.png)

.webp)

Credit risk assessment is about figuring out how likely a borrower is to miss payments or default. Banks, lenders, and fintech teams use it to cut losses, keep portfolios under control, and make better lending calls. It also helps with compliance, which is where things usually get messy if the process is weak.

There are different types of credit risk involved, and each one needs a slightly different response. That’s why credit risk assessment techniques matter so much. A decent model on paper can still fail if the inputs are stale or the policy is vague.

This article covers the main types of credit risk, the credit risk assessment process, and the tools teams use to manage it day to day. Nected shows up here too, mainly because it helps with rule-based scoring and monitoring without making the workflow harder than it needs to be.

What Are the Types of Credit Risk?

Credit risk isn't one thing. It shows up in different forms depending on who's borrowing, what's being financed, and what's happening in the broader market. These are the main types worth understanding.

Default Risk

The most straightforward one. A borrower takes on debt and can't pay it back. A company hits financial trouble, cash flow dries up, payments stop. The lender absorbs the loss. Most credit risk conversations start here because it's the most direct and measurable form.

Credit Spread Risk

This one matters more to investors than lenders. It's about the gap between what a credit instrument yields and what a risk-free benchmark yields. When that gap widens, it signals the market thinks default is more likely — and the bond loses value even if the borrower hasn't actually defaulted yet. The risk is in the perception shift, not just the event.

Counterparty Risk

Common in derivatives and structured transactions. Both parties have obligations. If one side fails to deliver — doesn't pay, doesn't transfer the securities, doesn't fulfill the contract — the other side takes the hit. This part often gets underestimated in complex financial arrangements where the chain of obligations is long.

Concentration Risk

Happens when exposure gets too narrow. A bank that's heavily lent into one sector — say, oil and gas — is fine when that sector is fine. But a single industry downturn can cause disproportionate damage to the whole portfolio. Same logic applies to geographic concentration or over-reliance on a single large borrower.

Migration Risk

Borrower credit quality doesn't stay static. A company that was investment grade last year might be junk-rated this year. That downgrade changes the risk profile of everything connected to it — bond valuations drop, reserve requirements shift, investor confidence falls. Migration risk is about tracking that movement, not just the current snapshot.

Sovereign Risk

Lending to governments isn't risk-free. Countries can face debt crises, political instability, or currency collapse — any of which can make it difficult or impossible to meet debt obligations. Investors holding government bonds aren't immune to loss, and this type of risk tends to be correlated with broader economic conditions in ways that are hard to hedge.

Settlement Risk

A more operational form of credit risk, but still consequential. Two parties agree to exchange assets — securities for cash, for example. One side pays. The other doesn't deliver. The paying party is now out the cash with nothing to show for it. Settlement risk is highest in high-volume, time-sensitive transactions where the window between agreement and settlement creates exposure.

