- Launching workflow processes

This automation reduces processing times while ensuring decisions remain aligned with organizational policies.

Credit Strategy Rule Engine Explained

A credit strategy rule engine is a specialized decision-management system that automates lending decisions using configurable credit policies and risk rules. It enables banks and financial institutions to evaluate borrowers consistently while ensuring compliance with underwriting standards and risk-management frameworks.

Rather than relying on manual reviews, credit strategy engines apply predefined lending logic to assess applications, determine risk levels, and generate appropriate lending decisions.

Credit Eligibility Rules

The eligibility criteria for credit decide if an individual is eligible for obtaining the financial service. Such criteria consider elements like age, income level, employment, credit history, liabilities, and geographical limitations, among others.

The automation of eligibility checks helps banks to spot potential applicants and save time on underwriting.

Credit Risk Assessment Rules

These are business logic used in assessing the probability of default on the loans. The engine evaluates the credit score, credit history, debt-to-income ratio, behaviors, and other risk factors to make an assessment of the risk classes. Such business rules help in keeping risk standards and also improve the portfolio quality.

Lending Terms and Offer Generation Rules

The pricing terms for loans are usually tailored to match the profile of the borrowing individual. A credit strategy rule engine will automatically generate the appropriate terms for interest rate, credit limit, loan repayment, and promotional offer using the existing business logic rules.

Credit Policy Management

There are often changes in credit policies depending on market forces, regulations, and risk management approaches. The credit strategy rule engine will ensure that all the changes in the policies are centralized, making them consistent throughout the lending process.

Business Rule Engine Use Cases in Banking

Business rule engines are used across multiple banking functions to automate decisions, enforce policies, and reduce operational complexity. Efficiency can be gained through the consistent application of rules, while compliance and faster customer interaction can be facilitated through rule engines. Rule engines help process important banking activities, such as lending, underwriting, fraud prevention, and collection processes.

Loan Origination

The loan origination process comprises various decision points such as qualifying decisions, validation of documents, risk assessments, and approvals. The business rule engine makes the decisions automatically based on lending criteria for each loan application.

After the submission of the loan application by the borrower, the rule engine will automatically assess the qualification criteria and decide upon further action accordingly.

Credit Underwriting

Underwriting entails the assessment of credit risk associated with potential borrowers on the basis of some key parameters. Underwriting is performed with the aid of rule engines that help assess the viability of loan applications.

Fraud Detection

Banks process huge volumes of transactions daily, which means that the timely identification of fraudulent activities is necessary.

The rule engine scans all the transactions for signs of fraudulent activities such as large transaction amounts, unusual geographical location, speedy spending, or anything out of the ordinary. Such predefined conditions trigger action.

KYC and Compliance Checks

Validation processes under Know Your Customer (KYC) and regulations are numerous. Rule engines undertake identity verification, sanctions screening, document validation, and regulatory evaluation.

This would help in making sure that all regulations are complied with without any manual effort or delay in the process of onboarding customers.

Collections and Recovery Workflows

Rule engines help the collections team in undertaking collections through automation. Dependent on the behavior of payment and risk factor, reminder letters or even collection may begin.

This approach is not only efficient in terms of saving time, but also consistent in treating all borrowers.

Business Rule Engine Architecture for Banking

In enterprise banking, rule engines must have an architecture that is capable of handling high transaction processing speeds in an efficient and reliable manner, while adhering to governance and regulatory standards. In today's world, a business rule engine architecture includes different components used for policy management and decision evaluation.

Rule Repository

The rule repository acts as the place where all rules, lending policies, regulatory requirements, and risk management strategies are stored. The purpose of this module is to allow banks to have control over rules from one source.

With the help of versioning and governance capability, any changes made to a policy can be easily traced and audited as required.

Decision Engine

The decision engine module helps to evaluate data according to the configured business rules and provide the resulting output. Customer data, transactions, risks, and other operational details are evaluated using the decision engine. This helps to make decisions related to the approval or rejection of requests.

Involvement in Core Banking Systems

A rule engine for banks needs to interact seamlessly with various applications like a loan origination system, a core banking system, CRM, fraud detection, and data warehousing systems.

