.png)

.webp)

Credit scoring still drives a lot of loan, mortgage, and card decisions. Most systems lean on payment history, debt-to-income ratio, and credit utilization. Behavioral credit scoring pushes that a bit further. It looks at how people actually act, not just what shows up in a credit file.

That means spending patterns, payment timing, transaction habits, and a few other signals that lenders have started paying attention to. It is not magic. But it does give a fuller picture when the usual data is thin or messy.

If you are trying to understand how the model works, where it helps, and where it can go wrong, this breaks it down without the fluff. You will also see a behaviour score breakdown and a few examples that show how these models are used in practice.

What is behavioral credit scoring?

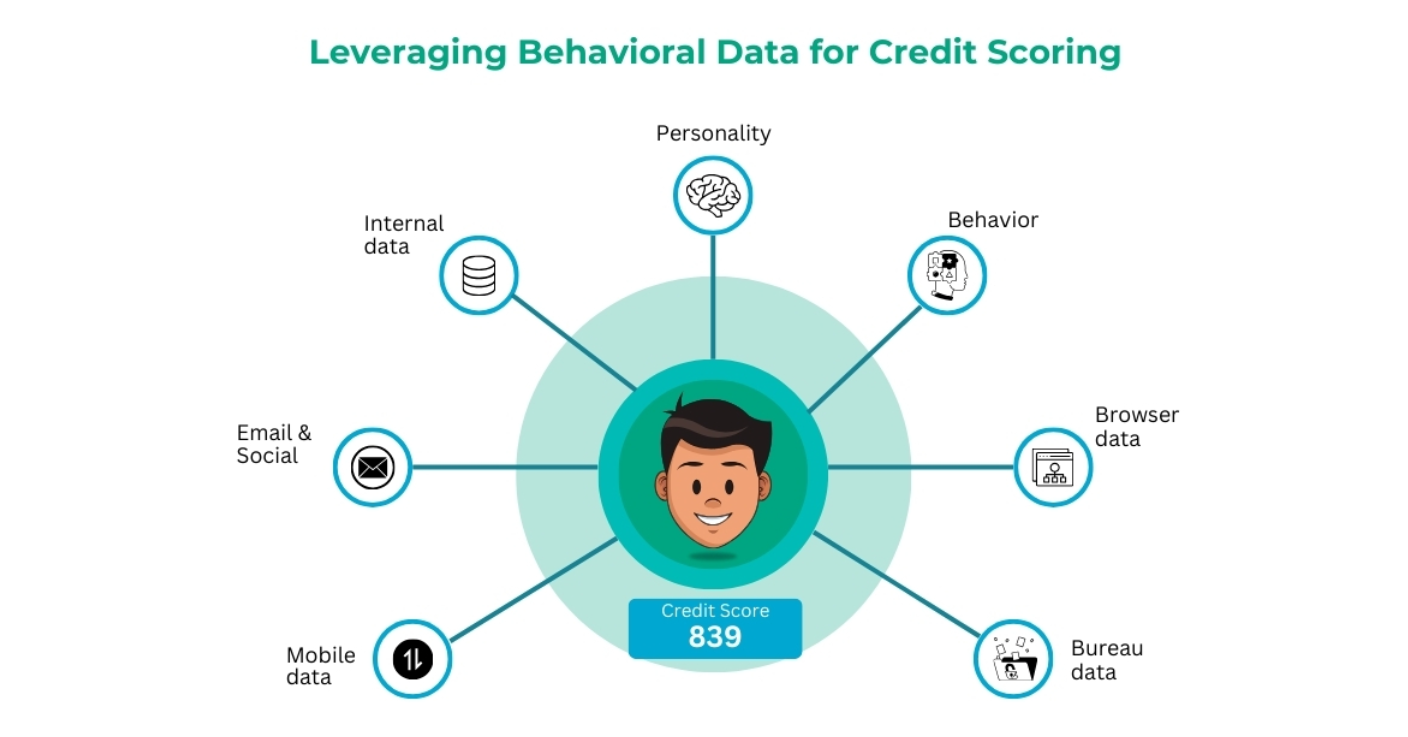

Behavioral credit scoring is a way to assess creditworthiness using everyday behavior along with standard financial data. It does not replace traditional credit scoring. It adds another layer on top of it.

Instead of looking only at old repayment records or balances, it checks things like spending habits, transaction frequency, purchase types, and other usage signals. In some setups, that can also include online activity or biometric data, though that part often gets ignored until compliance shows up.

For lenders, the point is simple. They want a better read on risk before they approve credit or set terms. That is where these models start to matter.