Also Read: Credit Scoring Python

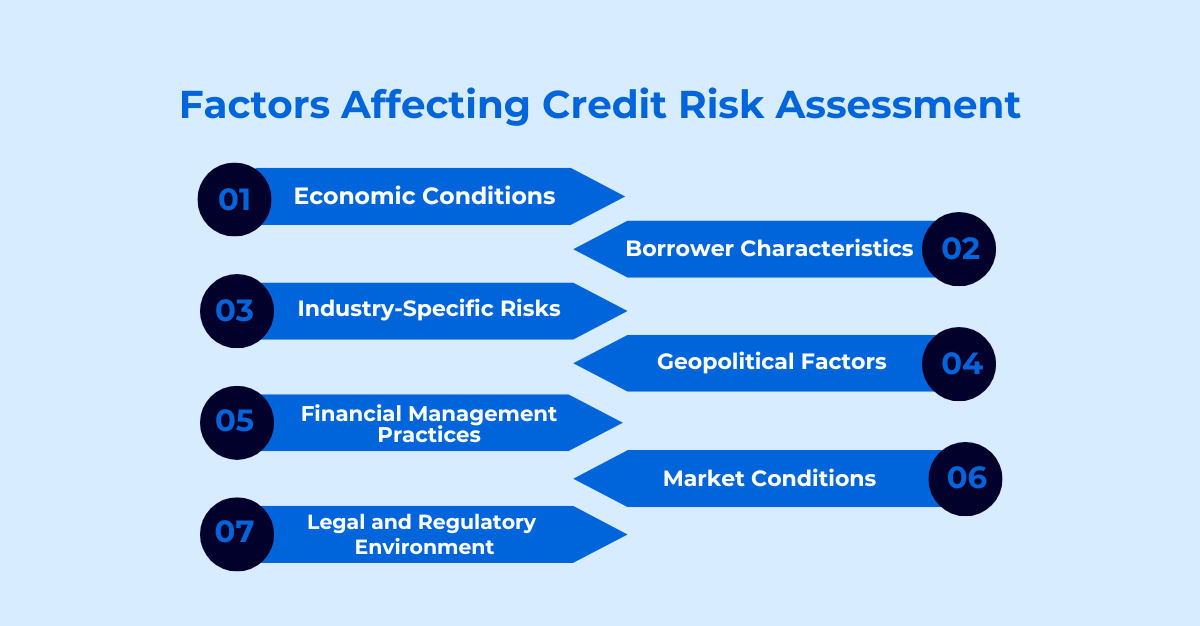

Which Factors Influence Credit Risk?

Rules and models help assess credit risk, but the underlying factors driving it are messier and harder to pin down. Here are the main ones.

Economic Conditions

The macro environment sets the baseline. High inflation erodes real income. Rising unemployment means more borrowers under financial stress. Slow growth squeezes business revenues. All of that flows downstream into repayment ability. In a strong economy, credit risk tends to compress. In a weak one, it expands — sometimes faster than models anticipate.

Borrower Characteristics

Credit history, income stability, existing debt load — these are the fundamentals. A borrower with a long history of on-time payments, steady income, and manageable debt is lower risk almost by definition. The opposite profile raises risk across every dimension. This seems obvious, but it's where a lot of the actual credit decision weight sits.

Industry-Specific Risks

Not all industries carry the same risk profile. Oil and gas is sensitive to commodity prices. Healthcare is exposed to regulatory changes. Retail is vulnerable to consumer sentiment shifts. A borrower's industry shapes their risk even when their individual financials look fine — because sector-level downturns can drag down otherwise healthy companies.

Geopolitical Factors

Trade conflicts, sanctions, political instability — these create disruptions that ripple through supply chains, currencies, and economies. A borrower operating across multiple jurisdictions can look stable until a geopolitical event changes the operating environment overnight. This factor is hard to model and easy to underweight until it isn't.

Financial Management Practices

Two borrowers can have similar revenue and still carry very different risk profiles based on how they manage their finances. Strong cash flow discipline, conservative leverage, and regular financial monitoring all reduce risk. Poor budgeting, excessive debt accumulation, and weak internal controls increase it. This is the management quality dimension — and it's often more predictive than surface-level financials.

Market Conditions

Interest rate changes affect borrowing costs directly. When rates rise, variable-rate debt gets more expensive and refinancing becomes harder. Market downturns can hit asset values, reduce collateral worth, and tighten liquidity — all of which affect a borrower's ability to service debt. Market conditions can shift the risk profile of an entire portfolio quickly.

Legal and Regulatory Environment

New regulations can change what's permissible, what's required, and what costs are imposed on borrowers. Stricter compliance requirements add overhead. Industry-specific rules can constrain revenue or require capital allocation that reduces repayment flexibility. The legal environment doesn't move fast, but when it does, it can affect creditworthiness across entire sectors at once.

