.png)

Banks run on rules: loan eligibility, credit policy, fee and pricing logic, KYC/AML outcomes, product eligibility, and regulatory checks. When those rules live in core systems or spreadsheets, change is slow, risky, and hard to audit. In 2026, leading banks treat business rule engines (BRE) and BRMS (Business Rules Management Systems) as a strategic layer—separate from core banking—so product, risk, and compliance can own and govern rule logic without waiting on IT releases.

This comparison focuses squarely on business rule engines and BRMS—platforms built to author, execute, version, and govern deterministic business rules (decision tables, rule sets, rule chaining). We do not include broad decision intelligence or flow-first decision platforms (e.g. Taktile) that prioritize end-to-end decision flows and AI orchestration over a rules-engine-first architecture. For banks that need a dedicated rules layer for credit policy, product rules, fees, KYC/AML logic, and compliance, the right choice is a BRE or BRMS.

This blog compares the top 5 business rule engines for banking in 2026—Nected, Inrule, Pega, FICO, and IBM ODM—with a focus on rule authoring and execution, core banking use cases (loan origination, credit policy, product rules, KYC/AML, fraud, compliance), governance and audit, and integration with core and data systems, so you can choose the right rules engine for your bank.

What Is BRE in Banking?

A Business Rule Engine in banking is a dedicated software layer that separates decision logic from the systems that execute transactions. Instead of hardcoding eligibility criteria or policy conditions inside core banking software, those rules live in an external engine that can be updated, versioned, and audited independently.

The simplest way to understand it: a BRE takes inputs (applicant data, transaction values, account attributes), evaluates them against a defined rule set, and returns a decision — without that logic being buried in application code.

Examples of rules a BRE evaluates in banking:

- If credit score ≥ 700 AND debt-to-income ratio ≤ 40%, then approve personal loan

- If transaction amount > $10,000 AND destination country is on sanctions list, then flag for AML review

- If account age < 90 days AND withdrawal > $5,000, then apply fraud hold

- If customer tier is "Gold" AND product is "Fixed Deposit", then apply 0.25% rate premium

These are deterministic rules. Given the same inputs, the engine always returns the same output. That predictability is what makes BREs suitable for regulated environments — the decision path is traceable.

Why banking specifically needs this

Banks deal with rules that change. Regulatory requirements shift. Credit policy gets updated every quarter. Product eligibility changes with new products. When those rules live inside core systems or custom code, changing them means touching production infrastructure — slow, risky, and hard to audit.

A BRE creates a clean separation: the rule logic is managed in one place, independent of the systems that execute it. Product teams, risk teams, and compliance teams can own their rules. IT stays out of the critical path for every policy update.

Benefits of a BRE in banking context:

- Rule changes don't require core system modifications

- Full audit trail of what rule ran, on what input, and what it returned

- Non-technical stakeholders (credit analysts, compliance officers) can review and modify rules

- Consistent decision-making across channels — branch, mobile, API — because the same engine evaluates every request

- Faster response to regulatory changes without deployment risk

Also Read: Top 10 Open-Source Rule Engine in 2026

What Banks Need in 2026?

A business rule engine (BRE) executes predefined business logic: if this condition, then that outcome. It’s the runtime that evaluates rules—well-suited for loan eligibility, pricing, risk bands, fee logic, and policy checks across retail and corporate banking.

A BRMS (Business Rules Management System) adds authoring, versioning, and deployment on top of the rule engine—so business users can change rules without coding. In 2026, banks typically look for BRMS (or BRE with management features) that offer:

- Rule authoring — Decision tables, decision trees, rule sets, and rule chaining so product, risk, and compliance can express policy in a structured, executable form.

- Rules + workflow (optional) — Some BRMS also offer multi-step workflows (e.g. loan origination, KYC, approvals) alongside rules; others are rules-first and integrate with separate BPM/workflow tools.