Integration will ensure that the rules engine can use the necessary information and make decisions without having an information gap.

Audit Trail and Compliance Tracking

Regulatory bodies require banks to account for how their decisions are being made. Rule engines offer an audit trail of rule execution and decision-making, as well as policies.

This ensures compliance with the relevant regulations, as well as internal governance and regulatory audits.

Benefits of Using a Business Rule Engine in Banking

The business of banks operates within a heavily regulated space where accurate and consistent decision-making becomes critical. The use of a rule engine allows financial firms to make complicated decisions easily and consistently while also meeting regulations and minimizing costs.

Faster Loan Decisions

The manual review of loans can be quite costly in terms of both time and effort required. The use of a rule engine automates these processes, thus making it easier for banks to make such decisions quickly. This ensures that customers receive timely responses to their loan applications.

Enhanced Compliance with Regulations

Banks often have to follow changing regulations in their operations, which must be strictly adhered to. Rules engines facilitate compliance through automated enforcement of the regulatory policies.

Regulation changes can lead to updates to rules, which can instantly be incorporated into different business processes within the bank.

Uniform Credit Decisions

There could be different interpretations by various departments and channels in the case of manual evaluation of lending policies. With rule engines, this problem can be solved through consistent implementation of the decision criteria.

Lowered Operating Expenses

With automation, there is reduced need for manual review, repetition of activities, and decision-making.

Credit Strategy Rule Engine vs Traditional Lending Systems

Conventional systems for lending involve a lot of manual processing, rigid processes, and fixed decision-making. Credit strategy rule engines provide automation, flexibility, and scalability to the decision-making process, and thus help banks understand the merits of such technology.

Decision Speed

Lending processes in conventional systems take quite some time to make decisions due to numerous manual reviews and approvals.

Rule-based lending systems enable fast processing of lending decisions, usually taking just seconds.

Flexibility

Policy updates within conventional lending models usually demand deployment efforts and development time. This results in delays in making changes and executing them.

A rule engine moves decision logic outside the application code, thereby allowing the business to alter lending policies and criteria without making any modifications within the application code itself.

Risk Management

Hard-coded and manual lending systems often lead to inconsistencies in lending policies. Rule engines apply risk policies consistently in all the applications.

The centralization of rule management further ensures consistent implementation of risk management policies across channels and products.

Types of Rule Engines in Banking

In the intricate realm of banking, where a multitude of operations and decisions are made every minute, different types of rule engines find their specific applications. These rule engines, designed to cater to various aspects of banking, contribute significantly to the sector's efficiency and compliance. Here, we delve into some of the key types of rule engines commonly used in the banking industry:

- Credit Scoring Engines: In the banking industry, one of the most prevalent uses of rule engines is in credit scoring. These engines assess the creditworthiness of individuals and businesses by analyzing various factors such as credit history, income, debt, and more. Rule-based credit scoring engines help banks make informed lending decisions, whether it's approving a loan, setting interest rates, or determining credit limits. They ensure consistency and objectivity in evaluating credit applications.

- Anti-Money Laundering (AML) Rule Engines: AML rule engines are vital tools for banks to combat financial crimes, including money laundering and terrorist financing. These engines employ predefined rules and algorithms to analyze transactions and customer data. When suspicious activities or patterns are detected, alerts are generated for further investigation. AML rule engines are crucial for regulatory compliance and safeguarding the integrity of the financial system.

- Fraud Detection Engines: Banking institutions face constant threats from fraudsters seeking to exploit vulnerabilities. Fraud detection rule engines play a pivotal role in identifying potentially fraudulent activities. They monitor transactions in real-time, applying rules to detect unusual patterns or behaviors. When a transaction triggers a predefined rule, it may be flagged for review or declined, preventing unauthorized access to funds and protecting customers.

- Customer Interaction Engines: Rule engines also enhance customer interactions in banking. These engines use predefined rules to personalize customer experiences. For example, when a customer logs into their online banking portal, the rule engine can display customized content based on their previous interactions and preferences. This personalization fosters stronger customer relationships and promotes cross-selling opportunities.

