.png)

.webp)

In commercial business, credit score plays a major role. It helps the business to make trustworthy transactions and enables the business to grow. Just as an individual has a credit score to determine creditworthiness, commercial businesses also undergo similar evaluation by the commercial credit scoring model. These models help the business lenders and creditors to identify the risk involved in extending credit to the business. In this blog, we will understand commercial credit scoring models and how they can influence your business.

Understanding Commercial Credit Scoring Models

Now, let us understand what is a commercial credit score model with definitions, examples, and other important things to consider.

What is the Commercial Credit Scoring Model?

A commercial credit scoring model is used to validate the creditworthiness of businesses. Similar to how individuals have credit scores that reflect their ability to manage debt and make payments on time, businesses are also evaluated based on their financial history to determine the risk associated with the commercial business.

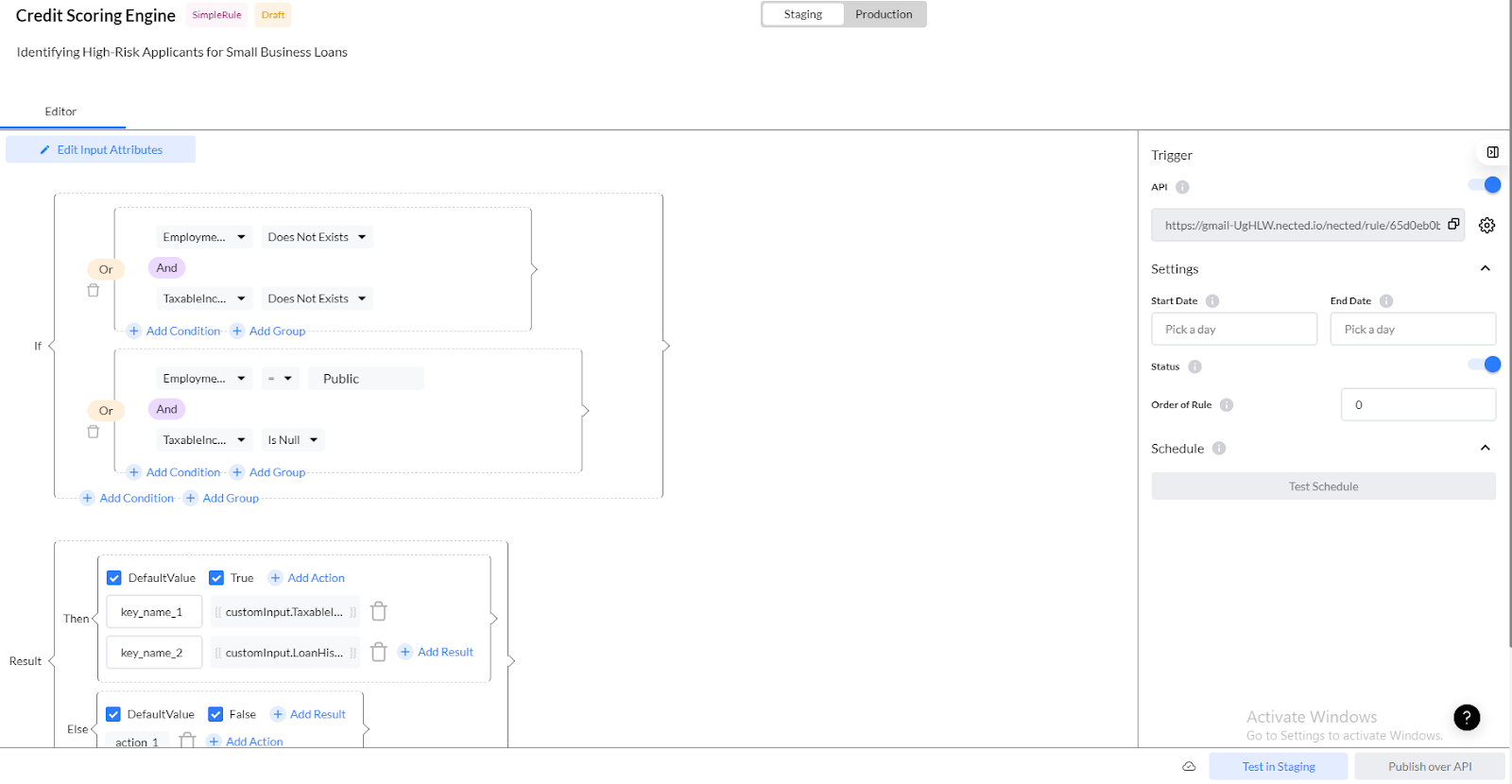

Commercial credit scoring engines using Nected help lenders and financial institutions analyze various aspects of a business's financial health, payment history, level of debt, length of credit history, industry risk, and other relevant factors. Considering these factors the scoring model generates a commercial credit score that shows the level of risk associated with lending to that business.