- Data + integrations — Connectors for core banking, credit bureaus, fraud and sanctions feeds, and internal APIs so rules use live data without custom middleware.

- Governance — Versioning, rollback, audit trails, maker-checker approvals, and controlled rollout—essential for regulators, internal audit, and SOX/compliance.

- AI-assisted authoring (optional) — AI Copilot or ML integration to speed up authoring and testing while keeping rule outcomes deterministic and auditable.

In short: the best business rule engines for banking let you author, run, and govern credit, product, and compliance rules—with optional workflow and AI—instead of locking logic inside core systems or spreadsheets.

Benefits of Business Rule Engines in Banking

Faster rule changes without core system risk Updating a credit policy threshold used to mean a core banking change request, weeks of testing, and a deployment window. With a BRE, it's a rule update — reviewed, approved, and live in hours or days. The blast radius of a rule change is contained and reversible.

Business ownership of policy Credit analysts, compliance officers, and product managers can read, test, and modify rules directly. They don't need to explain a business decision to an engineer and wait for it to be coded correctly. This reduces errors that come from translation between business intent and technical implementation.

Regulatory auditability Every decision has a trace: which rule ran, what the input was, what the output was, who approved the rule version. When regulators ask why an application was declined or a transaction was flagged, the answer is retrievable. Adverse action reason codes become straightforward to generate.

Consistency across channels The same rule engine evaluates decisions whether the request comes from a mobile app, a branch terminal, an API call, or a batch process. Inconsistent decisions across channels — a common problem when logic is embedded in each channel separately — go away.

Reduced technical debt Business logic that accumulates inside core systems or custom code becomes harder to change and impossible to audit cleanly. Moving that logic to a BRE stops the accumulation and makes existing logic visible and manageable.

Faster regulatory response When a regulatory change requires updated screening criteria or revised eligibility rules, the BRE is the right place to make that change — isolated from production systems, testable in a sandbox, auditable from day one.

Read Also: Python Rule Engines: Automate and Enforce with Python

Top 5 Business Rule Engines for Banking

The table below compares Nected, Inrule, Pega, FICO, and IBM ODM on rule engine and BRMS capabilities relevant to banking.

Below is an in-depth look at each platform, with Nected vs. competitor comparison tables framed for banking use cases: loan origination, credit policy, product rules, KYC/AML, fraud, compliance, and core integration.

1. Nected

Nected is a low-code/no-code business rule engine and BRMS that unifies rule execution and workflow orchestration in one layer. It is built to streamline backend processes, decision logic, and experimentation workflows with decision tables, decision trees, rule chaining, and workflow orchestration—so banks can ship credit policy, product eligibility, fee logic, KYC, and fraud rule changes quickly, safely, and at scale without touching core systems.

What sets Nected apart is the combination of ease of authoring (for product, risk, and ops) with production-grade controls (for engineering and compliance), and AI-native rule authoring (AI Copilot, AI Agents) so rules and workflows don’t depend on release cycles or specialist-only tooling.

Key Features (banking-oriented):

- Intuitive low-code/no-code visual rule and workflow designer for lending, product, KYC, and compliance flows

- Decision tables, decision trees, rule chaining via workflow editor

- Triggers: API, webhooks, scheduler, events (upcoming)

- Direct connectors for databases and APIs (no-code UI)—e.g. core banking, credit bureaus, fraud/sanctions providers

- Draft vs. published versions, versioning & rollback, parallel versions

- Audit trails, maker-checker approvals, import/export—suitable for regulatory and internal audit

- AI Copilot and AI Agents for accelerated authoring and optimization

- Cloud + private managed + self-hosted deployment (data residency and on-prem options for regulated banks)

- SOC 2, GDPR, ISO compliant

- High scalability; response time within 100–200 ms; 99.9%+ uptime for real-time decisioning

Pros:

- Unified rules + workflow + AI in one platform

- Strong fit for loan origination, credit policy, product rules, KYC/AML, and compliance workflows