- Compliance Rule Engines: Regulatory compliance is a top priority for banks. Compliance rule engines ensure that banking operations adhere to industry regulations and government mandates. These engines continuously monitor transactions, policies, and procedures, flagging any deviations from compliance standards. This helps banks avoid penalties, legal issues, and reputational damage.

- Accounting Rule Engines: Accounting rules engines play a crucial role in ensuring accurate financial reporting and compliance with accounting standards. They automate accounting processes, manage journal entries, and facilitate financial statement preparation. These engines help banks maintain financial transparency and integrity.

- Loan Origination Rule Engines: When customers apply for loans, whether for mortgages, personal loans, or business loans, loan origination rule engines streamline the application and approval process. They evaluate applicant data against predefined lending criteria, automating the decision-making process. Loan origination rule engines enhance the speed and accuracy of loan approvals while maintaining consistency in lending practices.

- Risk Management Engines: Managing risk is fundamental in banking. Risk management rule engines assess various types of risk, such as credit risk, market risk, and operational risk. By applying predefined risk models and rules, these engines help banks make informed decisions about investments, asset allocation, and lending strategies.

Each of these rule engines serves a distinct purpose within the banking industry, aligning with specific needs and challenges. The ability to automate decision-making based on predefined rules not only enhances operational efficiency but also ensures banks remain compliant, secure, and customer-focused. These rule engines collectively contribute to the robustness of the banking ecosystem, facilitating prudent financial practices and dependable customer service.

Read Also: Java Rule Engines: Automate and Enforce with Java

How to Use Rule Engines in Banking: An Example

To better understand the practical application of Business rule engines in the banking industry, let's delve into a real-world example of how a rule engine can be employed to streamline operations and enhance customer experiences.

Scenario: Loan Approval and Underwriting Process

In the dynamic landscape of the banking industry, where customers often seek financial assistance for various purposes, one critical aspect is the efficient processing of loan applications. Whether it's a personal loan, mortgage, or business loan, banks face the challenge of evaluating numerous applications while maintaining rigorous standards for risk assessment and regulatory compliance.

To meet these demands, banks employ sophisticated technological solutions that streamline the loan approval and underwriting process. A pivotal component of this modernization is the integration of rule engines. These rule engines are software systems that use predefined rules and decision logic to automate the evaluation of loan applications.

The scenario revolves around the intricate process of loan approval and underwriting within a banking institution. This multifaceted process is fundamental to a bank's operations, ensuring responsible lending practices while mitigating financial risks. Below, we provide an overview of the steps involved in this crucial process, highlighting how rule engines enhance efficiency and decision-making.

Step 1: Customer Application Submission The loan approval and underwriting process commences when a customer expresses the need for financial assistance, such as a personal loan, mortgage, or business loan. Customers can conveniently submit their loan applications through the bank's digital channels, including its website or mobile app.

Step 2: Data Collection

Once the loan application is submitted, the bank initiates a comprehensive data collection process. This step involves gathering a wide range of information from the applicant. This data may include:

Personal Details: Name, address, contact information, social security number, etc.

Financial History: Credit history, previous loans, repayment behavior.

Employment Records: Current and past employment details.

Income Statements: Documentation of income sources, such as pay stubs, tax returns, or business financials.

Purpose of the Loan: Specifics on how the loan will be used, such as buying a home or expanding a business.

Step 3: Data Verification

The collected data undergoes rigorous verification processes. Bank personnel verify the authenticity of submitted documents, confirm the applicant's identity, and cross-reference the information with existing records.

Step 4: Credit Score Assessment

A crucial aspect of the underwriting process is evaluating the applicant's creditworthiness. This assessment often relies on the applicant's credit score, which provides insights into their historical credit behavior and repayment reliability.

Step 5: Income and Financial Analysis

The applicant's income and overall financial health are scrutinized to determine their capacity to repay the loan. This analysis involves:

Reviewing income sources and stability.

Assessing debt obligations and existing financial liabilities.

Examining financial assets and reserves.