These commercial credit scores help lenders make informed decisions about whether to extend credit to a business and the probability of repayment.

Examples of Commercial Credit Scoring Model

Although the commercial credit scoring model may vary from business to business, it generally evaluates similar aspects of the business's financial health. Now let's see some credit scoring models examples

FICO Small Business Scoring Service: This model is designed by Fair Isaac Corporation. These business credit scoring models evaluated the creditworthiness of a business by analyzing historical transaction data.

Dun & Bradstreet PAYDEX: This model by Dun & Bradstreet provides the commercial credit score d&b based on the business's payment history with suppliers and vendors. These models utilize various methods and data sources to generate a commercial credit score for a business.

Experian's Intelliscore Plus: Intelliscore Plus evaluates a business's credit risk using predictive analytics, incorporating factors like credit utilization, payment history, and public records.

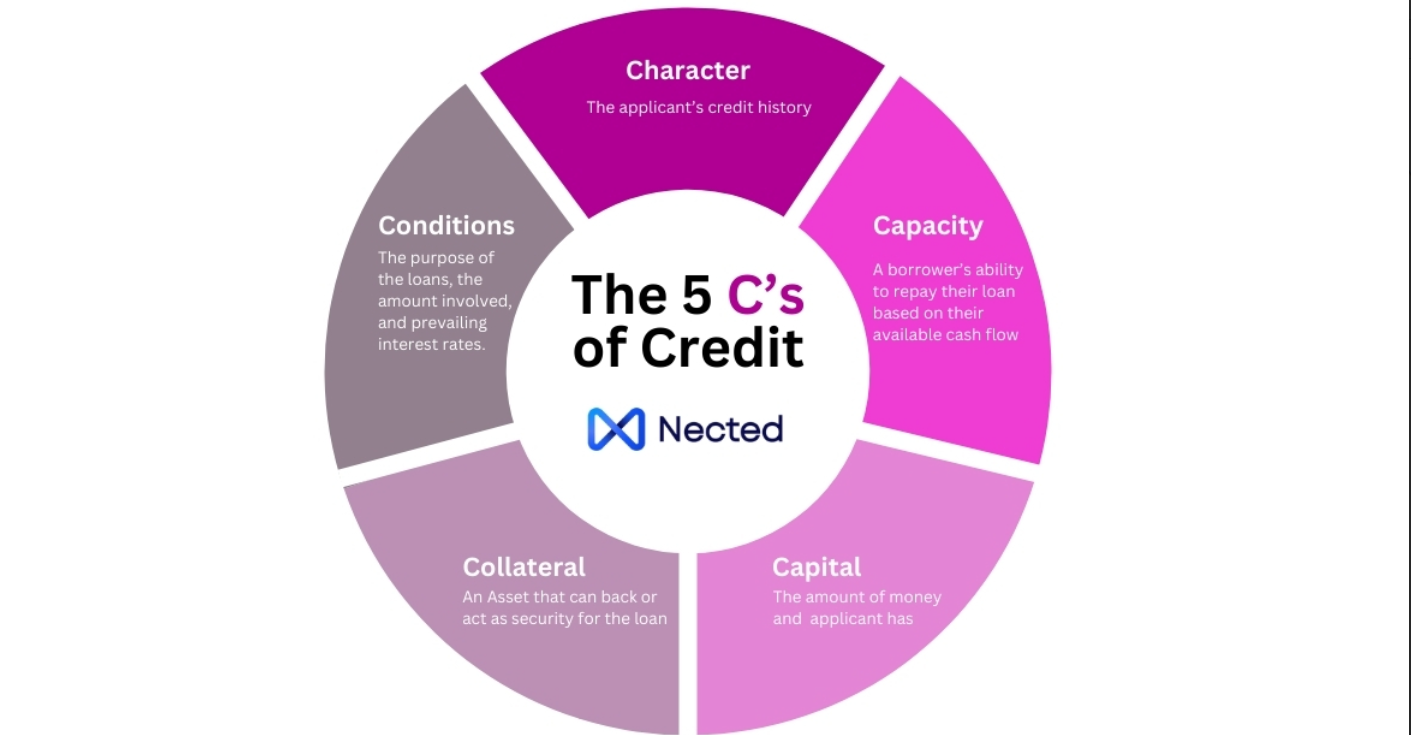

5Cs of the Commercial Credit Scoring Model

The 5Cs of a credit score are crucial to consider when you build a customized credit scoring rules engine for your company with Nected.

When you create a rule in your credit scoring rules engine keep in mind the 5Cs of Credit. Knowing and improving these parameters will improve your eligibility.

1. Capacity

2. Collateral

3. Capital

4. Conditions

5. Character

Capacity: Capacity assesses the business's ability to repay the loan by considering factors such as revenue, expenses, cash flow, and repayment timing detailed in the business plan. Lenders also examine personal and business credit reports along with credit scores from major credit reporting agencies like Equifax, Experian, and TransUnion. A lower debt-to-income ratio (DTI) indicates better liquidity and a higher probability of timely payment.s.

Capital: Capital demonstrates the business's financial commitment by showing that the owner has invested their own money or secured capital from partners. This investment serves as a down payment signaling seriousness and capability.

Collateral: Collateral acts as security for the loan ensuring that lenders have recourse if the borrower defaults. Real estate or other valuable assets may be included in the loan application to assure lenders.

Conditions: Conditions reflect the market viability of the business like economic factors, competition, industry trends, and the owner's track record. A well-prepared business plan can demonstrate the business's potential for success in various market conditions.

Character: Character includes the education, business background, personal credit history, and reputation of the business owner and staff. Positive references and a solid financial history enhance the perception of reliability and trustworthiness.