- Non-technical users (product, risk, ops) can manage rules and workflows without coding

- Fast iteration with built-in governance

- Flexible deployment and strong security posture

Cons:

- Teams new to structured rule authoring may need a short onboarding

- Complex legacy core banking systems may require careful integration planning

In summary, Nected stands out as a leading business rule engine and BRMS for banking because it unifies rules, workflows, and AI-native capabilities in a single layer. It offers a user-friendly interface, seamless integrations, and robust governance that suit both technical and non-technical users, making it a strong fit for banks that want to own and optimize credit, product, and compliance rule logic with AI built in.

2. Inrule

Inrule is an enterprise BRMS (Business Rules Management System) with a strong heritage in .NET and on-premises deployments. It provides rule authoring, versioning, and deployment for business logic, with support for decision tables and rule flows. It is rules-first; workflow orchestration and AI-native capabilities are limited compared to modern rule platforms. Implementation and change cycles are typically weeks to months, with higher TCO ($400K–$800K annually in many enterprise deployments) and a .NET-centric architecture that can create lock-in for banks on non-.NET stacks.

Best suited for

Banks already standardized on .NET and Inrule who need enterprise rule governance for lending, product, or operations, and who can accept longer implementation times and higher licensing and operational costs.

Key Features:

- Enterprise rule authoring and deployment

- Versioning and audit (with limitations)

- .NET-centric architecture; integration with other stacks often requires service boundaries

- On-premises and cloud deployment options

Pros:

- Mature enterprise BRMS with governance

- Familiar to teams already on Inrule and .NET

Cons:

- No / limited AI-native capabilities (no built-in AI Copilot or AI Agents)

- Limited workflow orchestration; end-to-end loan origination or KYC workflows often need additional tools

- Complex UI; limited business-user self-serve for product, risk, and ops

- Rule changes often take days to weeks; deployment can be heavy

- High TCO (licensing, infrastructure, change management)

- .NET lock-in for non-.NET core and channels

Read detailed Nected vs Inrule comparison

3. Pega

Pega is a heavyweight enterprise platform for case management, workflows, and decisioning. It combines rules, workflows, and case handling in one ecosystem, with AI and automation capabilities across the platform. It is extremely capable but introduces complexity: longer rollouts, higher licensing costs, and heavier operational overhead. AI-assisted authoring is available but often requires specialist skills; business-user self-serve is not always “lightweight” for product and ops teams.

Best suited for

Large banks that want a unified case/workflow + rules platform and can invest in specialist talent, longer implementations, and higher ongoing platform costs.

Key Features:

- Rules, workflows, and case management in one platform (e.g. lending, disputes, KYC, servicing)

- Strong governance and controls for enterprise environments

- Extensive ecosystem and integration options

- AI and automation capabilities (platform-wide)

- Cloud, on-premises, and hybrid deployment

Pros:

- Powerful enterprise platform for workflows, cases, and rule-based decisioning

- Strong governance and controls—suitable for regulated banking

- Broad ecosystem and integrations

- AI capabilities available

Cons:

- High implementation and operational complexity (slower time-to-value)

- Often requires specialized skills; business-user self-serve can be heavy

- High licensing and platform overhead (TCO can be significant if you mainly need rules + workflows + AI decisioning)

Read detailed Nected vs Pega comparison

4. FICO

FICO (including FICO Blaze and the broader decisioning suite) is a long-standing leader in rule and decision management for banking, insurance, and healthcare. It offers powerful rule authoring, decision modeling, and integration with FICO’s analytics and scoring ecosystem. It is rules- and decisioning-centric, with strong support for complex business logic and enterprise governance. AI-native capabilities (Copilot/Agents-style authoring) are less prominent than in Nected or Pega; the platform is often developer- or analyst-centric, with moderate to high implementation effort and enterprise-level pricing. It is widely used in credit scoring, collections, and fraud in banking.