Step 6: Collateral Assessment (if applicable)

For secured loans like mortgages, the bank assesses the value and condition of the collateral offered by the applicant. This collateral serves as security for the loan and mitigates the bank's risk.

Step 7: Regulatory Compliance

Banks must ensure strict compliance with financial regulations and lending laws. This step involves navigating a complex web of regulations at the federal, state, and local levels. Compliance ensures that the bank's lending practices align with legal requirements.

Step 8: Risk Evaluation

A critical function of underwriting is evaluating the risk associated with the loan. This involves:

Assessing the applicant's credit risk based on credit score and history.

Analyzing market conditions that may affect the loan's performance.

Evaluating the purpose of the loan and its alignment with the bank's lending criteria.

Step 9: Decision Making

After the completion of these comprehensive evaluations, a decision must be made regarding the loan application. Decisions can fall into several categories, including:

Approval: The loan is approved, and the applicant proceeds with the next steps.

Rejection: The application is declined based on risk assessment or other factors.

Further Review: In some cases, additional information or clarification may be required before a decision can be made.

Step 10: Customer Notification

Prompt communication with the customer is essential. Regardless of the decision, the applicant must be notified transparently and professionally, explaining the outcome and any necessary next steps.

Step 11: Documentation and Disbursement

For approved loans, the bank generates the required loan documentation. This documentation outlines the terms and conditions of the loan, including interest rates, repayment schedules, and any collateral details. After the applicant signs the agreement, funds are disbursed according to the loan's purpose.

Step 12: Post-Approval Monitoring

The relationship between the bank and the borrower doesn't end with approval. The bank continues to monitor the loan portfolio, ensuring that borrowers are meeting their repayment obligations. Early signs of delinquency are addressed through collections processes.

In this comprehensive loan approval and underwriting process, banks rely on rule engines to automate decision-making, improve efficiency, and ensure consistency in assessing loan applications. Rule engines play a crucial role in risk management and regulatory compliance, allowing banks to offer loans with confidence while safeguarding their financial interests.

Here's a diagrammatic representation of the steps for the "Loan Approval and Underwriting Process in Banking" scenario:

The diagram illustrates the "Loan Approval and Underwriting Process in Banking," providing a visual representation of the steps and decision points involved in this critical banking procedure. The process begins with a customer application submission, where data collection is initiated. Subsequently, the data undergoes verification, followed by a credit score assessment and an analysis of the applicant's income and financial situation. Concurrently, collateral assessment is conducted to evaluate assets provided as security.

Read Also: Rule Engine: A Comprehensive Guide to Business Rule Engine

Challenges and Considerations

Here's a table highlighting the challenges and considerations associated with the use of rule engines in the banking sector:

These challenges and considerations highlight the importance of careful planning, robust security measures, and ongoing monitoring in the implementation and usage of rule engines in the banking industry.

How Nected Supports Banking Rule Engines?

Banks are not only looking for decision automation. They need an entire platform for rule management, automation, and integration across multiple business departments. With Nected, users are able to develop and manage their banking decisions based on rules and automated workflows.

No-Code Credit Policy Management

With Nected, users are able to define, manage and customize their credit policies. Users can set up lending conditions, risk limits and regulations without much technical help.

Real-Time Decision Making

Many decisions in banking demand an immediate answer. Nected makes all decisions in real-time based on the available information provided by the customer or transaction.

It will help your organization become more responsive, making all decisions consistently and promptly.

Workflow-Based Banking Process Automation

Combining workflows with business rules helps automate banking processes from the beginning to the end, such as client onboarding, loan origination and underwriting, collections and many others.