Also Read: Credit Scoring Platforms

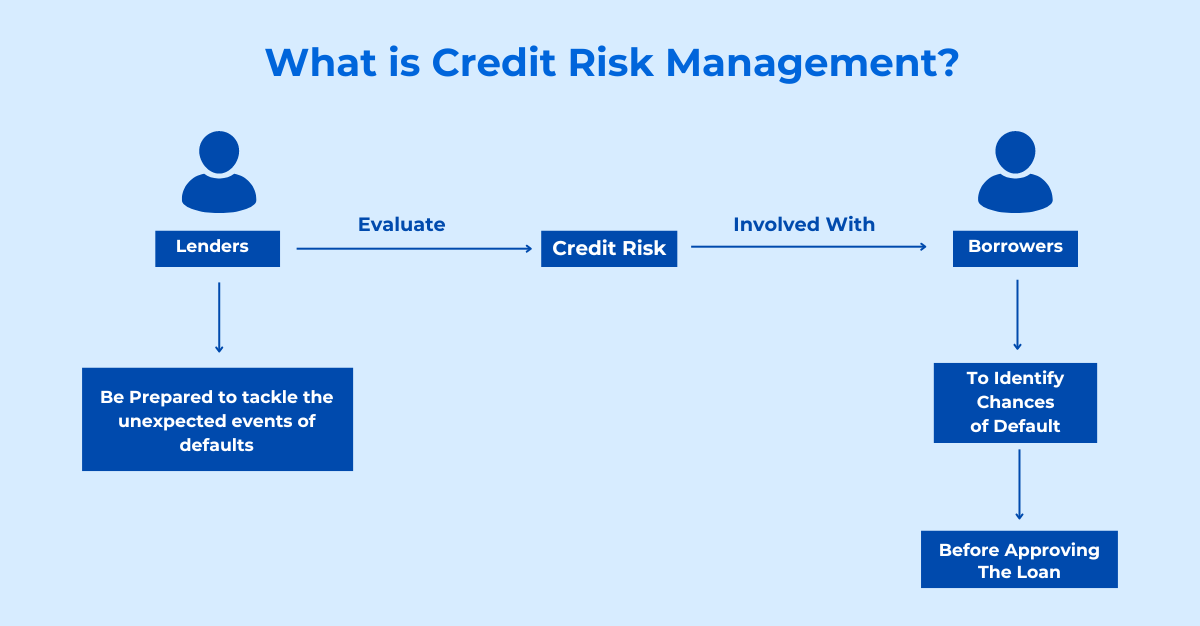

What Is Credit Risk Assessment?

Credit risk assessment is how lenders figure out whether a borrower or business might fail to repay. The review usually pulls in credit history, financial health, sector risks, and the broader economy. Nothing fancy there. It’s mostly about separating acceptable risk from the kind that can blow up a portfolio later.

That decision affects loan terms, pricing, approval, and how much exposure a lender is willing to take. It also feeds into credit risk management, which is the part that keeps the process from turning into guesswork.

Importance of Credit Risk Assessment

Credit risk assessment matters because bad lending decisions are expensive. If a lender misses early warning signs, defaults climb fast and recovery gets harder. Good assessment reduces that risk before it becomes a problem.

It also helps with compliance. Financial institutions have to show that lending decisions are based on consistent criteria, not loose judgment or random exceptions. This part often gets ignored until an audit or regulator asks uncomfortable questions.

There’s another side to it too: better decisions. When teams use structured credit risk assessment techniques, they can compare borrowers more fairly, set tighter limits, and avoid overexposure to one segment. That makes credit risk management easier to keep under control, especially when volumes start growing.

Credit Risk Assessment Process

The process is usually simple on paper, but the execution is where things usually break.

- Data Collection: Start with borrower data. That includes credit history, income, debt, repayment behavior, and any business financials if the borrower is a company. A lot depends on this step. Bad inputs lead to bad scores, and that never ends well.

- Risk Analysis: Next comes the review. The lender checks patterns, red flags, and the type of credit risk involved. This can include repayment history, sector exposure, market conditions, and policy exceptions.