Real-world examples of behavioral credit scoring

- Automotive financing: Credit scores are used to decide whether someone qualifies for an auto loan and what kind of rate they get.

- Telecommunications: Mobile service providers and utilities use scoring to decide who gets postpaid plans and who does not.

- Online retailers: eCommerce platforms use behavioral signals for financing offers and buy-now-pay-later programs.

- Rental housing: Landlords use it to screen applicants and cut down on payment risk.

Effects of Credit Behavior on Credit Scores

Credit behavior effects show up fast in scoring models. Some of them are obvious. Some are not.

Repayment history still carries the most weight in many systems. Credit utilization comes next in a lot of cases. Payment delays hurt quickly, sometimes more than people expect. Transaction patterns also matter because they show consistency, or the lack of it. Account age helps too. A longer history gives the credit scoring model more to work with.

This directly supports credit behavior effects. It is the difference between a score that only reacts to missed payments and one that picks up smaller changes earlier.

What Is a Behavioral Scoring Model

A behavioral scoring model is the part that turns raw customer data into a risk score. It can be rule-based, machine learning based, or a mix of both. In practice, lenders usually start simple and add more logic once they trust the inputs.

The data usually comes from account activity, repayment patterns, purchase behavior, and related signals. Then the model scores the behavior against whatever risk rules the lender has set. Some teams run it in batch. Others want real-time risk evaluation because that is where things usually break if the signal is delayed.

The flow is pretty direct:

Customer Data

↓

Behavior Analysis

↓

Scoring Model

↓

Risk Score

That is the basic shape. The hard part is deciding which signals are actually useful and which ones just add noise.

What business and customer-centric problems does behavioral credit scoring solve?

The tables below show the kinds of problems it solves on both sides. In lending, those two views usually overlap more than people like to admit.

Business-End Problems

This table will provide an overview of the business-end problems.

Customer-Centric Issues

This table will provide an overview of the customer-centric issues.

By addressing these problems, behavioral credit scoring gives lenders a more usable view of risk and gives customers a fairer shot when traditional data is limited.

What are the key factors considered in behavioral credit scoring models?

Behavioral credit scoring models look at more than just the usual financial history. The main signals are:

- Spending patterns: how often people buy, what they buy, and whether the pattern stays stable over time.

- Transaction history: timing, frequency, and size of transactions.

- Payment behavior: how often bills, loans, and card balances are paid on time.

- Credit utilization: how much of the available limit is being used.

- Online activity: browsing and platform interactions, when those signals are part of the model.

- Social interactions: social connections and activity, though this part is handled carefully because it can get messy fast.

- Biometric data: fingerprints, facial recognition, or voice checks for identity and fraud prevention.

- Location data: travel and spending patterns tied to geography.

- Interaction with financial products: applications, inquiries, and use of financial tools.

What are the challenges and limitations of behavioral credit scoring?

While behavioral credit scoring can help, it also brings a few headaches.

Implementing behavioral credit scoring is not hard because of the code. It is hard because of the data, the rules, and the edge cases.

What Is a Behavioral Scoring Model

You can set up behavioral scoring in Nected without building everything from scratch. That is useful if you do not want to wire a full internal system just to test one credit scoring model.

Nected uses a low-code, no-code rule engine that connects with data sources and lets teams define scoring rules around specific attributes. You can shape the model around credit history, credit utilization ratio, payment history, credit mix, length of history, income level, and similar inputs.

Here is the basic setup.