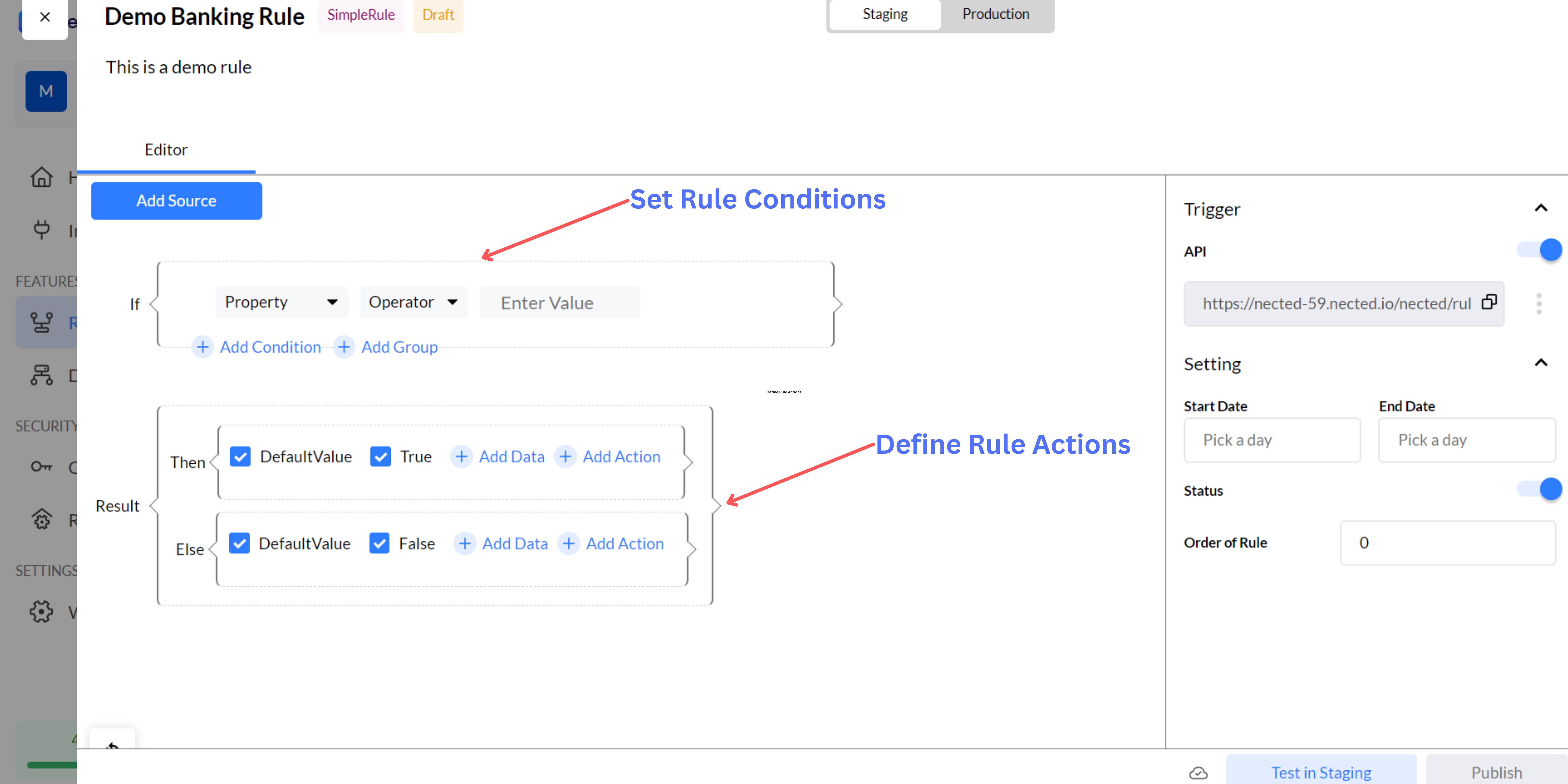

How to Build Rules for the Banking Sector with Nected?

Building and managing rules in the banking sector is critical to ensure compliance, streamline operations, and enhance decision-making processes. Nected, a powerful rule engine, offers an efficient way to create, deploy, and manage these rules. In this section, we'll walk you through the process of building rules for the banking sector using Nected, step by step.

Step 1: Accessing Nected

Login to Nected: Begin by logging into the Nected platform using your credentials. If you don't have an account, you can sign up for one.

Step 2: Create a New Rule

- Start a New Rule Project: Once you're logged in, you can start a new rule project. Click on "New Project" and select "Rule Project" from the options.