- Scoring Model: After that, the data gets translated into a score or rating. Some teams use credit scoring tools. Others use more layered credit risk assessment techniques with rule engines, models, and manual overrides. The point is to turn the messy part into something usable.

- Decision: Finally, the lender decides whether to approve, reject, or approve with conditions. The output can also affect limits, pricing, or collateral requirements. In many systems, this is where credit risk management tools connect the analysis to actual policy.

Once this loop is in place, it becomes easier to repeat the same logic across borrowers instead of re-evaluating everything from scratch every time.

Also Read: Open source Credit Scoring Software

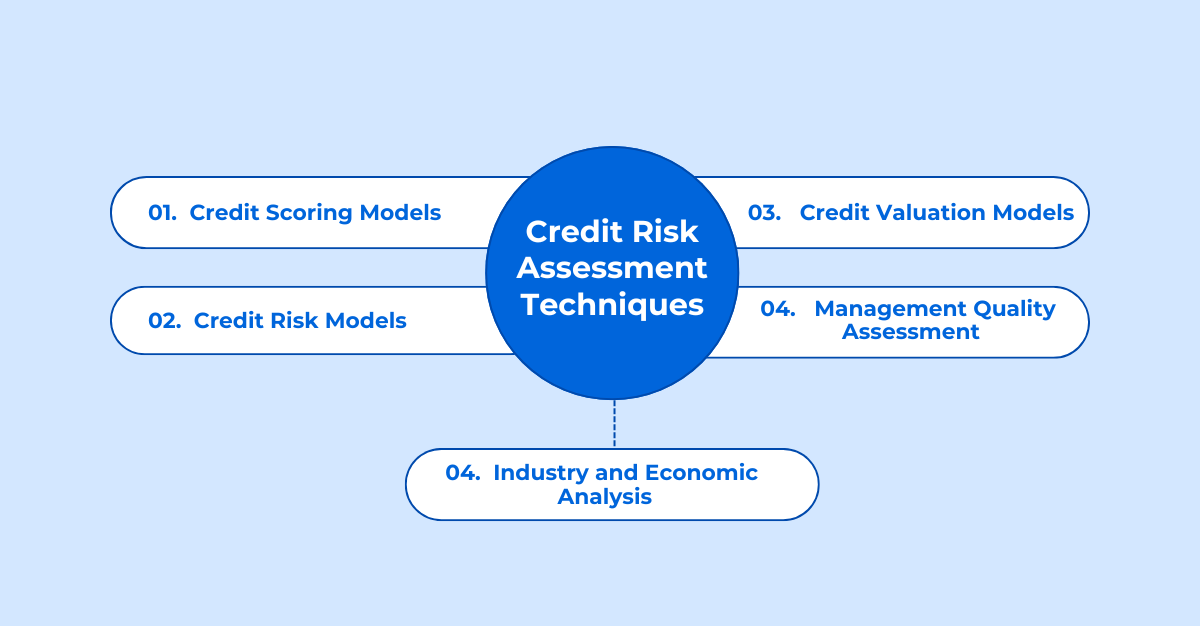

What Are Some Credit Risk Assessment Models?

Credit risk assessment models help evaluate the likelihood of borrower default and possible losses. Common credit risk assessment techniques include:

1. Credit Scoring Models: These models assign a numerical score that reflects the likelihood of default. It incorporates factors such as payment history, credit utilization, length of credit history, and types of credit accounts. Common examples include FICO scores and VantageScore, which help lenders make quick, data-driven lending decisions.

2. Credit Risk Models: These models use advanced techniques to estimate the likelihood of borrower default and potential losses. They incorporate historical data, financial ratios, and economic indicators. Methods like logistic regression, decision trees, and machine learning help refine these predictions and improve accuracy.