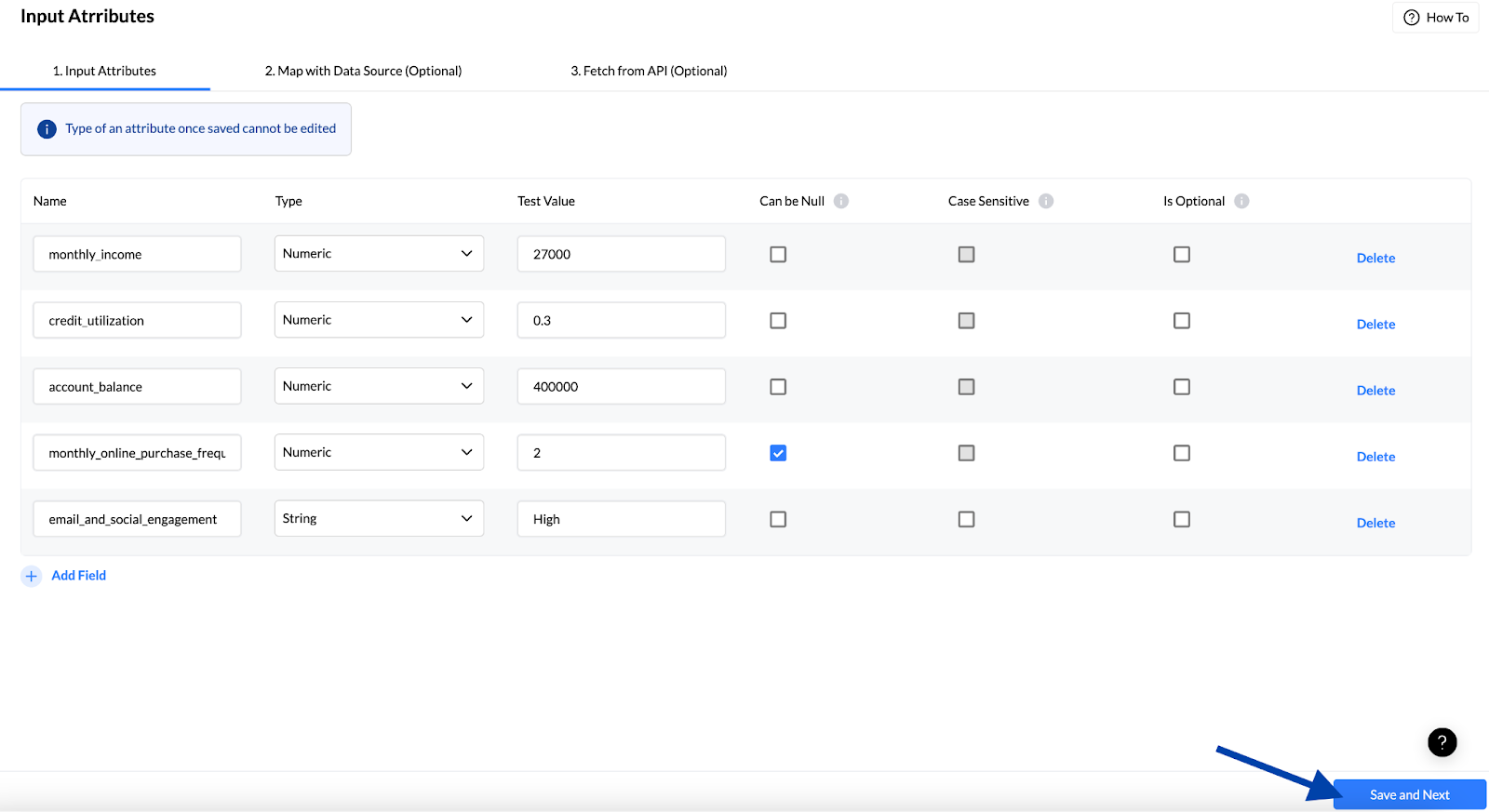

Step 1: Assigning Attributes

After logging in, go to the attributes section and pick the fields you want to use.

In this example, the model uses:

- Monthly Income

- Credit Utilization

- Account Balance

- Monthly Online Purchase Frequency

- Email & Social Engagement

These inputs help shape the score because they show how someone behaves over time, not just what their past credit file says.

In this step, add the attributes you want to use for the rule.

- Set the name, type, and test value.

- You can also mark fields as can be null, case sensitive, or optional.

- After that, click Save and Next.