Best suited for

Banks that already use or plan to use FICO’s analytics and scoring stack and need a robust, governed rules and decisioning layer for credit, risk, or collections.

Key Features:

- Enterprise rule and decision management (e.g. FICO Blaze)

- Strong fit for banking, credit scoring, collections, fraud, insurance

- Integration with FICO analytics and data

- High scalability and governance

- Cloud, on-premises deployment

Pros:

- Deep rule and decision management capabilities

- Strong in regulated, analytics-heavy banking (lending, risk, collections)

- Proven at scale

Cons:

- AI-native authoring (Copilot/Agents) less central than on modern rule platforms

- Non-tech friendly UI and self-serve can be limited for product and ops

- Enterprise-level pricing and implementation (high TCO)

- Maker-checker / approval flows may require custom setup

5. IBM ODM (Operational Decision Manager)

IBM Operational Decision Manager (ODM) is IBM’s enterprise BRMS for authoring, deploying, and governing business rules. It uses Business Action Language (BAL) for natural-language-style rule expression and provides a central repository for rules with versioning, testing, simulation, and traceability. ODM is widely used in banking for loan authorization, fraud detection, credit decisions, and transaction monitoring (e.g. overdraft, limits). It can be deployed on-premises, on OpenShift/Kubernetes, or as part of IBM Cloud Pak for Business Automation. Governance includes role-based permissions and audit trails. ODM is rules-engine-first; workflow orchestration is typically handled outside the product or via IBM BPM. AI-native authoring (Copilot/Agents) is not a core offering. Implementation is often months to a quarter, with high TCO (licensing ~$120K–$325K/year, infrastructure $200K–$300K/year for 1000 TPS in many estimates), and performance is tuning-dependent (~200 ms typical latency; sensitive to network latency between Decision Center and database).

Best suited for

Banks already invested in IBM middleware and Cloud Pak who need a proven, enterprise-grade rule engine for loan rules, fraud, and compliance and can absorb higher cost and longer implementation cycles.

Key Features:

- Rule authoring with Business Action Language (BAL) and decision tables

- Central rule repository with versioning, testing, simulation, audit

- Deployment: standalone, Cloud Pak for Business Automation, OpenShift, Kubernetes, z/OS

- Strong fit for banking: loan limits, transaction monitoring, fraud, credit decisions

- Role-based access and governance; documented proof of decision-making for compliance

Pros:

- Mature enterprise BRMS with deep banking adoption

- Natural-language-style rule authoring (BAL)

- Flexible deployment (on-prem, cloud, hybrid)

- Strong governance and audit trail

Cons:

- No / limited AI-native authoring (no built-in Copilot or AI Agents)

- Implementation: months to quarter; dependency on IBM consultants common

- High TCO (licensing, infrastructure, change management; often $670K–$1.3M/year for 1000 TPS)

- Business-user self-serve limited; complex UI and deployment

- Performance tuning-dependent; latency ~200 ms; degradation under peak load reported

- Maker-checker / approval flows may require custom or process integration

Read detailed Nected vs IBM ODM comparison

How AI Is Reshaping Business Rule Engines for Banking

AI is changing how banking rules get built and maintained

AI in a business rule engine isn’t about replacing deterministic rules. It’s about shortening the lifecycle from policy to production:

- Turning credit policy, product guidelines, and fee schedules into executable rules faster

- Generating edge-case test data for risk, fraud, and compliance scenarios

- Explaining decision paths to ops, compliance, and regulators (e.g. adverse action, reason codes)

- Detecting conflicts and unreachable rules in large policy sets

- Guiding refactors of complex rule bases (e.g. pricing, eligibility, overdraft)

For banking teams, “good AI” inside a rule platform means:

- Authoring: “Create rules for personal loan eligibility with these income and DTI bands…”

- Refactoring: “These product eligibility rules overlap—suggest a merged decision table.”