3. Credit Valuation Models: These models determine the fair value of credit-related instruments, such as bonds, by evaluating default risk and potential recovery rates. Models like Credit Valuation Adjustment (CVA) and the Merton model help investors and institutions price and manage credit risk effectively.

4. Management Quality Assessment: This involves evaluating the borrower’s management team to gauge credit risk. Factors such as experience, competence, and past performance are assessed. Strong management usually indicates better decision-making and risk management, which can lower the risk of default.

5. Industry and Economic Analysis: This technique examines industry trends and economic conditions to understand how they affect a borrower’s credit risk. By evaluating factors like economic cycles and regulatory changes, institutions can better assess how external conditions might impact a borrower’s ability to repay loans.

Credit Risk Management

Credit risk management is what happens after the assessment. You do not just score a borrower and move on. Teams need to keep watching exposure, repayment behavior, and changes in borrower health over time.

Monitoring is the first layer. If a borrower starts missing payments, taking on too much debt, or showing weaker cash flow, the risk profile shifts. That’s where credit risk management tools come in handy because they surface the change before it becomes a loss.

Mitigation usually means tightening limits, changing loan terms, asking for more collateral, or reducing exposure in risky segments. Policy implementation matters too. Without clear rules, the same borrower can get treated differently by different teams, and that creates noise fast.

Good credit risk management is not just about catching problems. It is also about making sure the response is consistent and defensible.

Credit Risk Monitoring Strategies

Utilizing credit risk monitoring tools and establishing effective strategies, you can manage potential losses from borrower defaults. These strategies include:

1. Key Performance Indicators (KPIs): KPIs are essential for evaluating how well credit risk management is performing. They track metrics such as missed payments, overdue accounts, and repayment rates. By examining these KPIs, financial institutions can assess their performance, identify trends, and make informed decisions to manage risks effectively.

2. Risk Reporting and Dashboards: Risk reporting tools and dashboards provide a clear, up-to-date view of credit risks. They use visuals such as heat maps and graphs to help decision-makers quickly understand and address new risks. Regular reports keep management informed about current risks and support timely actions.

3. Early Warning Systems: Early warning systems help spot potential credit problems before they become serious. They use data to detect signs of trouble, like changes in payment behavior or economic conditions. Early alerts allow banks to take action before problems grow.

4. Credit Review Processes: Regular credit reviews are important to keep risk assessments up-to-date. These reviews check the creditworthiness of borrowers and analyze the performance of the credit portfolio. They help banks adjust their strategies based on current borrower and market conditions.

5. Credit Risk Limits and Thresholds: Setting credit risk limits helps manage how much risk a bank takes on. Limits are set for individual borrowers, sectors, or the whole portfolio. If these limits are exceeded, actions like tightening credit terms or reducing exposure are triggered to control risk.

6. Portfolio Analysis: Portfolio analysis means reviewing the credit portfolio to find risks and opportunities. By checking details like borrower types, industries, and locations, banks can make informed decisions to manage risks and enhance their portfolio.

7. Customer Feedback and Interaction: Talking to customers provides useful information about their financial health and potential risks. Regular check-ins and feedback sessions help banks understand changes in borrowers’ situations and spot potential issues early. This helps improve credit risk assessments and build stronger relationships.

Read about: Credit Scoring: Uses, Benefits & Tool Comparison

Credit Risk Management Tools

Credit risk management tools are usually a mix of scoring, rules, analytics, and monitoring. You rarely get by with just one.

Risk scoring tools help rank applicants or borrowers based on how likely they are to default. Rule engines add policy logic on top of that, so the system can approve, reject, or flag cases based on specific conditions. That part often gets ignored until the manual review queue gets too big.

Analytics platforms are useful when teams want a broader view of portfolio movement, delinquency trends, or concentration by sector and geography. Monitoring systems handle the ongoing side of credit risk management. They track changes in repayment behavior, trigger alerts, and keep the process from going stale.

Nected fits into this mix as a low-code option for building rule-based scoring and decision workflows. It gives teams a way to connect policy, scoring, and monitoring without stitching together too many disconnected systems.