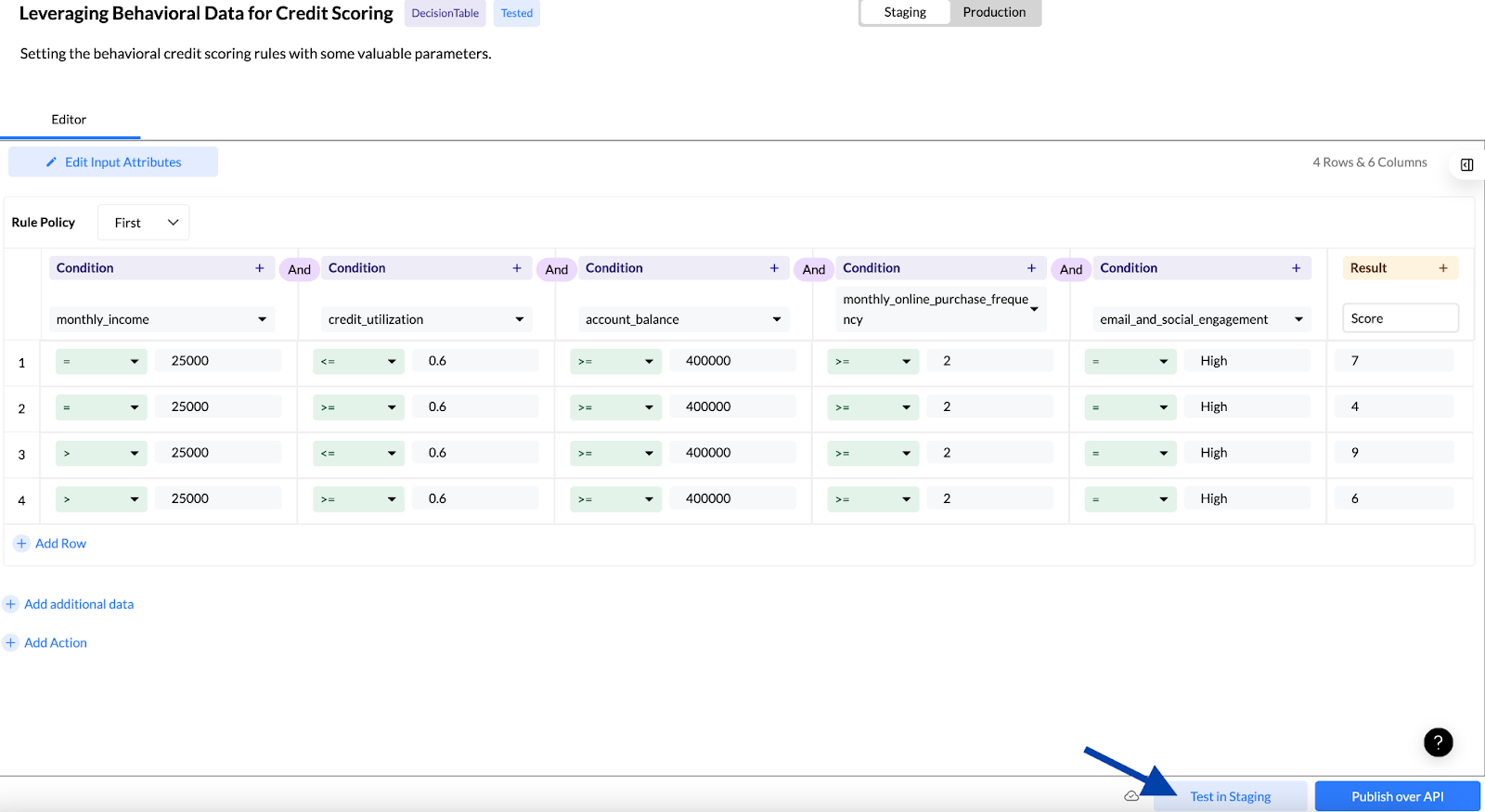

Step 2: Setting the conditional logic

This is the part that matters most. You define the logic, connect the attributes with AND and OR rules, and assign the output to a final score.

Once that is set, click “Test in Staging” and move on.