Lenders can make informed decisions about extending credit to businesses, mitigating risk, and ensuring the probability of repayment by assessing these factors collectively.

Commercial Credit Score Range and Interpretation

Commercial credit scores are crucial indicators for lenders assessing the risk associated with extending credit to businesses. Commercial credit score range usually ranges from 0 to 100 or 0 to 300 depending on the scoring model. The interpretation of commercial credit scores varies among lenders but generally follows a similar pattern.

- Scores above 80 (or 200) are considered low risk. Businesses with these scores demonstrate a strong credit history and are likely to receive favorable terms and interest rates when applying for credit.

- Scores between 50 and 79 (or 150 to 199) represent moderate risk. While these businesses may still be eligible for credit. Lenders may exercise caution and may offer terms that reflect a slightly higher level of risk.

- Scores below 50 (or 150) indicate high risk. Businesses with these scores may struggle to obtain credit and if approved, they may face less favorable terms and higher interest rates due to the increased risk of default.

Lenders may use these scores to determine whether to extend credit, the terms of credit, and the interest rates offered.

Factors Influencing Commercial Credit Scores

When building a credit scoring rules engine using Nected for your company, there are several factors influencing the commercial credit score model. These can also serve as attributes/conditions for your rules engine according to your company’s needs.

- Financial Performance: Revenue trends, profitability, and cash flow stability are important factors influencing a business's creditworthiness.

- Debt Levels: The ratio of debt to assets and income is closely linked by lenders with high debt levels potentially indicating a greater risk of default.

- Business Structure: Different business structures (e.g., sole proprietorships, partnerships, corporations) have varying levels of liability and financial transparency, impacting credit evaluations.

- Credit Inquiries: The frequency and volume of credit inquiries made by a business can impact its credit score, with multiple recent inquiries suggesting financial distress or sudden liquidity needs.

- Payment History: Timely payment of bills and obligations is a crucial factor in determining creditworthiness. Late payments can significantly impact a business's credit score.

- Credit Utilization: The ratio of credit used to credit available can show how responsibly a business manages its debt. High credit utilization of a business may suggest financial strain.