- Define Rule Properties: Give your rule project a name and provide a brief description. These properties will help you identify and manage your rule project effectively.

Step 3: Rule Creation

- Design Rule Structure: In Nected, rules are organized into a structured format. Define the structure of your rule by adding conditions, actions, and exceptions. Use the intuitive drag-and-drop interface to create and arrange rule components.

- Set Rule Conditions: Specify the conditions under which the rule will be applied. For example, you might define conditions based on customer account balances, transaction types, or risk levels.

- Define Rule Actions: Determine the actions to be taken when the rule conditions are met. Actions can include approving or denying transactions, sending alerts, or triggering further processes.

Step 4: Testing and Validation

- Testing Rules: Before deploying your rules in a live banking environment, it's crucial to thoroughly test them. Nected provides testing tools to simulate rule execution and verify that the outcomes align with your expectations.

- Validation: Ensure that the rules are validated against different scenarios and edge cases. Make adjustments as needed to fine-tune rule behavior.

Step 5: Deploying Rules

- Deployment: Once your rules are thoroughly tested and validated, you can deploy them into your banking system. Nected offers seamless integration options with various banking software and platforms.

Step 6: Monitoring and Optimization

- Monitoring Rules: After deployment, continuous monitoring of rule performance is essential. Nected provides real-time analytics and reporting tools to track rule execution and outcomes.

- Optimization: Based on monitoring data and changing banking regulations, you can optimize your rules. Nected allows you to make rule adjustments without disrupting operations.

Step 7: Compliance and Reporting

- Compliance: Ensure that your rules remain compliant with banking regulations. Nected assists in generating compliance reports and documentation.

- Reporting: Use Nected's reporting features to gain insights into rule performance, identify patterns, and make data-driven decisions to improve banking operations.

With Nected's user-friendly interface and comprehensive rule management capabilities, building and managing rules for the banking sector becomes efficient and agile. Whether it's fraud detection, loan approval, or customer onboarding, Nected empowers banking institutions to make faster and more accurate decisions while maintaining compliance.

By following these steps and leveraging Nected's capabilities, your bank can create, deploy, and manage rules effectively, ensuring smooth operations and compliance in the ever-evolving banking industry.

Interlinking Rule Engines in Banking

In the banking industry, the use of rule engines often extends beyond individual applications. Many banks leverage multiple rule engines or integrate them into a broader ecosystem of software and services. Interlinking rule engines in banking is a strategic approach that enables seamless data flow, decision consistency, and enhanced operational efficiency. Here, we explore how rule engines are interconnected in the banking sector:

1. Data Integration and Exchange: Rule engines often work with vast datasets scattered across various systems within a bank. Interlinking rule engines facilitates data integration, allowing these systems to share information efficiently. For example, customer data stored in the bank's core system can be seamlessly accessed and analyzed by credit scoring rule engines, ensuring consistent decision-making.

2. Workflow Automation: Rule engines are integrated into workflow automation systems, ensuring that rule-based decisions are executed as part of end-to-end processes. For instance, loan origination workflows can use rule engines to determine eligibility, calculate interest rates, and automate approvals, streamlining the entire loan application process.

3. Decision Consistency: Banks use multiple rule engines for different purposes, such as fraud detection, risk assessment, and compliance checks. Interlinking these rule engines ensures that decisions made across various functions are consistent and aligned with the bank's overarching objectives.

4. Real-time Processing: In scenarios where real-time decision-making is crucial, interlinked rule engines enable instant access to relevant data and rules. For example, during card transactions, rule engines can quickly assess whether a transaction should be approved or flagged as potentially fraudulent based on predefined rules.

5. Regulatory Compliance: Banks must adhere to a myriad of regulations and standards. Interlinked rule engines help ensure that compliance rules are consistently applied across all banking operations, reducing the risk of non-compliance and associated penalties.

6. Reporting and Analytics: Rule engines generate valuable data that can be leveraged for reporting and analytics. By interlinking these engines, banks can centralize data storage and reporting, gaining insights into the performance of rule-based systems and identifying areas for improvement.

7. Customer Experience: Banks aim to provide a seamless and personalized customer experience. Interlinked rule engines support this goal by enabling the customization of services and offerings based on customer profiles and preferences.