- Testing: “Generate edge-case inputs to stress this credit policy ruleset.”

- Explainability: “Why did we decline this applicant? Show reason codes for adverse action and audit.”

AI becomes useful when the platform has a solid foundation: schemas, versioning, environments, replay, and observability. The platforms compared here are evaluated on whether AI-native capabilities are built in and governable, not bolted on.

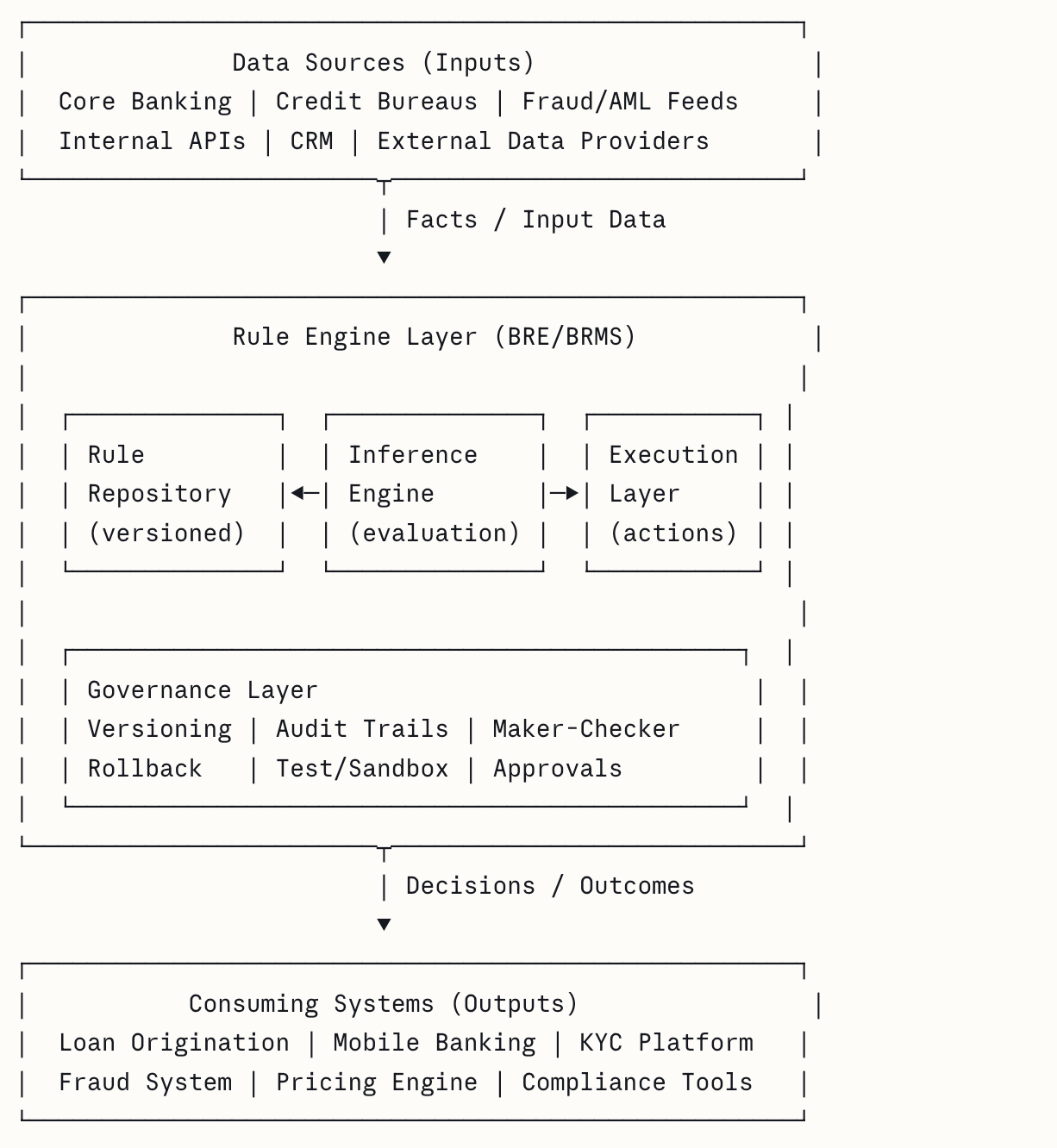

Business Rule Engine Architecture in Banking

A banking BRE sits as a dedicated layer between the data sources that supply facts and the systems that act on decisions.

Rule Repository — stores all rule definitions with full version history. Every change is tracked. Previous versions can be restored. In a banking context, this repository also serves as documentation for regulatory exams — auditors can see exactly what rule was active at any point in time.

Inference Engine — the evaluation core. Takes the input facts (applicant attributes, transaction data, account state) and determines which rules match. For complex banking rules — multiple conditions, nested logic, exception handling — this engine traverses the condition tree recursively and resolves conflicts based on priority or grouping.

Execution Layer — runs the actions triggered by matched rules. Returns the decision: approved, declined, referred, flagged. May also trigger downstream actions — sending a notification, updating a record, routing to a human review queue.

Governance Layer — where banking-specific requirements live. Versioning ensures you can trace which rule version ran on a specific application at a specific time. Maker-checker enforces four-eyes approval before rule changes go live. Audit trails satisfy internal audit and regulatory examination requirements. Test/sandbox environments let teams validate rule changes before production deployment.

Integration points — a banking BRE needs to pull live data from multiple sources during evaluation. Credit bureau scores, KYC status, transaction history, sanctions list checks. The architecture needs to handle these data calls cleanly, either by pre-loading facts before evaluation or by lazy-loading them as rules require specific inputs.

Also Read: Rule Engine Design Pattern

How to Choose the Best Business Rule Engine for Banking