- Length of Credit History: A longer credit history provides more data for evaluation and can positively influence a business's credit score to track record of responsible credit use.

- Public Records: Bankruptcies, judgments, and other public records can signal financial distress and negatively affect a business's credit score.

- Industry Risk: Considering the industry in which a business operates certain industries may inherently carry higher or lower levels of risk.

Challenges in the Commercial Credit Scoring Model

These are some of the limitations of the traditional commercial scoring model

- Limited Data Availability: Obtaining comprehensive and up-to-date financial information from businesses especially small and medium-sized enterprises (SMEs) can be challenging. Incomplete or outdated data may lead to inaccurate credit evaluations.

- Lack of Standardization: Different credit scoring models and methodologies used by lenders can result in inconsistency in credit assessments. This lack of standardization makes it difficult for businesses to understand how their creditworthiness is being evaluated and for lenders to accurately compare credit risk across different businesses.

- Limited Use of Alternative Data: Traditional credit scoring models often use primarily financial data from credit bureaus overlooking valuable alternative data sources like transactional data, social media activity, and business performance metrics.

- Industry-specific Risk Factors: Certain industries may have unique risk factors that traditional credit scoring models fail to capture. For example, seasonal fluctuations in revenue or reliance on volatile commodity prices may pose challenges in assessing credit risk accurately.

- Rapidly Changing Business: Traditional credit scoring models may struggle to adapt quickly enough to capture these changes leading to outdated credit assessments.

- Scoring Model Variability: Different scoring models may produce disparate results leading to inconsistency in credit evaluations.

How Nected Solves the Challenges in the Commercial Credit Scoring Model

Let us consider a scenario to understand how the commercial credit scoring model with Nected helps to overcome the real-time challenges of building and deploying the commercial credit scoring rules engine.

Scenario: As a financial institution that frequently encounters multiple loan applicants from companies with different backgrounds. you often face the challenge of accurately assessing creditworthiness while managing risk effectively. Let's explore how this scenario evolves and how credit scoring rules engine with Nected can provide valuable support in making informed lending decisions.

Challenges in this scenario:

- Diverse applicants from different backgrounds: The financial institution encounters applicants from various fields and industries but the models need to adapt to the unique characteristics of each business.

- Lack of scalability: The accuracy of the model drops when it experiences multiple applicants at the same time.

- No integration support for data: Commercial scoring models access the financial data from the outsourced database to check the creditworthiness of each applicant this increases the complexity of the model and also increases the wait time for the evaluation.

Implementing a credit scoring model using Nected:

Nected simplifies the implementation of a rules engine with its user-friendly interface. To build a personalized rules engine for your commercial company, you can follow Nected’s easy guide.

However, implementing a commercial credit scoring engine may differ in the specification of attributes and conditions. As discussed earlier, while specifying the rules, it is important to know these parameters:

- Applicant Name

- Loan History

- Type of Organization/Employment Type

- Debt Ratio

- Age

- Credit Limit

- Taxable Income

Conclusion

In conclusion, understanding the commercial credit scoring model is essential for both lenders and financial institutions to make an effective lending decision. To overcome the complexities of the commercial credit scoring models utilize Nected and explore its features by signing up.

FAQs

Q1. What factors are typically considered in commercial credit scoring models?

Commercial credit scoring models typically consider various factors related to a business's financial health and creditworthiness. These may include the company's credit history, payment behavior, financial ratios (such as debt-to-equity ratio, and liquidity ratios), profitability, industry risk, business size, length of time in operation, and any legal or regulatory issues.

Q2. How do commercial credit scoring models differ from consumer credit scoring models?

While commercial and consumer credit scoring models aim to assess credit risk, they differ in several key aspects. Commercial credit scoring models analyze factors relevant to a company's financial stability and ability to repay debt, often incorporating data from business credit reports, financial statements, and industry-specific metrics, while consumer credit scoring models focus on individuals.

Q3. How are commercial credit scoring models used by lenders and financial institutions?

Commercial credit scoring models are used by lenders and financial institutions to assess the risk of extending credit or providing financing to businesses. These models help lenders make informed decisions about whether to approve a loan or line of credit as well as determine the terms and conditions like interest rates and credit limits.

.svg.webp)

.webp)

.jpg)

%20Medium.jpeg)

%20(1).webp)