How Nected Helps in Building Credit Scoring Models?

If you’re looking for an efficient tool for building credit scoring models, Nected is your go-to solution. Creating accurate credit scoring models for risk assessment is a seamless process with Nected, even for non-tech users, thanks to its easy-to-use yet advanced features.

Nected is a versatile low-code/no-code tool for building credit scoring models. Its rules-based approach stands out from traditional systems, offering dynamic and adaptable rule-setting capabilities.

Designed with user experience in mind, Nected’s intuitive interface simplifies defining, configuring, and building credit scoring rules. Users can set parameters and adjust criteria without extensive coding or complex setup, enabling quick deployment and modification of credit scoring models.

With Nected’s credit scoring solutions, you can analyze various data points according to your business needs, including credit history, employment status, and financial behavior, to generate a credit score. This score helps lenders make informed decisions and assess overall risk.

This modern approach not only enhances efficiency and accuracy in credit scoring but also improves the adaptability of the models to meet diverse user needs. One of Nected's core strengths is its ability to accommodate various credit scoring paradigms.

Nected speeds up credit score evaluations and ensures consistency. Lenders can use Nected’s systems to monitor changes in a borrower's credit status and adjust lending terms as needed.

Use Cases of Credit Risk Assessment

Credit risk assessment shows up in a few places people already expect. Loan approval is the obvious one. Lenders use it to decide whether a borrower qualifies and on what terms.

It also matters for credit cards, where issuers need to balance approval rates with loss risk. In fintech lending, the process has to move fast, so automated scoring and rule-based decisions do a lot of the heavy lifting. SME lending is another big use case, especially when small businesses do not have perfect records but still need funding.

In each case, the same core idea applies: use credit risk assessment techniques to make the decision faster and less random.

Benefits of Credit Risk Assessment

The most obvious benefit is faster decisions. Once the process is structured, lenders do not have to spend as much time on manual checks for every application.

It also reduces defaults. Better assessment means weak borrowers are easier to spot early, which helps keep losses down. On top of that, it improves compliance because decisions are more consistent and easier to explain later.

That’s the real value here. Not just better scores, but fewer surprises.

Conclusion

Effective credit risk management is crucial for banks and financial institutions. It helps them stay stable and make a profit. Key strategies include understanding various types of credit risks, using reliable tools like credit scoring models, and implementing strong monitoring practices.

As the financial world changes, institutions need to keep an eye on new risks and update their strategies to avoid losses. Advanced tools like analytics and machine learning will help make credit risk management more accurate and responsive.

With ongoing changes in the economy and technology, more sophisticated monitoring will be necessary. Embracing these innovations will help institutions better manage credit risk and achieve better financial results. For an advanced solution in credit risk assessment and management, consider Nected.

Nected's advanced analytics and real-time processing capabilities provide a powerful edge in developing accurate credit scoring models and effective monitoring strategies. Explore how Nected can refine your credit risk management approach and drive better financial outcomes.

FAQs About Credit Risk Assessment

Q1. What is credit risk assessment?

Credit risk assessment is the process of checking how likely a borrower is to default. Lenders use it to decide whether to approve credit, what terms to offer, and how much exposure to take on.

Q2. What are credit risk types?

Common type of credit risk include default risk, counterparty risk, concentration risk, migration risk, sovereign risk, credit spread risk, and settlement risk.

Q3. How is credit risk measured?

It is usually measured with credit scores, financial ratios, repayment history, and model-based analysis. Some lenders also use internal ratings and rule-based systems to track risk across a portfolio.

Q4. What tools are used?

Teams use credit risk management tools like scoring models, rule engines, analytics platforms, dashboards, and monitoring systems. Nected is one option for setting up rule-based credit scoring and decision workflows without a heavy build.

.svg.webp)

.webp)

.webp)

.jpg)

.webp)

%20(1).webp)