What’s driving demand in 2026

The global BRMS market is projected to reach approximately USD 2.48 billion in 2026, with a CAGR of ~8.15% through 2031. Gartner forecasts that by 2027, AI will augment or automate 50% of business decisions. Banks are looking for business rule engines and BRMS that combine deterministic rules, AI-driven authoring and optimization (where needed), workflows, and real-time governance—so product, risk, and compliance can own and iterate on credit, product, and compliance rules at market speed without sacrificing auditability.

What to look for (banking lens): Use Cases of BRE in Banking

Loan origination and credit decisioning Eligibility rules for personal loans, mortgages, auto loans, and credit cards. Credit score bands, income thresholds, DTI ratios, employment conditions — all defined as rules that credit teams can update without engineering involvement. The BRE evaluates each application against the current policy and returns an approve, decline, or refer decision in real time.

Product eligibility and onboarding Which products a customer qualifies for based on their profile. Account tenure, balance history, credit standing, geographic restrictions. When product eligibility rules change (new product launches, promotional criteria, regulatory restrictions), the BRE updates handle it without touching the core banking system.

KYC/AML rules and transaction monitoring Screening rules for sanctions lists, PEP checks, and suspicious transaction patterns. Rules that flag transactions for manual review based on amount, frequency, destination, or counterparty. AML rules in particular change as regulatory guidance evolves — a BRE makes those updates manageable.

Fraud detection Velocity rules, behavioral anomaly conditions, device fingerprint checks, geographic inconsistency flags. Fraud patterns shift constantly; fraud teams need to update detection rules quickly without deployment cycles. The BRE is the right layer for this.

Pricing and fee logic Interest rate bands based on credit score and product type, fee waiver eligibility, promotional rate conditions. Pricing rules change with market conditions and competitive response. Keeping them in a BRE means the pricing team can respond without opening a change request to engineering.