8. Scalability: As banking operations grow, scalability becomes essential. An interconnected rule engine architecture can be scaled horizontally or vertically to accommodate increased workloads and maintain high performance.

9. Risk Management: Interlinking rule engines enhance risk management by allowing banks to consolidate risk assessment data from various sources. This comprehensive view enables more informed decisions regarding risk exposure and mitigation strategies.

In summary, interlinking rule engines in banking fosters operational efficiency, data consistency, and enhanced decision-making across various functions. It enables banks to adapt to evolving regulatory requirements, improve customer experiences, and effectively manage risks. The strategic integration of rule engines is a valuable asset in modern banking operations, contributing to competitiveness and compliance.

Read Also: Spring Boot Rule Engine: Powering Business Logic with Ease

Conclusion

In the dynamic and highly regulated world of banking, rule engines have emerged as indispensable tools for automating processes, ensuring compliance, and delivering exceptional customer experiences. This blog has explored the diverse applications of rule engines in the banking sector, ranging from fraud detection and risk assessment to loan approvals and compliance checks.

We've delved into various types of rule engines, such as open-source and proprietary solutions, each offering unique features and benefits. Moreover, we've examined real-world use cases, including loan approval and underwriting processes, to illustrate how rule engines drive efficiency and consistency in decision-making.

From an Indian perspective, rule engines play a pivotal role in addressing the specific needs of the banking industry in India, aligning with regulatory frameworks and streamlining operations.

However, it's essential to acknowledge the challenges and considerations that come with implementing rule engines, including data privacy, integration complexities, and the need for skilled personnel.

As the banking sector continues to evolve, the role of rule engines will only become more prominent, supporting banks in their quest for operational excellence and customer satisfaction.

FAQs:

Q1. What do you mean by Banking rule engine?

A banking rule engine is a specialized software system designed to automate decision-making processes within the banking industry. It employs predefined rules and logic to evaluate data and make consistent, efficient, and compliant decisions across various banking operations, including risk assessment, fraud detection, loan approvals, and regulatory compliance.

Q2. What are the features of Banking rule engine?

Key features of a banking rule engine typically include:

- Rule Authoring: The ability to define and manage rules efficiently, often using a user-friendly interface.

- Scalability: The capacity to handle large volumes of data and transactions in real-time.

- Integration: Seamless integration with existing banking systems and databases.

- Decision Traceability: The capability to track and audit decisions made by the rule engine for compliance purposes.

- Flexibility: The ability to adapt to changing regulatory requirements and business needs.

- Real-time Processing: Rapid evaluation of rules and instant decision-making.

- Rule Versioning: The ability to manage different versions of rules for historical reference.

- Rule Testing: Tools for validating and testing rules before deployment.

- Reporting and Analytics: The generation of reports and insights into rule performance.

- Security: Robust security features to protect sensitive banking data.

Q3. Why do we use Banking rule engine?

Banking rule engines are used for several critical reasons:

- Efficiency: Rule engines automate routine decision-making processes, reducing manual effort and operational costs.

- Consistency: They ensure that decisions are made consistently, adhering to predefined rules and regulatory requirements.

- Compliance: Rule engines help banks comply with complex and ever-changing regulatory frameworks.

- Risk Mitigation: They assist in identifying and mitigating risks related to fraud, credit, and compliance.

- Enhanced Customer Experience: By expediting processes like loan approvals, they contribute to improved customer satisfaction.

- Data-Driven Decision-Making: Rule engines analyze vast amounts of data to make informed decisions quickly.

- Competitive Advantage: Banks that implement rule engines can offer faster and more accurate services, gaining a competitive edge.

Q4. What is a rule engine in banking?

A rule engine in banking is a software component that automates decision-making processes within a bank's operations. It operates based on predefined rules and logic, evaluating data to make consistent and efficient decisions across various banking functions. Rule engines in banking are crucial for ensuring regulatory compliance, enhancing operational efficiency, and improving customer service.

.svg.webp)

.webp)

.jpg)

%20(1).webp)