Step 3: Testing and confirmation

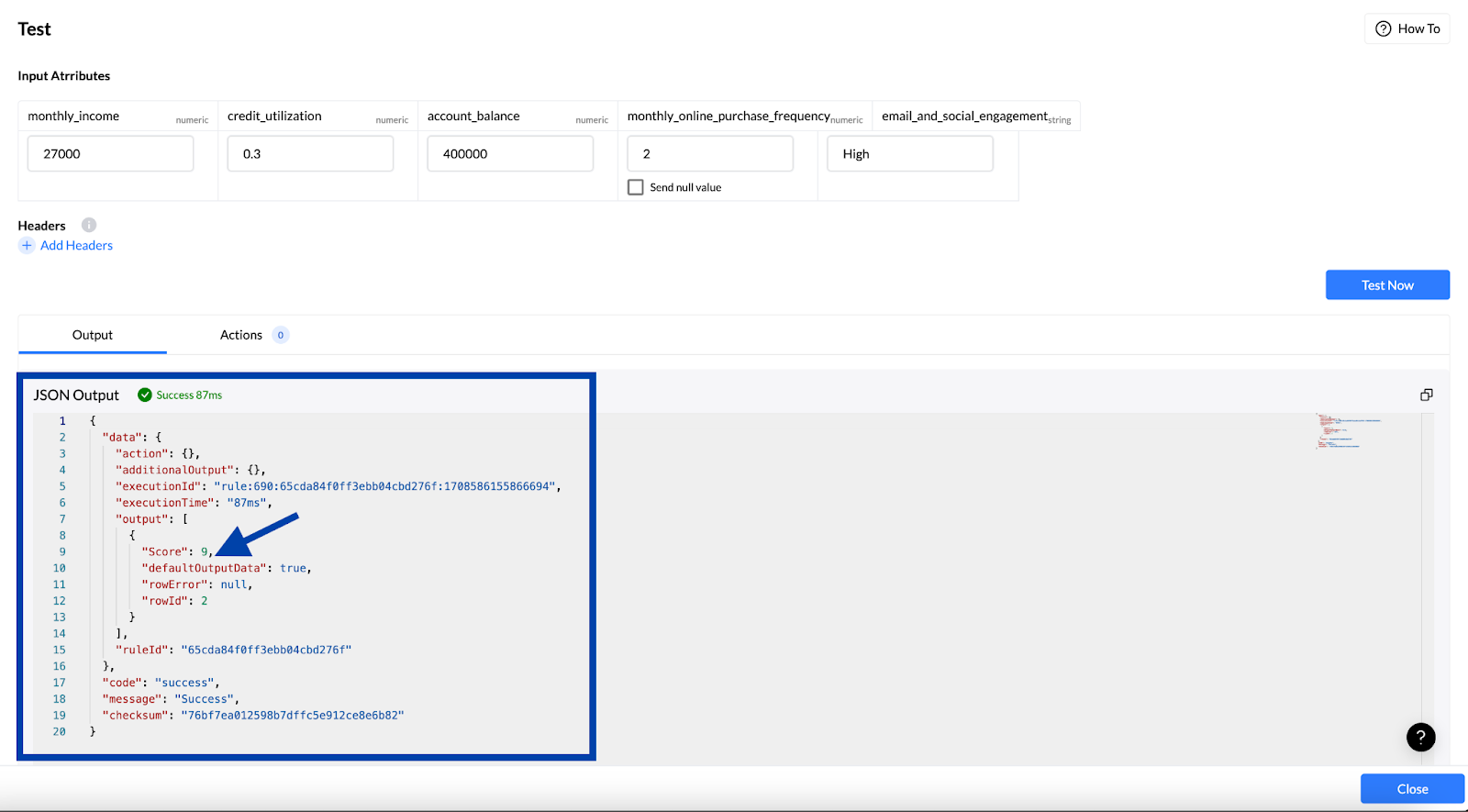

In the input attributes section, add the values you want to test and check the score. For this example, the data is:

- Monthly Income = 27000

- Credit Utilization = 0.3

- Account Balance = 400000

- Monthly Online Purchase Frequency = 2

- Email & Social Engagement = High

After that, click Test Now and wait for the result. If you see “Rule Tested Successfully” and the score in the JSON output, the setup worked.

You can also reuse those attributes, test different values, and adjust the scoring logic as needed.

For a deeper walkthrough, read this article: Mastering Credit Scoring with Nected.

Applications of Behavioral Credit Scoring

Behavioral credit scoring shows up in a few places where traditional checks are too slow or too thin. Personal lending is one. BNPL platforms use it too. So do fintech credit risk models, credit card approvals, and SME lending.

In smaller-ticket lending, speed matters. A lender does not always have time to wait for a full manual review. This is where a credit scoring model built on behavior can help.

- Personal lending: used to screen borrowers quickly when standard credit history is limited.

- BNPL platforms: helps decide whether a customer gets instant checkout credit.

- Fintech credit risk models: gives product teams a cleaner way to score users in real time.

- Credit card approvals: supports faster underwriting and better limit assignment.

- SME lending: useful when business cash flow is irregular and the usual scorecard misses context.

Conclusion

Behavioral credit scoring is one of those ideas that sounds simple until you try to use it at scale. The data needs to be clean. The rules need to hold up. And the model has to make sense when real customers start moving through it.

Still, it gives lenders a better way to evaluate risk, especially when traditional files do not tell the full story. It also helps with credit behavior effects, which are often the first signs that a borrower’s profile is changing.

If you are building this kind of system, a behavioral scoring model is usually easier to manage when the logic is centralized instead of scattered across code. That is where a tool like Nected fits in.

This looks simple. It usually isn’t.

FAQs

What is behavioral credit scoring?

It is a method of scoring creditworthiness using behavioral data along with standard financial data. The goal is to get a better read on risk than a traditional credit scoring model can offer on its own.

What is a behavioral scoring model?

A behavioral scoring model is the logic that takes customer behavior, applies rules or machine learning, and turns that into a risk score.

How does credit behavior affect credit scores?

Things like repayment history, payment delays, utilization, transaction patterns, and account age can raise or lower the score. Good habits usually help. Bad ones usually do not.

What factors influence behavioral credit scores?

Common factors include spending patterns, repayment behavior, credit utilization, transaction timing, account age, and in some cases online or biometric signals.

.svg.webp)

.webp)

.jpg)

%20Medium.jpeg)

%20(1).webp)