Regulatory compliance checks Rules encoding specific regulatory requirements — stress testing criteria, reporting thresholds, permitted product structures. When regulations change, the compliance team updates the rules in the BRE rather than waiting for a core system release.

Why Nected fits the 2026 banking rule engine market

Nected was built as a unified rules + workflow platform with AI-native authoring from the ground up. It combines:

- Visual rule authoring (decision tables, trees, chaining) with workflow orchestration (triggers, approvals, multi-step flows) for lending, product, KYC, and compliance

- Direct connectors for databases and APIs

- Governance (versioning, audit trails, maker-checker) built in

- AI Copilot and AI Agents for accelerated authoring and optimization

- Cloud + private managed + self-hosted deployment (data residency and on-prem options for regulated banks)

- SOC 2, GDPR, ISO compliance

Banks can run everything from simple product eligibility and fee rules to complex loan origination and KYC decision workflows—with AI built in—without stitching multiple tools together.

Conclusion

The business rule engine market for banking in 2026 is less about “who can execute rules” and more about who can operationalize change safely and at speed:

- Can product, risk, compliance, and engineering collaborate safely?

- Can you ship rule and workflow changes (credit policy, product rules, fee logic, KYC steps) without redeploying core or custom apps?

- Can you govern and audit rules at scale for regulators and internal audit?

- Can you integrate core banking, bureaus, and fraud/sanctions feeds without glue-code debt?

- Can AI accelerate the rule lifecycle without increasing risk or reducing explainability?

If your rules sit in the blast radius of lending, product, pricing, KYC/AML, or compliance, your choice of business rule engine (or BRMS) is a long-term architecture decision. Choose the platform that makes safe change and business-user ownership the default, not the exception.

FAQs

What is a Business Rule Engine (BRE) in banking?

A business rule engine executes predefined business logic (e.g. if income ≥ X and DTI ≤ Y, then eligible for product Z). In banking, BREs are used for loan eligibility, credit policy, product eligibility, fee and pricing logic, KYC/AML outcomes, and regulatory checks. A BRMS (Business Rules Management System) adds authoring, versioning, and deployment so business users can change rules without coding. Modern BRMS often combine rules with workflow and AI-assisted authoring for end-to-end rule lifecycle management.

What’s the difference between a Business Rule Engine and a BRMS?

A business rule engine is the runtime that evaluates rules (if/then logic). A BRMS typically includes the engine plus rule authoring, versioning, deployment, and governance. In 2026, many banks look for BRMS that also offer workflow orchestration and AI-native authoring (e.g. Copilot, Agents) so they can model and run full decision flows (e.g. loan origination, KYC) with auditability.

Why do banks need a dedicated Business Rule Engine?

Banks need a dedicated rule layer so that product, risk, and compliance can change eligibility, pricing, and policy logic without touching core banking systems or waiting on IT releases. A good BRE or BRMS provides versioning, audit trails, maker-checker, and rollback—essential for regulators and internal audit. It also allows integration with core, bureaus, and fraud feeds so rules use live data.

How do Business Rule Engines support regulatory compliance in banking?

By providing controlled change and governance: versioning, approvals, audit trails, test/sandbox environments, and monitoring/alerts. Rule changes become traceable (who, what, when) and safer than changing core or custom code. Maker-checker and explainability (e.g. reason codes for adverse action) support fair lending and regulatory exams. Platforms with AI can accelerate authoring and testing while keeping rule outcomes deterministic and auditable.

When should a bank choose a dedicated BRE/BRMS over hard-coding rules in core?

Choose a dedicated business rule engine or BRMS when you need to change rules frequently (credit policy, product eligibility, fees, KYC logic), govern and audit changes for compliance, and let business users (product, risk, ops) own rule updates without coding. Choose hard-coding in core when rules are stable, rarely change, and your bank has no requirement for business-user authoring or detailed audit trails.

.svg.webp)

.webp)

.webp)

.webp)

.webp)

.jpeg)

%20(1).webp)